- Share

Why Small Business Lending Isn’t What It Used to Be

Since the Great Recession, bank lending to small businesses has fallen significantly, and policymakers have become concerned that these businesses are not getting the credit they need. Many reasons have been suggested for the decline. Our analysis shows that it has multiple sources, which means that trying to address any single factor may be ineffective or make matters worse. Any intervention should take all of the many causes of the decline in small business lending into consideration.

The views authors express in Economic Commentary are theirs and not necessarily those of the Federal Reserve Bank of Cleveland or the Board of Governors of the Federal Reserve System. The series editor is Tasia Hane. This paper and its data are subject to revision; please visit clevelandfed.org for updates.

Small business lending has dropped substantially since the Great Recession. While some measures of small business lending are now above their lowest levels since the economic downturn began, they remain far below their levels before it. For example, in the fourth quarter of 2012, the value of commercial and industrial loans of less than $1 million—a common proxy for small business loans—was 78.4 percent of its second-quarter 2007 level, when measured in inflation-adjusted terms. And despite an increase of nearly 100,000 small businesses over the period, the number of these loans dropped by 344,000 over the 2007 to 2012 period (many such loans arguably go to small businesses).1

Policymakers have become concerned that the decline in small business lending may be hampering the economic recovery. Small businesses employ roughly half of the private sector labor force and provide more than 40 percent of the private sector’s contribution to gross domestic product. If small businesses have been unable to access the credit they need, they may be underperforming, slowing economic growth and employment.

Different views have emerged about the cause of the slowdown. Bankers say the problem rests with small business owners and regulators—business owners for cutting back on loan applications amid soft demand for their products and services, and regulators for compelling the banks to tighten lending standards (which cuts the number of creditworthy small business owners). Small business owners, in turn, say the problem rests with bankers and regulators—bankers for increasing collateral requirements and reducing their focus on small business credit markets, and regulators for making loans more difficult to get.

In our analysis, we find support for all of these views. Fewer small businesses are interested in borrowing than in years past, and at the same time, small business financials have remained weak, depressing small business loan approval rates. In addition, collateral values have stayed low, as real estate prices have declined, limiting the amount that small business owners can borrow.

Furthermore, increased regulatory scrutiny has caused banks to boost lending standards, lowering the fraction of creditworthy borrowers. Finally, shifts in the banking industry have had an impact. Bank consolidation has reduced the number of banks focused on the small business sector, and small business lending has become relatively less profitable than other types of lending, reducing bankers’ interest in the small business credit market.

Because none of these factors is the sole cause of the decline in small business credit, any proposed intervention needs to take into account the multiple factors affecting small business credit.

The Demand-Side Problem

Bankers say that the main reason small business lending is lower now than before the Great Recession is that demand has fallen. Small business owners, they argue, aren’t expanding, depressing the amount that the small business sector needs to borrow.

This is no doubt part of the story. Small businesses were hit hard by the economic downturn. Analysis of data from the Federal Reserve Survey of Consumer Finances reveals that the income of the typical household headed by a self-employed person declined 19 percent in real terms between 2007 and 2010. Similarly, Census Bureau figures indicate that the typical self-employed household saw a 17 percent drop in real earnings over a similar period.

Weak earnings and sales mean that fewer small businesses are seeking to grow. Data from the Wells Fargo/Gallup Small Business Index—a measure drawn from a quarterly survey of a representative sample of 600 small business owners whose businesses have up to $20 million a year in sales—show that the net percentage of small business owners intending to increase capital investment over the next 12 months fell between 2007 and 2013. In the second quarter of 2007, it was 16 (the fraction intending to increase capital investment was 16 percentage points higher than the fraction intending to decrease capital investment), while in the second quarter of 2013, it was –6 (the fraction intending to decrease capital investment was 6 percentage points higher than the fraction intending to increase it). Similarly, the net percentage of small business owners planning to hire additional workers over the next 12 months was 24 in the second quarter of 2007, but only 6 in the second quarter of 2013.

Reduced small business growth translates into subdued loan demand. Thus, it is not surprising that the percentage of small business members of the National Federation of Independent Businesses (NFIB) who said they borrowed once every three months fell from 35 percent to 29 percent between June 2007 and June 2013.

Some of the subdued demand for loans may stem from business owners’ perceptions that credit is not readily available. According to the Wells Fargo/Gallup Small Business Index survey, in the second quarter of 2007, 13 percent of small business owners reported that they expected that credit would be difficult to get in the next 12 months. By the second quarter of 2013 that figure had increased to 36 percent. By contrast, 58 percent of small business owners said credit would be easy to get during the next 12 months when asked in 2007, compared to 24 percent six years later.

Small Businesses Are Less Creditworthy Than They Used to Be

Lenders see small businesses as less attractive and more risky borrowers than they used to be. Fewer small business owners have the cash flow, credit scores, or collateral that lenders are looking for. According to the latest Wells Fargo/Gallup Small Business Index, 65 percent of small business owners said their cash flow was “good” in the second quarter of 2007, compared to only 48 percent in the second quarter of 2013.

Small business credit scores are lower now than before the Great Recession. The Federal Reserve’s 2003 Survey of Small Business Finances indicated that the average PAYDEX score of those surveyed was 53.4. By contrast, the 2011 NFIB Annual Small Business Finance Survey indicated that the average small company surveyed had a PAYDEX score of 44.7. In addition, payment delinquency trends point to a decline in business credit scores. Dun and Bradstreet’s Economic Outlook Reports chart the sharp rise in the percent of delinquent dollars (those 91 or more days past due) from a level of just over 2 percent in mid-2007 to a peak above 6 percent in late-2008. While delinquencies have subsided somewhat since then, the level as of late 2012 remained at nearly 5 percent, notably higher than the pre-recession period.

More lending is secured by collateral now than before the Great Recession. The Federal Reserve Survey of Terms of Business Lending shows that in 2007, 84 percent of the value of loans under $100,000 was secured by collateral. That figure increased to 90 percent in 2013. Similarly, 76 percent of the value of loans between $100,000 and $1 million was secured by collateral in 2007, versus 80 percent in 2013.

The decline in value of both commercial and residential properties since the end of the housing boom has made it difficult for businesses to meet bank collateral requirements. A significant portion of small business collateral consists of real estate assets. For example, the Federal Reserve’s 2003 Survey of Small Business Finances showed that 45 percent of small business loans were collateralized by real estate.

On the residential side, Barlow Research, a survey and analysis firm focused on the banking industry, reports that approximately one-quarter of small company owners tapped their home equity to obtain capital for their companies, both at the height of the housing boom and in 2012. The value of home equity has dropped substantially since 2006. According to the Case-Shiller Home Price Index, the seasonally-adjusted composite 20 market home price index for April 2013 was only 73.8 percent of its July 2006 peak.

On the commercial side, the Moody’s/Real commercial property price index (CPPI) shows that between December 2007 and January 2010, commercial real estate prices dropped 40 percent. While prices have recovered somewhat since then, the index (as of February 2013) is still 24 percent lower than in 2007.

Lending Standards Have Tightened

At the same time that fewer small businesses are able to meet lenders’ standards for cash flow, credit scores, and collateral, bankers have increased their credit standards, making even fewer small businesses appropriate candidates for bank loans than before the economic downturn. According to the Office of the Comptroller of the Currency’s Survey of Credit Underwriting Practices, banks tightened small business lending standards in 2008, 2009, 2010, and 2011.

Loan standards are now stricter than before the Great Recession. In June 2012, the Federal Reserve Board of Governors asked loan officers to describe their current loan standards “using the range between the tightest and easiest that lending standards at your bank have been between 2005 and the present.” For nonsyndicated loans to small firms (annual sales of less than $50 million), 39.3 percent said that standards are currently “tighter than the midpoint of the range,” while only 23 percent said they are “easier than the midpoint of the range.”

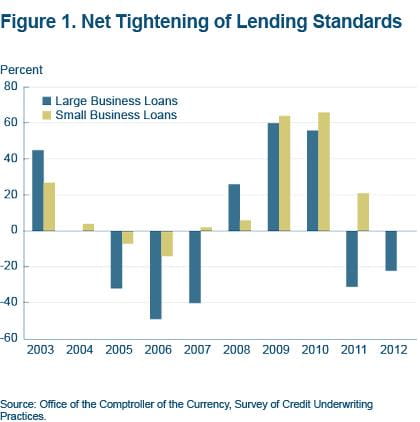

Moreover, while banks have loosened lending standards for big businesses during the recent economic recovery, they have maintained tight standards for small companies. Figure 1 shows the net tightening of lending standards (the percentage of banks tightening lending standards minus the percentage loosening them) for small and large customers from 2003 to 2012. As the figure indicates, net tightening was slightly greater for small businesses than large businesses in 2009 and 2010. However, in 2011 and 2012, there was a net tightening of lending standards for small businesses, despite a net loosening for big businesses.

While banks adjust lending standards for a number of reasons, there is some evidence that heightened scrutiny by regulators had an impact on them during and after the Great Recession. Recent research quantifies the impact of tighter supervisory standards on total bank lending. A study by Bassett, Lee, and Spiller finds an elevated level of supervisory stringency during the most recent recession, based on an analysis of bank supervisory ratings. This research concludes that an increase in the level of stringency can have a statistically significant impact on total loans and loan capacity for several years—approximately 20 quarters—after the onset of the tighter supervisory standards.

It’s Not All about the Financial Crisis and the Great Recession

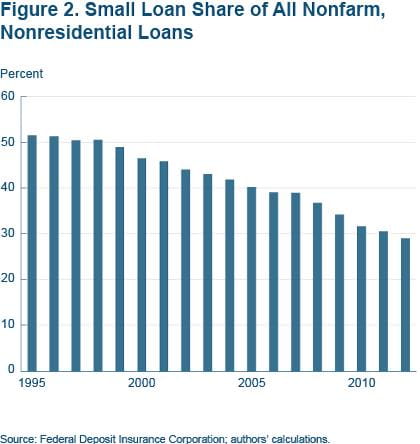

Recent declines in small business lending also reflect longer-term trends in financial markets. Banks have been exiting the small business loan market for over a decade. This realignment has led to a decline in the share of small business loans in banks’ portfolios. As figure 2 shows, the fraction of nonfarm, nonresidential loans of less than $1 million—a common proxy for small business lending—has declined steadily since 1998, dropping from 51 percent to 29 percent.

The 15-year-long consolidation of the banking industry has reduced the number of small banks, which are more likely to lend to small businesses. Moreover, increased competition in the banking sector has led bankers to move toward bigger, more profitable, loans. That has meant a decline in small business loans, which are less profitable (because they are banker-time intensive, are more difficult to automate, have higher costs to underwrite and service, and are more difficult to securitize).

Conclusion

No one disputes the decline in the amount of small business credit since the financial crisis and Great Recession. The most recently available data put the inflation-adjusted value of small commercial and industrial loans at less than 80 percent of their 2007 levels.

While bankers, small business owners, and regulators all point to different sources for the drop in small business credit, a careful analysis of the data suggests that a multitude of factors explain this decline in credit.

The factors unleashed by the financial crisis and Great Recession added to a longer-term trend. Banks have been shifting activity away from the small business credit market since the late 1990s, as they have consolidated and sought out more profitable sectors of the credit market.

Small business demand for lending has shrunk, as fewer small businesses have sought to expand. Credit has also become harder for small businesses to obtain. A combination of reduced creditworthiness, the declining value of homes (a major source of small business loan collateral), and tightened lending standards has reduced the number of small companies able to tap credit markets.

This confluence of events makes it unlikely that small business credit will spontaneously increase anytime in the near future. Given the contribution that small businesses make to employment and economic activity, policymakers may want to intervene to ensure that small business owners can access the credit they need to operate effectively. When considering means of intervention, however, it is important for policymakers to understand and take into account the multiple factors affecting small business credit. Any proposed solution needs to consider the combined effect of these factors.

Footnote

- For purposes of this discussion, we will focus on traditional commercial bank lending, as it is the most frequently utilized source of small business credit. According to a 2011 survey by the National Federation of Independent Businesses, 85 percent of businesses reported that a commercial bank was their primary financial institution, while only 5 percent has such a relationship with a nondepository financial institution (such as private finance companies). Furthermore, loans guaranteed by the Small Business Administration, while clearly important to some businesses, continue to comprise just over 1 percent of all small business loans. Return to 1

References

- “Income, Poverty, and Health Insurance Coverage in the United States: 2010,” Carmen DeNavas-Walt, Bernadette D. Proctor, and Jessica C. Smith, 2011. Current Population Reports: Consumer Incomes, U.S. Bureau of the Census.

- “Estimating Changes in Supervisory Standards and Their Economic Effects,” William F. Bassett, Seung Jung Lee, and Thomas W. Spiller. Federal Reserve Board, Divisions of Research and Statistics and Monetary Affairs, Finance and Economics Discussion Series, no. 2012-55.

Suggested Citation

Wiersch, Ann Marie, and Scott Shane. 2013. “Why Small Business Lending Isn’t What It Used to Be.” Federal Reserve Bank of Cleveland, Economic Commentary 2013-10. https://doi.org/10.26509/frbc-ec-201310

This work by Federal Reserve Bank of Cleveland is licensed under Creative Commons Attribution-NonCommercial 4.0 International