- Share

Some people who don’t use banks still see value in them – and say alternatives aren’t perfect substitutes

People who use banks rarely or not at all sometimes still see value in banking relationships – and don’t see alternatives as perfect substitutes, according to a new Cleveland Fed report.

The report summarizes the results of focus groups consisting of 36 unbanked and underbanked individuals in Cleveland and Houston, where they discussed how they manage their finances and their views toward banks and other financial service providers.

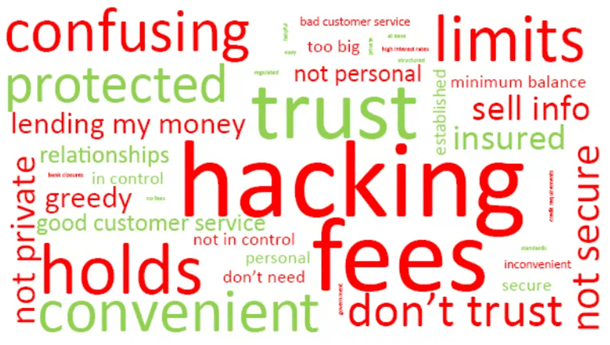

Several participants “placed a high value on having relationships with banks, believing that such relationships could improve their access to credit,” according to the report.

“If you have good credit with a bank,” one participant said, “you have good credit anywhere.”

Several focus group members appreciated the convenience of bank locations and ATMs. Some also viewed bank accounts as more secure than alternative financial services.

Still, many participants still voiced concerns about cybersecurity and overdraft charges, contributing to an overall negative sentiment toward banks.

One participant described how fees can pile up.

"For the first three days they charge $7, and then after that, it was just $35 each day, each day, each day."

Participants’ Views on Banks, Represented as a Word Cloud:

Beyond banks

Many participants used prepaid cards and appreciated their low and transparent fees, but some noted that they aren’t accepted everywhere, especially if they lack a chip. One participant recalled being approved for a furniture loan online, only to be rejected at the last step because their prepaid card wasn’t tied to a bank.

"They said you can't use that kind of card.”

Participants highlighted the convenience of fintech tools and apps, especially for peer-to-peer transfers. Still, hacking was a common concern, and such tools also aren’t accepted everywhere. Some said app providers lack good customer service.

“They basically put their hands up and say, ‘I don’t know what to tell you.’”

The full report also provides insights related to how unbanked and underbanked individuals use cash, money orders, check-cashing services and more.

Read the Economic Commentary: The Accounts of the Unbanked and Underbanked

Federal Reserve Bank of Cleveland

The Federal Reserve Bank of Cleveland is one of 12 regional Reserve Banks that along with the Board of Governors in Washington DC comprise the Federal Reserve System. Part of the US central bank, the Cleveland Fed participates in the formulation of our nation’s monetary policy, supervises banking organizations, provides payment and other services to financial institutions and to the US Treasury, and performs many activities that support Federal Reserve operations System-wide. In addition, the Bank supports the well-being of communities across the Fourth Federal Reserve District through a wide array of research, outreach, and educational activities.

The Cleveland Fed, with branches in Cincinnati and Pittsburgh, serves an area that comprises Ohio, western Pennsylvania, eastern Kentucky, and the northern panhandle of West Virginia.

Media contact

Chuck Soder, chuck.soder@clev.frb.org, 216.672.2798