- Share

A Real-Time Assessment of Inflation Nowcasting at the Cleveland Fed

The views authors express in Economic Commentary are theirs and not necessarily those of the Federal Reserve Bank of Cleveland or the Board of Governors of the Federal Reserve System. The series editor is Tasia Hane. This paper and its data are subject to revision; please visit clevelandfed.org for updates.

Real-time tracking of inflation developments is important because inflation influences the behavior of everyone participating in an economy. When making decisions, consumers and businesses may have to forecast the inflation rate far into the future, but inflation tends to be difficult to predict accurately. However, some recent research finds that model-based forecasts of inflation over the next several years can be improved by incorporating more-accurate estimates of where inflation is likely to be in the near term.1 These inflation “nowcasts” thus serve as an important jumping-off point for modeling how inflation is likely to behave over a longer period.

In 2013, we developed a model to produce daily nowcasts of various inflation measures. The model nowcasts US headline and core inflation as measured by the Consumer Price Index (CPI) and the price index for personal consumption expenditures (PCE).2 The nowcast estimates are updated every business day and are made available on the Cleveland Fed’s public website at clevelandfed.org/indicators-and-data/inflation-nowcasting. This and other inflation-related indicators on the website are part of the content provided by the Bank’s Center for Inflation Research to inform policymakers, researchers, and the public about inflation.

In this Commentary, we examine and compare the nowcasting accuracy of the headline and core inflation estimates coming from our model and published on the Cleveland Fed’s website to the accuracy of nowcasts coming from competing sources, which include alternative statistical models and surveys of professional forecasters, in particular, the Blue Chip Economic Indicators Survey and the Federal Reserve Bank of Philadelphia’s Survey of Professional Forecasters (SPF). We evaluate inflation nowcasting accuracy over a long sample spanning 1999:Q2 through 2022:Q4 and a shorter sample spanning the period since the onset of the COVID-19 pandemic, a period associated with very high economic uncertainty and volatile movements in economic variables, including inflation.3

While past performance does not guarantee future results, we find that our inflation nowcasting model has performed relatively well during both sample periods. Compared with alternative statistical models, our model has historically been more accurate for headline inflation, and the model’s accuracy has been similar to that of other statistical models for core inflation. When we compare our model’s performance with that of professional forecasters, our model has been relatively more accurate than the inflation nowcasts coming from the Blue Chip consensus and the SPF. While nowcasting errors have increased in absolute size since the onset of the pandemic, our inflation nowcasting model has tended to outperform survey estimates even during this recent period. These results are noteworthy because when making forecasts, professional forecasters can and do use a range of models and expert judgment to capture the special factors that affect near-term inflation trends.4

A Summary of Our Inflation Nowcasting Model

In a nutshell, there are five parts to our model. The first part nowcasts core inflation; these nowcasts are generated by forecasting that core inflation in coming months will be equal to its average reading over the prior 12 months. The second part nowcasts food price inflation; we follow the approach used for core inflation. The third part nowcasts gasoline price inflation based on a combination of current gasoline prices and current oil prices, under the assumption that today’s oil prices are informative about where gasoline prices are likely to head in the future. The fourth part combines the nowcasts of core inflation, food price inflation, and gasoline price inflation to produce nowcasts of inflation in either the CPI or PCE price index. Finally, the fifth part takes into account timing lags between the release of CPI and PCE inflation by converting the former to the latter in cases in which CPI inflation has been released but PCE inflation has not. For an accessible description of the model, see the Frequently Asked Questions portion of the Cleveland Fed’s inflation nowcasting website; for technical details, see Knotek and Zaman (2017).

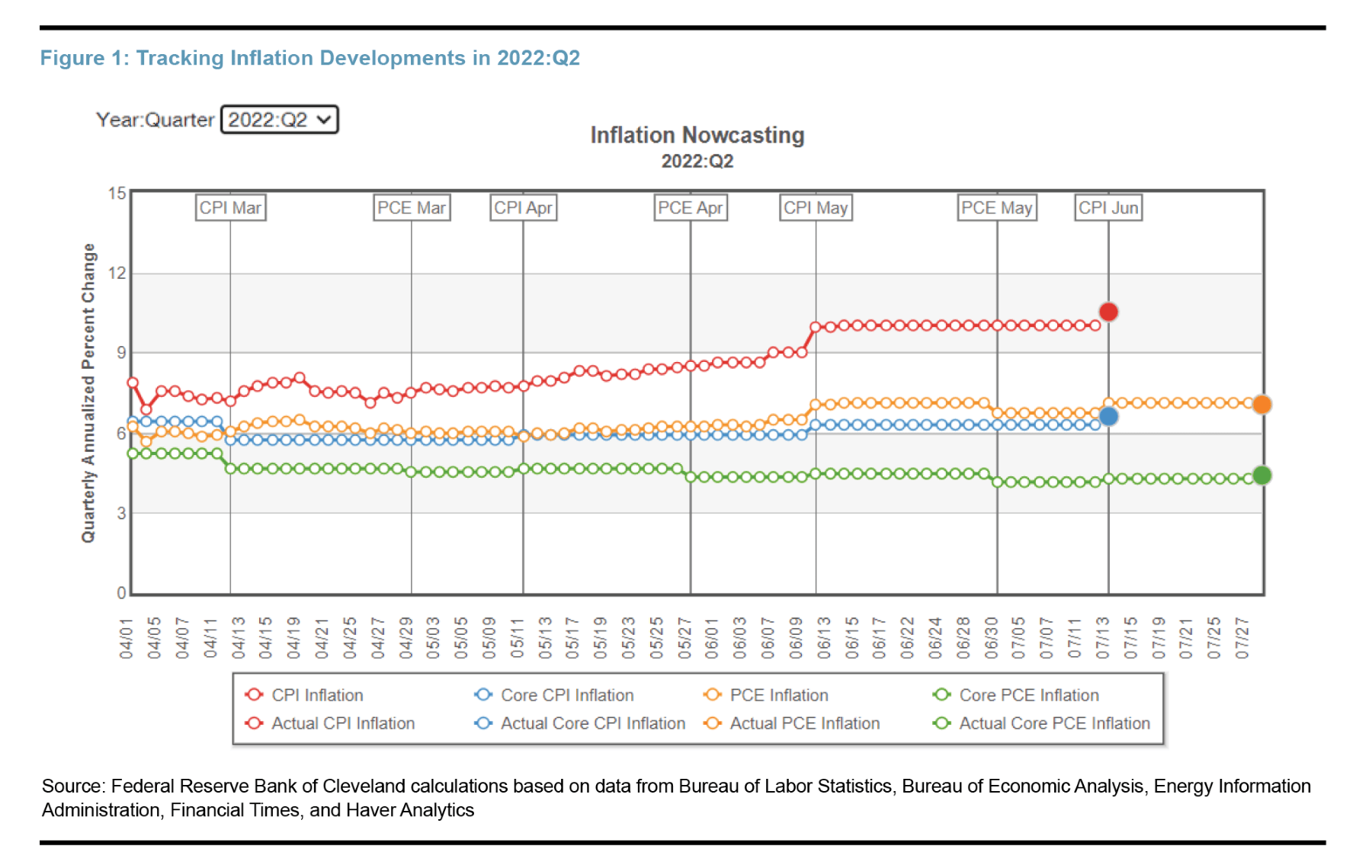

The Evolution of Inflation Nowcasts in 2022:Q2

To give a sense of the evolving nature of the nowcast estimates, Figure 1 plots the evolution of the inflation nowcast estimates for 2022:Q2. The figure has four lines corresponding to the four inflation measures. Also included are the actual quarterly realizations, shown as solid dots and vertical lines to indicate the official releases of monthly CPI and PCE inflation data.

As soon as the quarter began on April 1, the model began producing nowcast estimates for the quarter. Once the data for the third month of the quarter were released, the model stopped producing nowcasts for that quarter because we had the complete quarterly data for the target quarter. Because CPI data are released roughly two weeks before the release of PCE data, the CPI nowcasts for the target quarter end two weeks earlier than those for PCE inflation. Within the quarter, the nowcast estimates changed when new data arrived that were different than what was expected.

Core inflation nowcasts use very few data sources, and these arrive infrequently; therefore, the core inflation nowcasts change infrequently. Nowcasts of core CPI inflation are based on past core CPI inflation only; thus, the nowcasts change only when new monthly CPI data are released (or when past data are revised). If the data come in exactly as expected, then the core CPI inflation nowcasts will not change.

Nowcasts of core PCE inflation are based on either past core PCE inflation or core CPI data for the most recent month if those data are more timely than the PCE data. Thus, core PCE nowcasts change only when we get new data on either the CPI or the PCE price index; but, again, if the data come in exactly as expected, the nowcasts will not change. In general, core inflation tends to be relatively slow moving, so revisions to core inflation nowcasts are often small.

The headline inflation nowcasts can change when new CPI or PCE price index data are released, but they can also change between those release dates based on fluctuations in gasoline prices, which are a key driver of high-frequency headline inflation. Gasoline price nowcasts depend on oil prices, and because oil prices fluctuate almost every day, some of that volatility is passed through to headline inflation nowcasts. For example, on April 1, our model nowcasted CPI inflation of 7.9 percent for 2022:Q2. Over time, the nowcast estimate moved up gradually, reaching 10.0 percent by July 12, a day before the release of the CPI data for the last month of the quarter, completing the Q2 CPI data. The data indicated that CPI inflation was 10.5 percent at a quarterly annualized rate, a number which implies a prediction error of 0.5 percentage points when evaluated using the last nowcast and a much bigger error of 2.6 percentage points when evaluated using the estimate produced at the beginning of the quarter.

In the case of core CPI inflation, the nowcast estimate changed very little over the period shown, from 6.4 percent (April 1) to 6.3 percent (July 12), and with the actual data coming in at 6.6 percent, the prediction errors were 0.2 and 0.3 percentage points, respectively. Our results share a common finding with those in the nowcasting literature that, on average, nowcasts made with more information later in a month or quarter tend to be more accurate than those made early in a month or quarter.

Historical Performance Accuracy: Our Model versus Competing Statistical Models

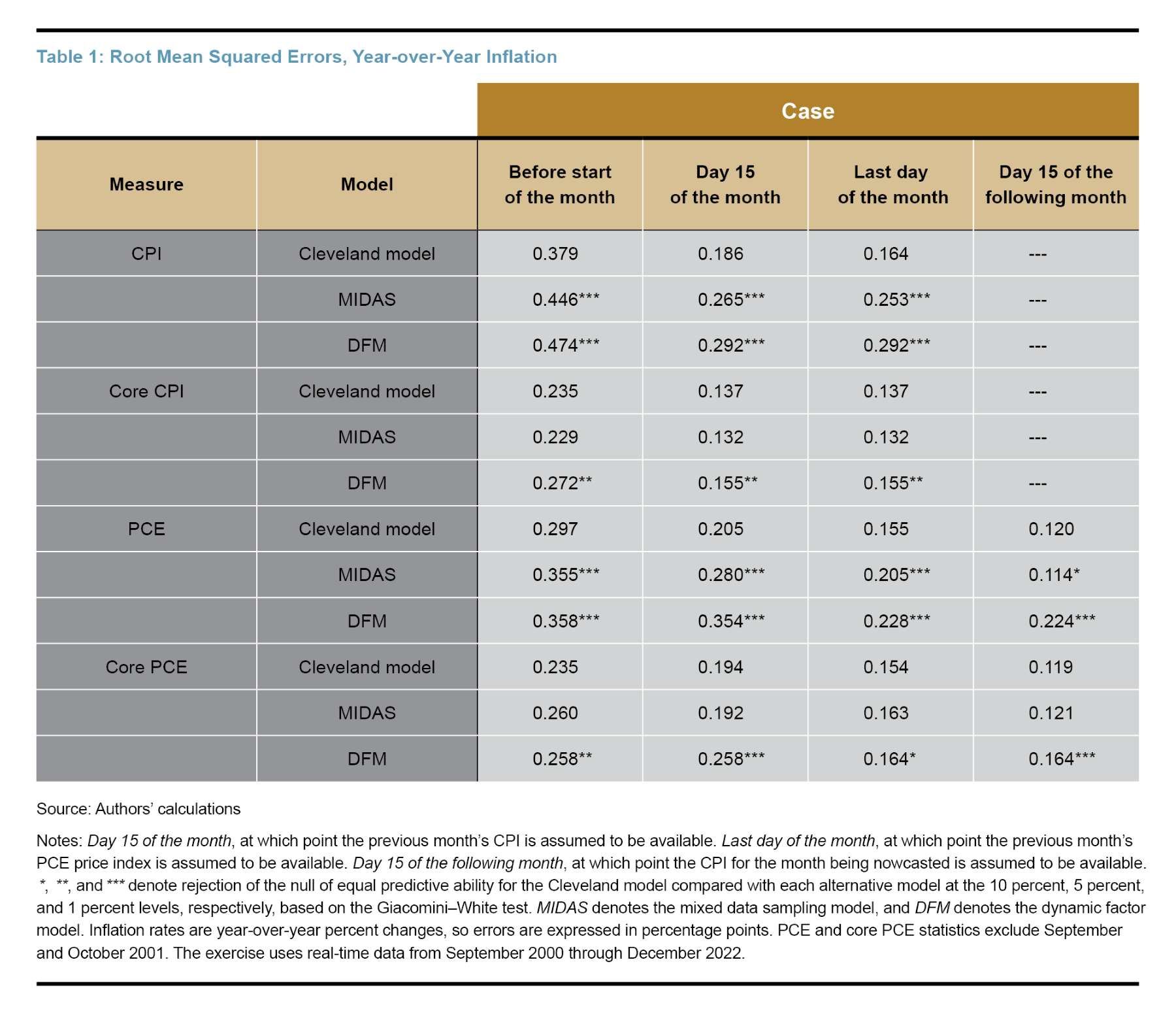

Following Knotek and Zaman (2017), we compare the nowcast accuracy of our model to other popular mixed-frequency statistical models: mixed-data sampling (MIDAS) models and dynamic factor models (DFM). Table 1 reports the (point) nowcasting accuracy of year-over-year inflation projections in terms of root mean squared errors (RMSEs) of our model and the MIDAS and DFM models.5 The smaller the RMSE, the more accurate the nowcast estimate.

Predictive accuracy is shown for four representative cases to capture typical nowcast accuracy at different points over the course of a month, reflecting evolving information sets resulting from the incoming information flow used to compute the nowcasts. Case 1 occurs right before the start of the month; Case 2, day 15 of the target month; Case 3, the last day of the target month; and Case 4, day 15 of the following month, at which point the CPI for the month being nowcasted is assumed to be available, and only PCE and core PCE inflation rates remain to be nowcasted.

For virtually all the cases, the RMSEs indicate that our model has historically generated more accurate headline inflation nowcasts than the other two competing statistical models. For headline CPI and PCE inflation, the reductions in RMSEs coming from our model compared with those coming from the competing models are substantial and statistically significant. In the case of core inflation, our model is very competitive with both the DFM and MIDAS models, a fact suggesting that there is little benefit from using these latter more sophisticated and computationally demanding models.

Nowcasting Accuracy Comparison with Blue Chip

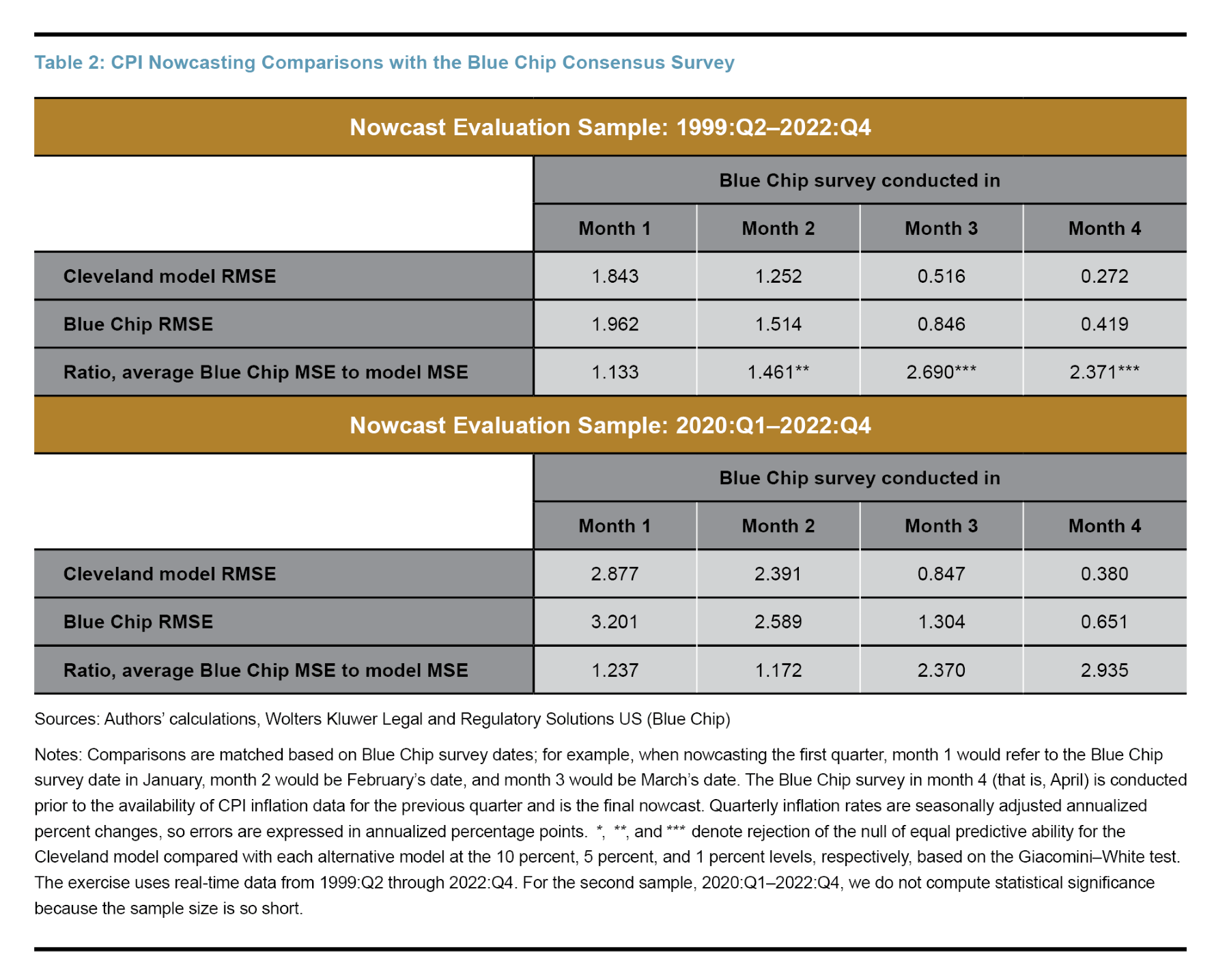

The Blue Chip Economic Indicators survey of private professional forecasters, published by Wolters Kluwer Legal and Regulatory Solutions US, provides forecasts of major US economic indicators, including quarterly CPI inflation. The Blue Chip survey is typically released around the 10th of each month, but the survey is conducted over an earlier two-day period that is usually mentioned in the release. We match this timing when comparing the nowcast accuracy between Blue Chip and our model.

Considering the timing of the Blue Chip survey and the publication of the CPI data, we compare Blue Chip nowcasting accuracy with the model at four different points in time for each quarter. For example, nowcasts of the second quarter are collected in the April, May, June, and July Blue Chip surveys. The July Blue Chip survey data are released about one to two weeks before the Bureau of Labor Statistics (BLS) releases all the data needed to compute quarterly CPI inflation.

Table 2 reports the RMSE accuracy comparison for the sample period spanning 1999:Q2 through 2022:Q4 (top panel). We also report results for a short sample spanning 2020:Q1 through 2022:Q4 (bottom panel) in order to investigate inflation nowcasting performance since the start of the pandemic. The results indicate the following.

First, as we move from month 1 (at the very beginning of the quarter) through month 4 (the survey from the month immediately following the quarter that is released right before the quarterly CPI data are available), we see sequential reductions in RMSEs for both our model and the Blue Chip consensus. This improved nowcast accuracy is due to accumulating information as we move from month 1 to month 4. Second, our model’s nowcasts have been more accurate on average than Blue Chip nowcasts across all four months, as demonstrated by smaller RMSEs. Third, the magnitude of the errors experienced since the onset of the pandemic is notably larger as evidenced by comparing RMSEs between the long and short evaluation samples, a finding which is consistent with inflation’s becoming more volatile and more difficult to forecast during the latter period. Nevertheless, our model’s inflation nowcasts have tended to be more accurate on average during this period.

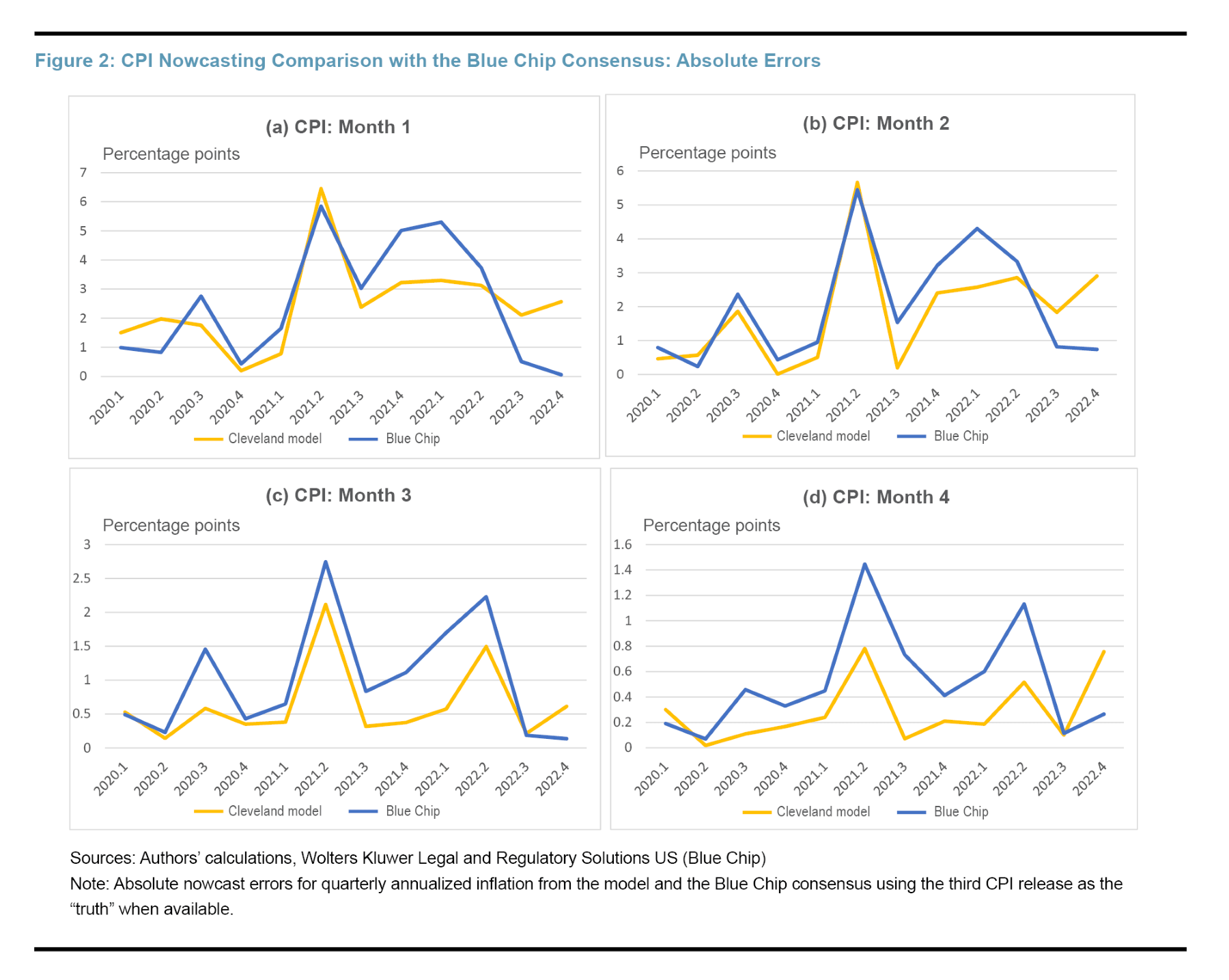

To provide a visual illustration of recent quarterly performance, Figure 2 plots the profiles of the absolute nowcast errors from our model and the Blue Chip consensus for the short sample since the beginning of the COVID-19 pandemic in 2020:Q1. The four panels in the figure correspond to months 1 through 4. Looking at the figure, two observations immediately stand out. First, moving from panels (a) through (d), the magnitude of the absolute errors decreases (as can be seen by the changing scale of the y-axis). Second, it is generally the case that our model nowcasts were more accurate than the Blue Chip consensus, with the notable exception of very recent quarters.

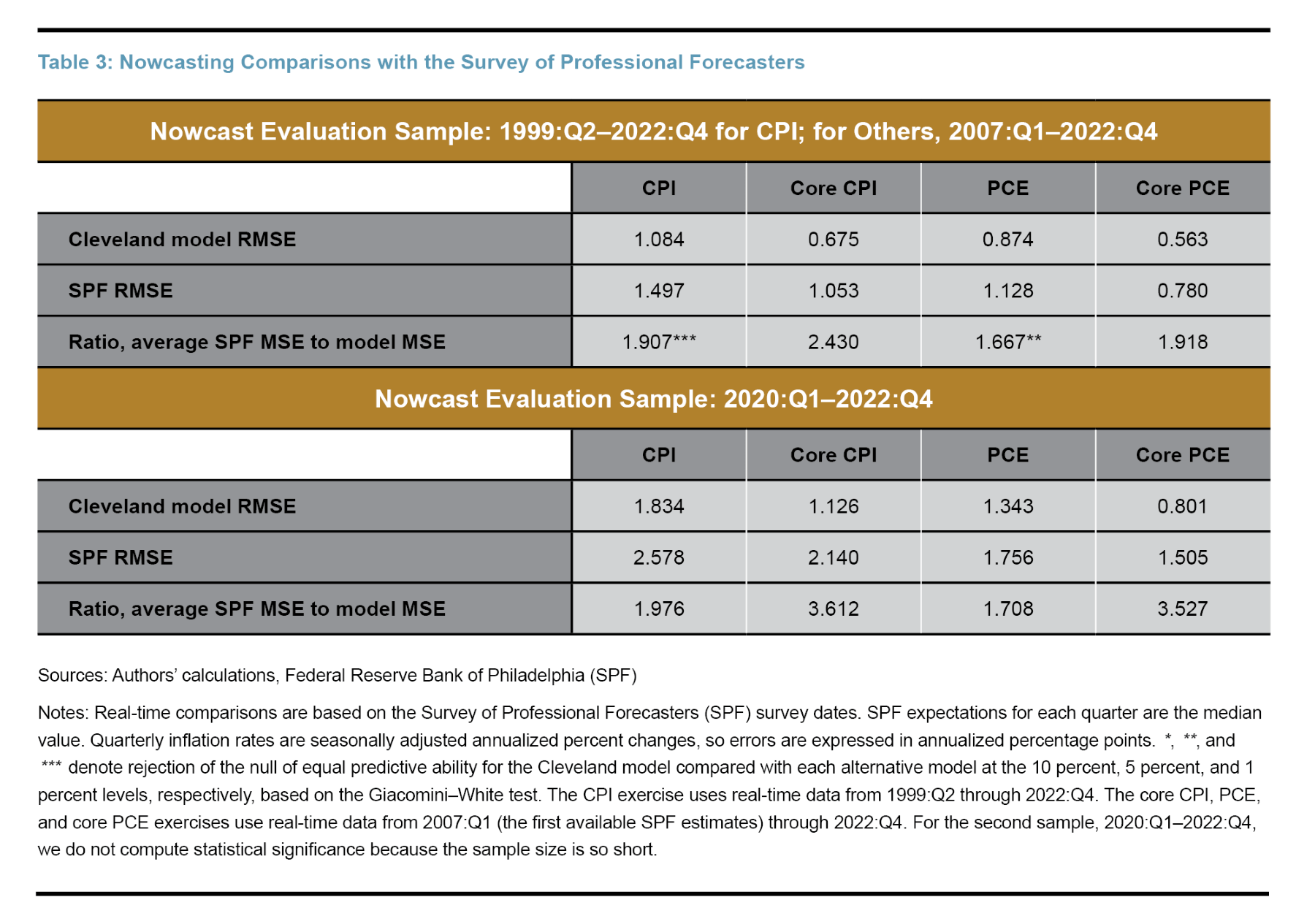

Nowcasting Accuracy Comparison with SPF

The SPF is a publicly available survey that is published quarterly and is released around the middle of the second month of the quarter. The Federal Reserve Bank of Philadelphia publishes the survey dates. These dates are about one week prior to the release date, so this timing means that SPF nowcasts of current-quarter inflation are made before the first monthly CPI reading for the quarter is released. To ensure that our model and SPF are on a level footing for this comparison exercise, we match the information sets that would have been available to the professional forecasters with the information set for our model.

The SPF has a long history of reporting CPI forecasts, and we perform CPI nowcast comparisons beginning in 1999:Q2. The SPF started reporting core CPI inflation, headline PCE inflation, and core PCE inflation in 2007:Q1; accordingly, we conduct comparisons with these three series starting at this point. The final quarter of comparison is 2022:Q4. To highlight the nowcasting comparison during the pandemic period, we also report accuracy results for the short sample. In line with much of the forecasting literature, we use the SPF median nowcasts.

Table 3 reports the results, comparing the nowcast accuracy of our model to that of SPF for all four inflation measures. As can be seen, when evaluated over the long sample, our model’s nowcasts for both headline CPI and PCE inflation outperform the accuracy of the SPF nowcasts by 0.41 percentage points and 0.25 percentage points on average, respectively. When evaluated over the short sample that includes the pandemic and the recent surge in inflation, the magnitudes of the accuracy gains from our model compared with those of the SPF are significantly larger, at 0.74 percentage points for headline CPI and 0.41 percentage points for headline PCE.

In the case of core inflation, our model has also tended to outperform the SPF nowcasts on average. This outperformance holds true over the long sample and has remained the case since the start of the pandemic.6

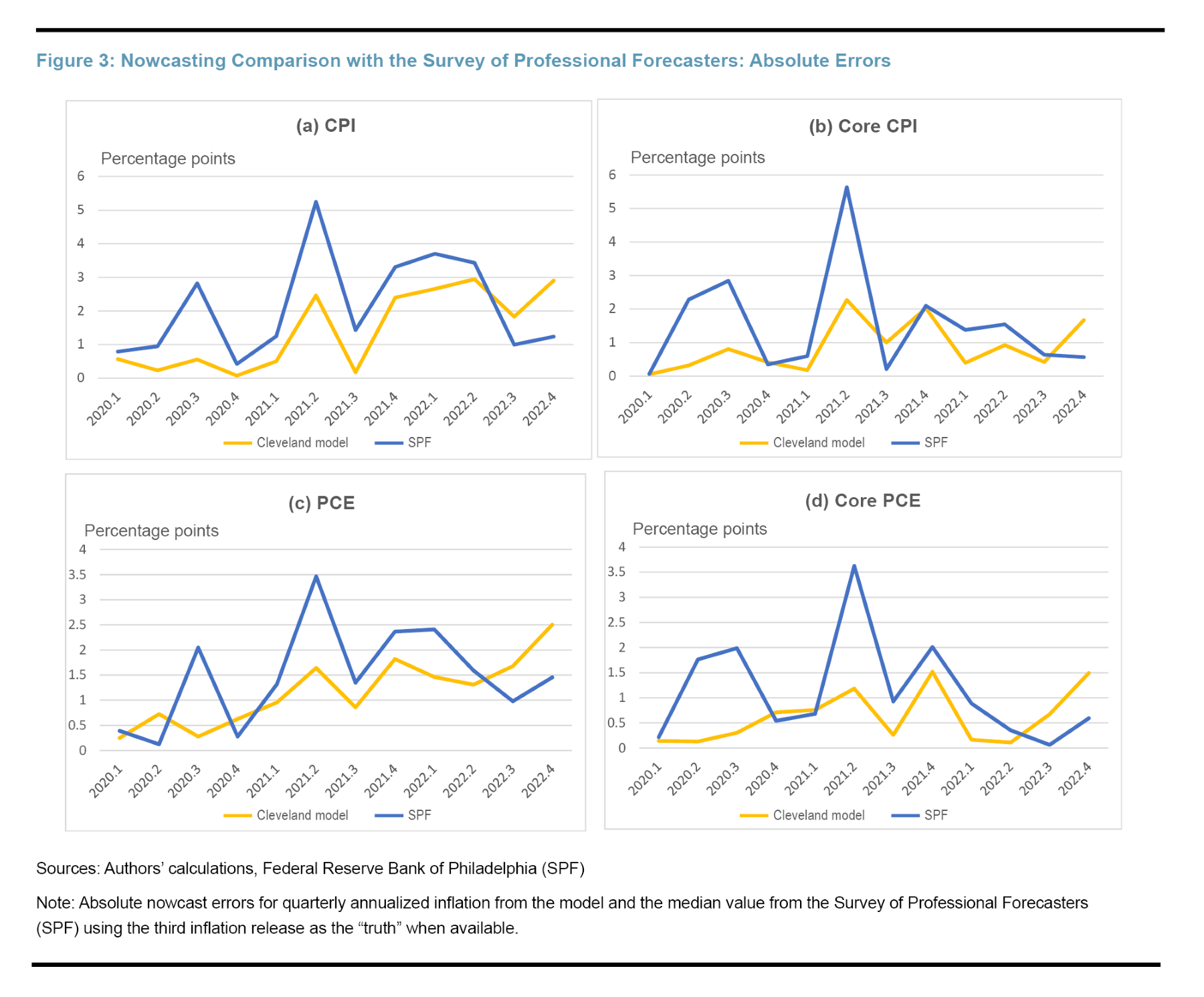

Figure 3 provides a visual illustration of nowcast performance since the onset of the pandemic. The four panels in the figure plot the absolute nowcast errors for CPI, core CPI, PCE, and core PCE inflation measures from our model and from the SPF. Early in the pandemic and as inflation began to move up in 2021 and early 2022, the inflation nowcasts from our model tended to be more accurate than those from the SPF; however, that relative performance reversed at the end of 2022 as inflation started showing signs of easing.

Conclusion

The Cleveland Fed’s website has been providing nowcast estimates of both headline and core inflation measures at a daily frequency since early 2014. This Commentary examines the historical predictive accuracy of the model behind the production of the Cleveland Fed inflation nowcasts compared with nowcasts from professional forecasters (via Blue Chip and the SPF) and competing statistical models. Compared with alternative statistical models, our model has historically been more accurate for headline inflation, with comparable accuracy for core inflation. Whether looking over a long sample starting in 1999 or a shorter sample starting with the onset of the COVID-19 pandemic, we find that inflation nowcasts coming from our model have historically tended to outperform those from professional forecasters.

Endnotes

- See Faust and Wright, 2013; Kruger et al., 2017; Knotek and Zaman, 2019; Tallman and Zaman, 2020. Return to 1

- Core inflation rates exclude movements in food and energy prices. The model reports seasonally adjusted, month-over-month inflation rates in the inflation measures (expressed as nonannualized percent changes) and quarterly inflation rates in these measures (expressed at seasonally adjusted annualized rates, or SAAR). The model also reports year-over-year inflation rates in these measures (based on nonseasonally adjusted data for CPI inflation and core CPI inflation and seasonally adjusted data for PCE inflation and core PCE inflation). Return to 2

- For the period 1999 through 2013:Q2, we compute the inflation nowcasts coming from our model using the real-time data that would have been available at each point in the past. For 2013:Q3 onward, we use the inflation nowcasts that were generated and published to the Cleveland Fed website in real time. Return to 3

- These findings are in line with the results in Knotek and Zaman (2017), who document the competitive point nowcast accuracy of this model over the evaluation sample spanning 1999:Q2 through 2015:Q2, and Knotek and Zaman (2022), who document the competitive density nowcast accuracy of this model over the same evaluation sample. Return to 4

- We use the third monthly estimate of PCE and CPI prices as the actual value, that is, the truth, except for the final observations, corresponding to November and December 2022, for which we use the second and first monthly estimates, respectively. Return to 5

- However, the nowcast improvements for core inflation are not statistically significant according to the Giacomini–White test. Return to 6

References

- Faust, Jon, and Jonathan H. Wright. 2013. “Forecasting Inflation.” In Handbook of Economic Forecasting, edited by G. Elliott and A. Timmermann, 2, Part A:2–56. Elsevier. https://doi.org/10.1016/B978-0-444-53683-9.00001-3.

- Knotek II, Edward S., and Saeed Zaman. 2017. “Nowcasting U.S. Headline and Core Inflation.” Journal of Money, Credit and Banking 49 (5): 931–68. https://doi.org/10.1111/jmcb.12401.

- Knotek II, Edward S., and Saeed Zaman. 2019. “Financial Nowcasts and Their Usefulness in Macroeconomic Forecasting.” International Journal of Forecasting 35 (4): 1708–24. https://doi.org/10.1016/j.ijforecast.2018.10.012.

- Knotek II, Edward S., and Saeed Zaman. 2022. “Real-Time Density Nowcasts of US Inflation: A Model Combination Approach.” International Journal of Forecasting, October, S0169207022000589. https://doi.org/10.1016/j.ijforecast.2022.04.007.

- Krüger, Fabian, Todd E. Clark, and Francesco Ravazzolo. 2017. “Using Entropic Tilting to Combine BVAR Forecasts With External Nowcasts.” Journal of Business & Economic Statistics 35 (3): 470–85. https://doi.org/10.1080/07350015.2015.1087856.

- Tallman, Ellis W., and Saeed Zaman. 2020. “Combining Survey Long-Run Forecasts and Nowcasts with BVAR Forecasts Using Relative Entropy.” International Journal of Forecasting 36 (2): 373–98. https://doi.org/10.1016/j.ijforecast.2019.04.024.

Suggested Citation

Knotek, Edward S., II, and Saeed Zaman. 2023. “A Real-Time Assessment of Inflation Nowcasting at the Cleveland Fed.” Federal Reserve Bank of Cleveland, Economic Commentary 2023-06. https://doi.org/10.26509/frbc-ec-202306

This work by Federal Reserve Bank of Cleveland is licensed under Creative Commons Attribution-NonCommercial 4.0 International