- Share

How Large Are the American Rescue Plan Fund Distributions to State and Local Governments?

The views authors express in District Data Briefs are theirs and not necessarily those of the Federal Reserve Bank of Cleveland or the Board of Governors of the Federal Reserve System. The series editor is Harrison Markel.

Download the merged SLFRF and COG data to find your state and local governments' ratio.

In March of this year, the American Rescue Plan (ARP) authorized the US Department of the Treasury to distribute $350 billion to state and local governments through the legislation’s Coronavirus State and Local Fiscal Recovery Funds (SLFRF) to help speed the nation’s economic recovery from the COVID-19 pandemic. Since then, candidates and advocates have stepped forward to say what community challenges they will solve with the funds. When we hear that a county is receiving $500 million and a state is receiving $5 billion, both figures sound very large, but what we don’t know is how much change those allocations can create. To ground this conversation, we are providing a list of all of the planned allocations scaled by the receiving jurisdiction’s annual tax revenue. Most of us are familiar with the taxes we pay to state and local governments each year and the programs that those taxes are able to support. Scaling by our state or local government’s annual tax revenue enables us to consider whether our SLFRF allocation could be transformational or merely helpful. Once the total funds are divided over at least 4,000 recipients, they range from modest sums of less than 10 percent of the local government’s tax revenue, which may offset some collections lost during lockdowns, to values well over 100 percent, an amount that could create a once-in-a-generation opportunity to invest more than an entire year’s worth of tax revenue without taking on new debt.

The SLFRF allocations will not be distributed evenly across all communities. State allocations are based on each state’s unemployment rate during the pandemic (US Treasury, 2021e). County funds are allocated on a per capita basis unless the per capita amount is less than the amount the county would receive under the Community Development Block Grant (CDBG) formula (US Treasury, 2021c). City funds are allocated based solely on the CDBG formula (US Treasury, 2021d). The total allocation for each local government is being distributed over two years, with the first half disbursed in May 2021, and the second half disbursed a year later. The ratios we report include the sum of the SLFRF money to be distributed rather than only the first year’s amount. Recipients must spend the funds by the end of 2024.

The recipient governments are allowed to use the funds for several purposes, including replacing tax revenue lost because of the pandemic; making grants to households, businesses, and nonprofit organizations impacted by the pandemic; increasing pay to essential staff that worked during the pandemic; or investing in public health, water, or broadband infrastructure (US Treasury, 2021b). While these authorized uses are quite broad (much broader than those of the CARES Act funds), the SLFRF money is not completely unrestricted. The US Treasury can force repayment if the funds are used for something other than the authorized uses, such as a project proposed before 2020 that has no connection to the pandemic recovery. The ARP stated that the funds could not be used to enable tax cuts by replacing revenue a recipient would have collected despite the pandemic. However, guidance issued by the US Treasury allowed for some leeway because the net impact of tax code changes is not perfectly predictable (Auxier, 2021). Several states, including Ohio, Kentucky, and West Virginia, have challenged the restriction on tax cuts in court, and some of the decisions have gone their way (Wu, 2021).

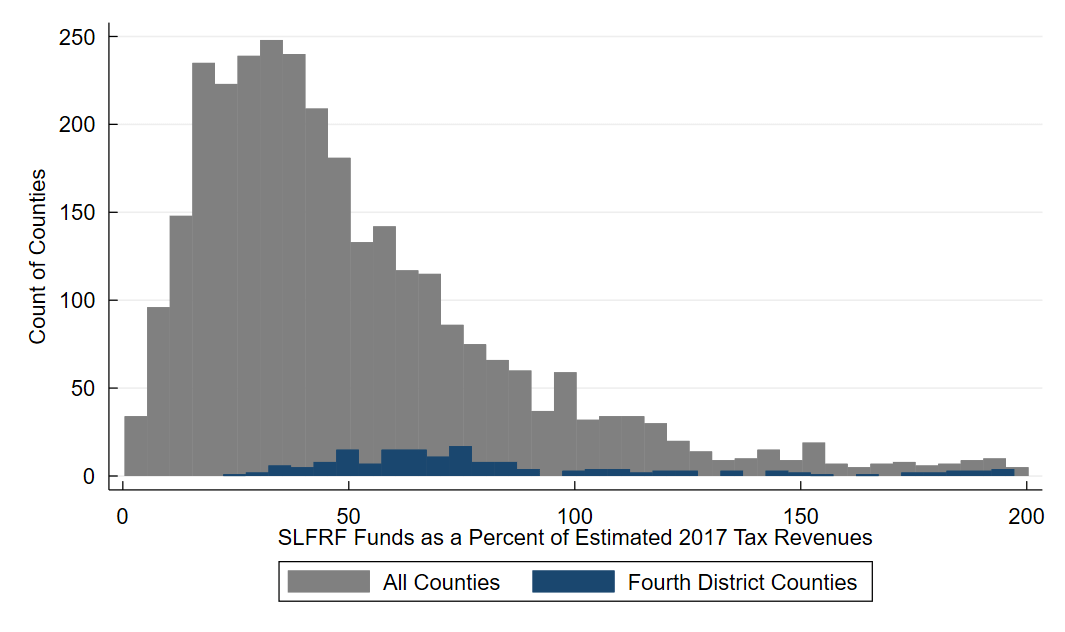

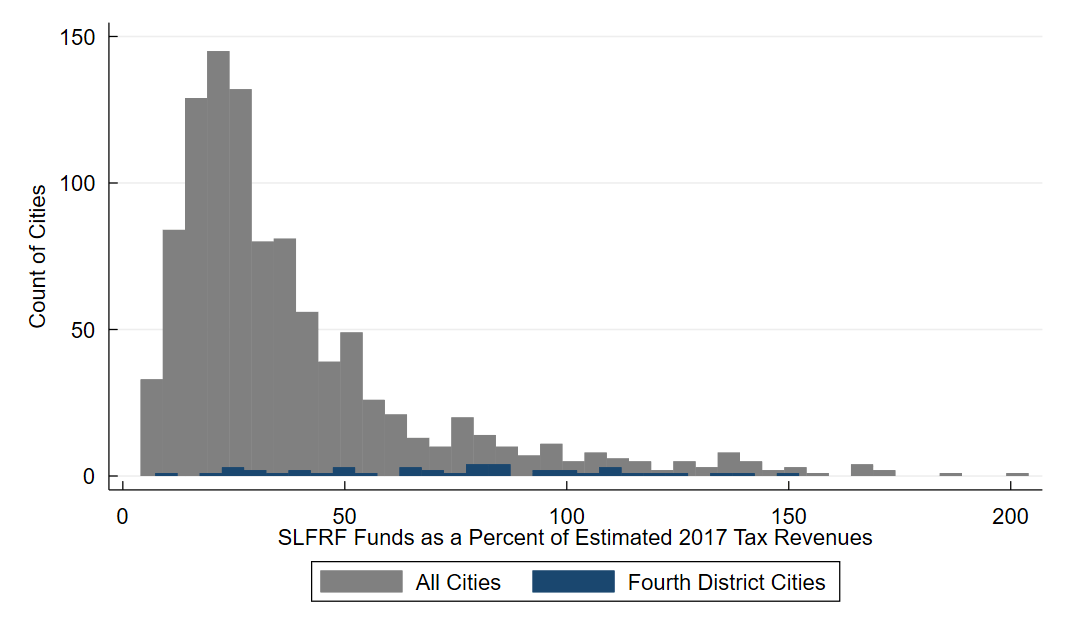

Table 1 presents summary statistics for the SLFRF allocations expressed as a percentage of annual tax revenue for all jurisdictions and separately for the Fourth District jurisdictions. Figures 1, 2, and 3 display the same distributions as histograms, in which the height of the bar represents the count of jurisdictions with percentages in the bar’s range. For a detailed description of how we estimated 2020 tax revenues and matched the individual jurisdictions, please see the appendix.

The median state is receiving SLFRF money equivalent to 20 percent of its annual tax revenue. Almost all states have ratios between 10 percent and 30 percent. The four unusually high values are for New Hampshire (36 percent), South Dakota (49 percent), Wyoming (51 percent), and Alaska (95 percent). Both Alaska and Wyoming suffered losses of severance tax revenue (taxes on oil production) during 2020, a situation that lowered their revenue denominator and raised their SLFRF-to-revenue ratios.

The Fourth District states’ allocations of SLFRF money as a share of tax revenues are right in the middle of the pack compared to other states. Ohio, Kentucky, and Pennsylvania are all receiving approximately 17 percent of their 2020 tax revenue. West Virginia will receive 24 percent of its 2020 tax revenue.

| Median | Mean | Standard Deviation | Count of Matched Jurisdictions |

|

|---|---|---|---|---|

| All States | 19.6 | 22.4 | 13.2 | 50 |

| All Counties | 38.2 | 45.7* | 33.4* | 3,103 |

| All Cities | 23.9 | 33.2* | 29.4* | 1,042 |

| Fourth District States | 17.2 | 18.8 | 3.6 | 4 |

| Fourth District Counties | 64.6 | 75.9* | 38.9* | 170 |

| Fourth District Cities | 70.2 | 67.9* | 35.2* | 46 |

Notes: The mean and standard deviation values with an asterisk (*) are calculated after trimming the top 2 percent of the values. When looking at the county or city SLFRF allocations expressed as a percent of tax revenue, it is important to keep in mind that some states fund counties or cities via intergovernmental transfers instead of taxes, or the state may only permit cities and counties to perform a very limited set of government functions. In these cases, the counties or cities would have relatively low tax revenues. This low denominator allows the SLFRF distributions to be a very high percentage of the tax revenue even if the SLFRF allocation is typical. To avoid having these unusual observations obscure the distribution, we have trimmed the top 2 percent of the percentages for counties and cities (all observations are included in the microdata file).

Sources: US Treasury, US Census Bureau, Quarterly Summary of State and Local Tax Revenue, and authors’ calculations.

For counties, the distribution of the ratio of SLFRF allocations to tax revenues is centered at a median of 38 percent. Five hundred forty-six counties will receive funds equal to more than 75 percent of their annual tax revenue, with 291 receiving more than 100 percent. Because the allocation formula is determined by population and the CDBG formula rather than any measure of county finances, there is nothing to limit it as a fraction of tax revenue or expenditures.

The distribution of SLFRF allocations as a proportion of estimated 2020 tax revenue for cities has a median of 24 percent. Of the 1,042 matched cities, 117 have an SLFRF allocations-to-tax-revenue ratio of more than 75 percent—72 of those are more than 100 percent.

The distribution of the SLFRF money relative to taxes for the Fourth District counties and cities is significantly higher than the national distribution. Both the median and the mean of the percentages of estimated 2020 revenue are 25 to 45 points higher than that of the national distribution. The CDBG formula, which is used for both the county and city allocations, is based on “several objective measures of community needs, including the extent of poverty, population, housing overcrowding, age of housing, and population growth lag in relationship to other metropolitan areas” (US Department of Housing and Urban Development, 2021). The formula directs relatively high levels of funding to counties and cities in the Fourth District because our District includes several areas with relatively high poverty, old housing stock, and slow-growing populations.

Since the pandemic began, we have seen multiple federal appropriations of unprecedented scale to help individuals, firms, and nonprofits endure economic disruption. The magnitude of the total funds for state and local governments in the SLFRF, $350 billion, is also extremely large for a one-time program. Through the scaling exercise conducted here, we can see that the huge top line translates into the equivalent of four months’ worth of tax revenue for the median recipient. A few hundred counties and cities with high poverty rates and slow population growth will receive over 12 months of revenue and have an opportunity to greatly accelerate their recovery or make a major investment.

References

- Auxier, Richard C. 2021. “Treasury Will Allow States to Take ARP Funds and Cut Taxes, With Some Guardrails.” TaxVox (blog). May 13, 2021. https://www.taxpolicycenter.org/taxvox/treasury-will-allow-states-take-arp-funds-and-cut-taxes-some-guardrails.

- Peter G. Peterson Foundation. 2021. “Why Do States Receive Different Amounts of Federal COVID Aid?” PGPF Blog (blog). April 19, 2021. https://www.pgpf.org/blog/2021/04/why-do-states-receive-different-amounts-of-federal-covid-aid.

- Rosewicz, Barb, Mike Maciag, and Melissa Maynard. 2021. “How Far American Rescue Plan Dollars Will Stretch Varies by State.” Pew Charitable Trusts. June 28, 2021. https://pew.org/35PDhPp.

- Schultz, Laura. 2021. “The American Rescue Plan Act: State and Local Funding Breakdown.” Rockefeller Institute of Government (blog). March 24, 2021. https://rockinst.org/blog/the-american-rescue-plan-act-state-and-local-funding-breakdown/.

- State Policy Network. 2021. “The American Rescue Plan: An Analysis of Proposed Federal Funds Distribution to the States.” SPN Blog (blog). March 2, 2021. https://spn.org/blog/state-covid-aid-american-rescue-plan/.

- US Census Bureau. 2017. “2017 State and Local Government Finances Datasets and Tables.” https://www.census.gov/programs-surveys/gov-finances/data/datasets.html.

- US Department of Housing and Urban Development. 2021. “Community Development Block Grant Program.” June 8, 2021. https://www.hud.gov/program_offices/comm_planning/cdbg.

- US Department of the Treasury. 2021a. “Coronavirus State and Local Fiscal Recovery Funds.” https://home.treasury.gov/policy-issues/coronavirus/assistance-for-state-local-and-tribal-governments/state-and-local-fiscal-recovery-funds.

- US Department of the Treasury. 2021b. “Coronavirus State and Local Fiscal Recovery Funds.” Federal Register 86 No. 26786. May 17. https://www.federalregister.gov/documents/2021/05/17/2021-10283/coronavirus-state-and-local-fiscal-recovery-funds.

- US Department of the Treasury. 2021c. “Coronavirus State and Local Fiscal Recovery Funds Allocations to Counties.” May 10. https://home.treasury.gov/system/files/136/Allocation-Methodology-for-Counties-508A.pdf.

- US Department of the Treasury. 2021d. “Coronavirus State and Local Fiscal Recovery Funds Allocations to Metropolitan Cities.” May 10. https://home.treasury.gov/system/files/136/Allocation-Methodology-for-MetropolitanCities-508A.pdf.

- US Department of the Treasury. 2021e. “Coronavirus State and Local Fiscal Recovery Funds Allocations to State Governments.” May 10. https://home.treasury.gov/system/files/136/Allocation-Methodology-for-States-508A.pdf.

- Walczak, Jared. 2021. “State and Local Aid in the American Rescue Plan Act.” Tax Foundation (blog). March 3, 2021. https://taxfoundation.org/state-and-local-aid-american-rescue-plan/.

- Wu, Titus. 2021. “Judge: Feds Can’t Prohibit Ohio’s Use of COVID-19 Relief Funds for Tax Cuts.” The Columbus Dispatch, July 2, 2021, sec. Politics. https://www.dispatch.com/story/news/politics/2021/07/02/ohio-attorney-general-dave-yost-wins-against-biden-rule-prohibiting-tax-cuts-covid-19-district-court/7843159002/.

Appendix: Estimating and Matching Methodology

The most recent complete data on state and local government finances are the 2017 Census of Governments (COG) (US Census Bureau, 2017). These data are collected from jurisdictions after jurisdictions have completed their comprehensive annual financial reports (CAFRs), and each stream of revenue and type of expenditure is reported as a line item in the COG data. We use the sum of the categories corresponding to tax revenues, such as property and sales taxes, to provide a sense of scale and put the SLFRF dollar amounts in context. To create an estimate of recent tax revenue for local governments, we increase the 2017 values by the growth observed for each type of tax by the local government’s state government. State government revenue data are collected much more frequently because there are comparatively few states (50), but there are many more county-level governments (3,143) and city-level governments (35,602). State revenue figures are collected quarterly and released within a few months of the end of each quarter. For each state, we divided the revenue recorded for each type of tax in 2020 by the revenue recorded for the same type of tax in 2017. We then multiplied this growth ratio by the 2017 revenue of the same type for all local jurisdictions in the state to estimate local governments’ 2020 tax revenues. We used calendar year totals of the state revenues. The local government data reflect fiscal year 2017, which matches the calendar year for many, but not all, local governments.

We obtained data on SLFRF allocations to state and local governments from the Coronavirus State and Local Fiscal Recovery Funds (US Treasury, 2021a). We merged the US Treasury allocation data with our estimate of 2020 tax revenue for local governments by matching government entities in both data sets with the same name and state. SLFRF money is being allocated to all 50 states, 3,119 counties and county equivalents, and 1,152 cities. An additional $19.5 billion will be distributed to the states to pass on to cities that did not qualify for an allocation under the CDBG formula. The states will decide how to allocate this money to individual cities, so the US Treasury data do not provide dollar values for these jurisdictions.

For each of the successfully matched local governments with an estimated 2020 revenue value and an SLFRF allocation value, we divided the allocation by the 2020 revenue estimate. For the state governments, we use the actual revenues during the 2020 calendar year. There are many merged city-county governments. The revenue and SLFRF amounts were summed before calculating their ratio. If the COG reported revenue at both levels, or for the county only, these observations are categorized as counties. A few have revenue reported in the COG at the city level only, but they are also receiving county SLFRF money. These observations appear as cities.

There are 91 counties or county-equivalent governments that are in US territories rather than states. We did not attempt to match these. Also, there are 46 counties in states where the state does not allow counties to perform any general-government functions. The total of these counties’ allocations was given to the states to disburse as the state chooses. We did not match these observations because we do not know how the states will divide the funds.

Some states do not collect certain types of taxes, so we had to impute a growth ratio to apply to their local governments’ revenues. For the states that did collect these taxes, we regressed the observed growth ratios on indicators for the state and the type of tax. We replaced the missing values with ratios predicted by the regression and then used these imputed growth ratios to raise the local government’s 2017 revenue figures up to 2020 estimates.

The estimation of 2020 tax revenues depends on some assumptions that probably do not hold in many cases. For example, if a city raised its sales tax rate between 2017 and 2020 but the state kept its rate unchanged, the growth in revenue will be underestimated for that city. For those who would prefer comparing the SLFRF allocations to older revenue data with no model adjustment, we have also provided a ratio of the SLFRF money to the COG 2017 revenue value. In Table A1 and Figures A1 and A2, we present the summary statistics and distributions of these ratios.

| Median | Mean | Standard Deviation | Count of Matched Jurisdictions |

|

|---|---|---|---|---|

| Counties | 51.6 | 41.8* | 36.8* | 3,041 |

| Cities | 38.7 | 28.5* | 30.7* | 1,023 |

Note: The mean and standard deviation values with an asterisk (*) are calculated after trimming the top 2 percent of the values.

Sources: US Treasury, US Census Bureau, Quarterly Summary of State and Local Tax Revenue, and authors’ calculations.

Note: For readability, the 70 observations above 200 percent are not plotted. Each bin of the histogram counts counties in a 5 percentage-point span.

Sources: US Treasury, US Census Bureau, Quarterly Summary of State and Local Tax Revenue, and authors’ calculations.

Note: For readability, the 22 observations above 200 percent are not plotted. Each bin of the histogram counts cities in a 5 percentage-point span.

Sources: US Treasury, US Census Bureau, Quarterly Summary of State and Local Tax Revenue, and authors’ calculations.

Suggested Citation

Whitaker, Stephan D., and Grant Rosenberger. 2021. “How Large Are the American Rescue Plan Fund Distributions to State and Local Governments?” Federal Reserve Bank of Cleveland, Cleveland Fed District Data Brief. https://doi.org/10.26509/frbc-ddb-20210930

This work by Federal Reserve Bank of Cleveland is licensed under Creative Commons Attribution-NonCommercial 4.0 International