- Share

The Unemployment Cost of COVID-19: How High and How Long?

We use flows into and out of unemployment to estimate the unemployment rate over the next year. This approach produces less stark projections for the unemployment rate over the course of the next year than some of the more alarming projections that have been reported. Using our approach and assuming that the severest social-distancing measures will be lifted in June, we estimate that the unemployment rate will peak in May at about 16 percent but gradually decline thereafter and end the year at 7.5 percent.

The views authors express in Economic Commentary are theirs and not necessarily those of the Federal Reserve Bank of Cleveland or the Board of Governors of the Federal Reserve System. The series editor is Tasia Hane. This paper and its data are subject to revision; please visit clevelandfed.org for updates.

After experiencing the longest expansion in history, the US labor market is now undergoing tremendous stress because of the COVID-19 outbreak and subsequent mitigation efforts. As a result of stay-at-home orders, nonessential business closures, health concerns, and reduced demand for products and services, many workers have stopped working.

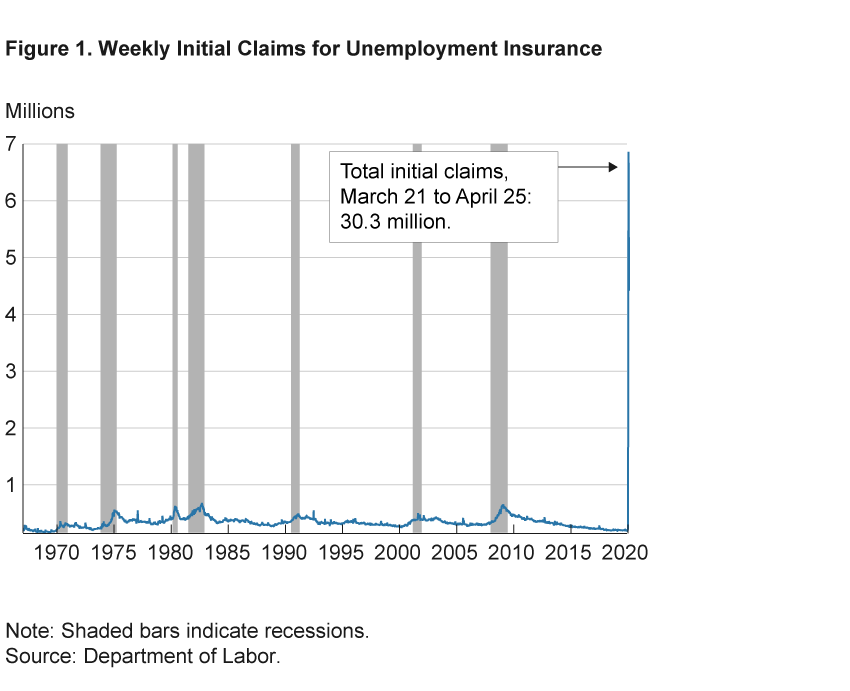

Among common labor market indicators, the first sign of massive job losses came with the initial unemployment insurance claims report for the week ending on March 21. More than 3.3 million workers filed for unemployment insurance that week, an unprecedented number even during deep recessions (figure 1). The surge in initial claims for unemployment insurance continued, and within five weeks, total initial claims had reached the 26 million mark. While a great deal of uncertainty surrounds how many of these workers will return to their previous jobs or which companies will still remain in business when social-distancing measures are eased, it is important to obtain our best estimates for how much the unemployment rate will increase and how persistent the increase will be.

In this Economic Commentary we analyze flows into and out of unemployment—utilizing what is commonly referred to as a flows-based approach—to provide tentative answers to these questions. This approach produces less stark projections for the unemployment rate over the course of the next year than some of the more alarming projections that have been reported. In preparing our projections, we make several assumptions about the nature of the economic shock we are undergoing and the prospects for the reversal of the mitigation policies currently in place. Most importantly, we think the shock is temporary. Unlike in past recessions, we know the underlying reason for the contraction in economic activity, and because the shutdowns are coordinated by federal and state governments, they could be reversed gradually once the public health emergency passes.

Using our approach and assuming that the severest social-distancing measures will be lifted in June,1 we estimate that the unemployment rate will jump from 4.4 percent in March to 12 percent in April with a further increase in May to about 16 percent. We expect that the unemployment rate then will start declining as the mitigation efforts begin to subside starting sometime in June. Our estimate for the unemployment rate at the end of the year is 7.5 percent.

Stocks versus Flows

The initial claims report, produced by the Bureau of Labor Statistics (BLS), is a count of the number of individuals who have lost their jobs and applied for unemployment benefits. It is tempting to interpret this number as a rise in the number of workers who are unemployed (the stock of unemployed) and use it to forecast the unemployment rate for the upcoming month. To do this calculation for April, we first take the initial claims for March and project initial claims for the four weeks spanning the April employment release. This yields an estimate of 22 million. We add this figure to the stock of unemployed in March (7 million), which suggests the stock of unemployed will rise to 29 million in April. To calculate the unemployment rate in April, we divide the stock of unemployed by the number of workers in the labor force (around 163 million, assuming it remains the same as in March), and arrive at an unemployment rate of 18 percent. If we also consider that not all unemployed workers qualify or file for unemployment insurance benefits, we may conclude that the April unemployment rate might be well above 20 percent, possibly around 35 percent.

However, one problem with this approach is that it views labor markets as static; it implicitly assumes that unemployed workers never leave unemployment. But labor markets are fluid. Workers are continuously flowing into the pool of the unemployed and out of it, and what matters for the unemployment rate is the net number of those unemployed, not the gross flows into unemployment alone. Another problem with the approach is that initial claims reflect only a subset of those who have lost jobs: A large number of workers might enter into unemployment without filing for unemployment benefits. To illustrate how inaccurate this approach can be, we do the above calculation for the Great Recession and the 1980–1982 recessions and find that it would have significantly overestimated the observed unemployment rate.

Though using changes in stocks to calculate the unemployment rate is common, we argue that focusing on the unemployment flow rates directly is preferable because it can provide a more transparent view of the evolution of unemployment. In addition, we argue that the relationship between initial claims and the inflow rates into unemployment is not as simple as the basic calculation above suggests. The fraction of eligible workers who actually apply for unemployment insurance (the take-up rate) rises substantially during recessions as more workers file for unemployment insurance amid deteriorating labor market conditions. The take-up rate is even more likely to increase now because unemployment insurance coverage has been expanded under the Coronavirus Aid, Relief, and Economic Security Act (CARES Act).

Unemployment Inflow and Outflow Rates

Our approach is based on the stock-flow dynamics of the unemployment rate. From this point of view, unemployment rises when more people become unemployed (that is, when inflows into unemployment increase) or when unemployed people remain unemployed longer than had previously been the case (that is, when outflows from unemployment—to employment or to labor-force exit—decrease). We refer to the unemployment inflow probability as S (think of job separation—job loss—or entry into unemployment from out of the labor force) and the unemployment outflow rate as F (think of job finding or leaving the labor force). Economic theory provides us with a simple equation that relates these underlying flow rates to the unemployment rate. Therefore, if we have reliable estimates of the underlying flow rates at a point in time, Ft and St, we can characterize the evolution of the unemployment rate accurately. The flow approach has been proven to improve forecast accuracy both in the very near term (Barnichon and Nekarda, 2012) and in the medium-to-long run (Tasci, 2012; Meyer and Tasci, 2015; Crump et al., 2019).

So the first step in using the flows-based approach to calculate the path of the unemployment rate is to produce reliable estimates of the underlying flow rates for the forecast period. We start that exercise by considering a historical perspective. We look at typical values of the underlying flow rates over time, their extreme values during past recessions, and the way these values have translated into the unemployment rate. This perspective will give us a sense of the reasonable range for the flow rates.

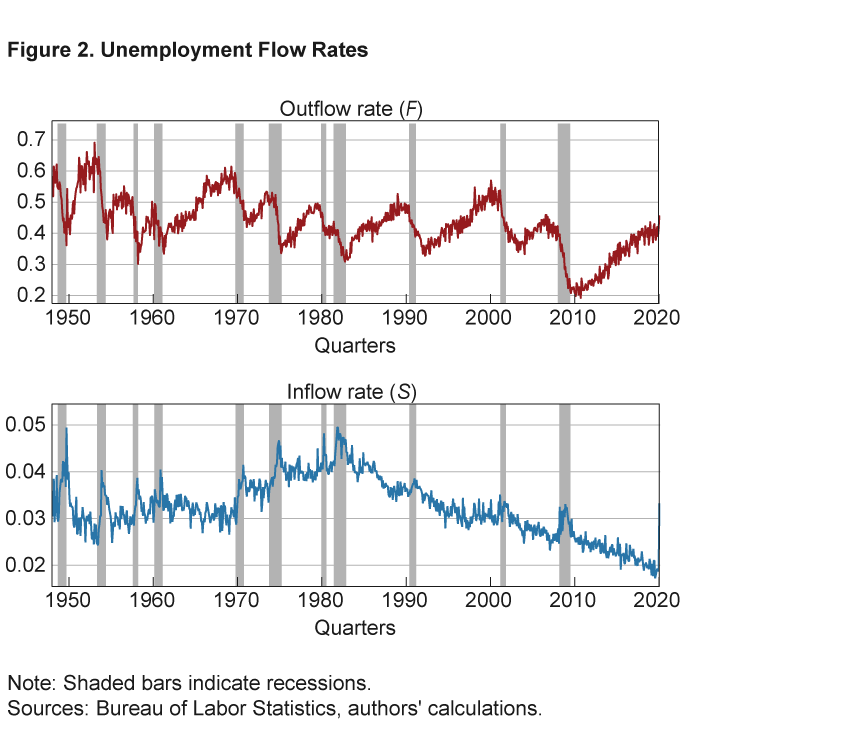

Figure 2 shows the unemployment outflow and inflow rates, F and S, from 1948 to 2019 as computed using the approach developed by Shimer (2012). Since flow rates are measured in continuous time, they refer to the flow of workers between two Current Population Survey (CPS) reports. As an example, we refer to the flow of workers from mid-March to mid-April as the flow rates for March. One can see from figure 2 that, over the course of a typical business cycle, the outflow rate, F, is procyclical—it rises during expansions and contracts as the economy experiences a downturn. It is important to note that big spikes in job destruction will change the outflow rate by making it harder for the unemployed to find jobs because of increased competition for jobs. Separations, or the inflow probability, S, move in the opposite direction, rising sharply at the onset of a recession and normalizing over the remainder of the cycle. For the period from 1948 through 2019, F seems to have fluctuated between 0.2 and 0.7, implying that, historically, between 20 percent and 70 percent of the unemployed left unemployment in a given month. S, on the other hand, moved in a narrow band between 0.02 and 0.05 over the whole period, implying that inflows into unemployment historically averaged between 2 percent and 5 percent of the labor force.

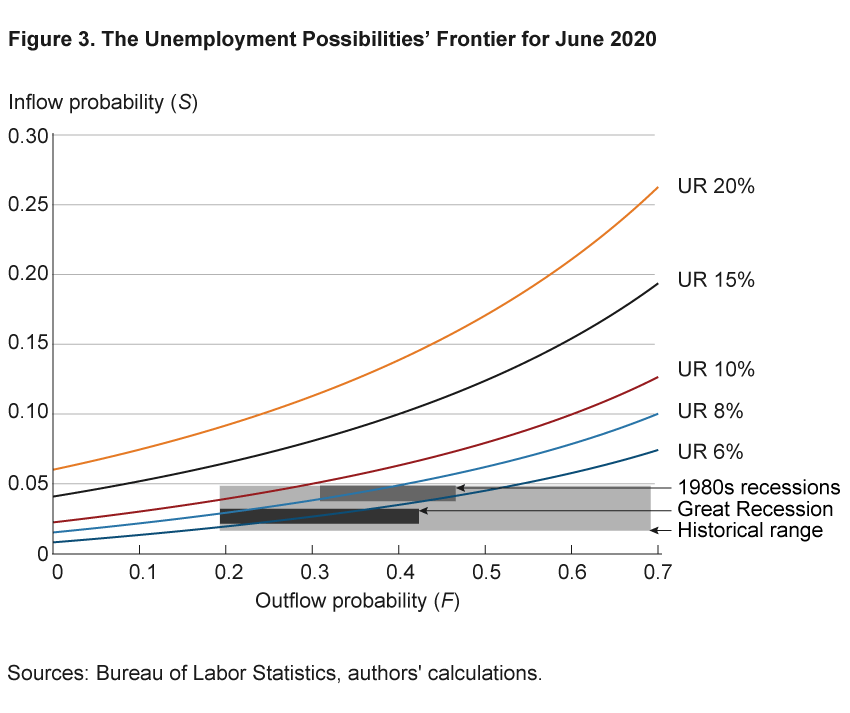

We can use these results to give a first approximation of the likely range of possible unemployment rate paths for the upcoming months. Let’s consider some of the available forecasts, which vary widely given the uniqueness of the current shock. We come at the question in a reverse fashion by asking what values of Ft and St would produce any of the unemployment rate forecasts and then comparing the resulting values with their historical ranges. We illustrate these calculations in a display we call an unemployment possibility frontier. Our unemployment possibility frontier shows all the possible combinations of Ft and St in a specified month that would result in a given unemployment rate over a set of upcoming months. We compute frontiers for April, May, and June, starting from the most recent reading of the unemployment rate, 4.4 percent in March.2

Figure 3 presents the results from this exercise for June. The combinations of Ft and St along each curve generate the level of the unemployment rate indicated by the respective curve. The picture implies, for instance, that if the economy sheds jobs at a 10 percent rate over the next three months—that is twice as high as the rate has ever been since 1948—and F stays in its historical range, the unemployment rate could reach 20 percent in June.

The shaded areas highlight how unprecedented the current situation might be. They show how far F and S values ranged during the extremes of the Great Recession and the 1980–1982 recessions as well as during the entire time for which we have data. Even during the Great Recession, the worst labor market downturn since 1948, F fluctuated between 0.2 and 0.42 and S moved between 0.023 and 0.033. If we replicated the worst possible combination of F and S in that episode (a high S of around 0.033 and a low F of around 0.2) for the next three months, the unemployment rate could go up to only about 8 percent. In fact, if we assume that we will get the worst possible realization of the flow rates ever seen—an F of 0.2 and an S of 0.05—the unemployment rate would go up only to 12 percent.

Using this historical perspective to narrow down the range of plausible values, we now turn to estimating the likely path of the inflow and outflow rates in the immediate future.

Unemployment Inflow Rate Projections

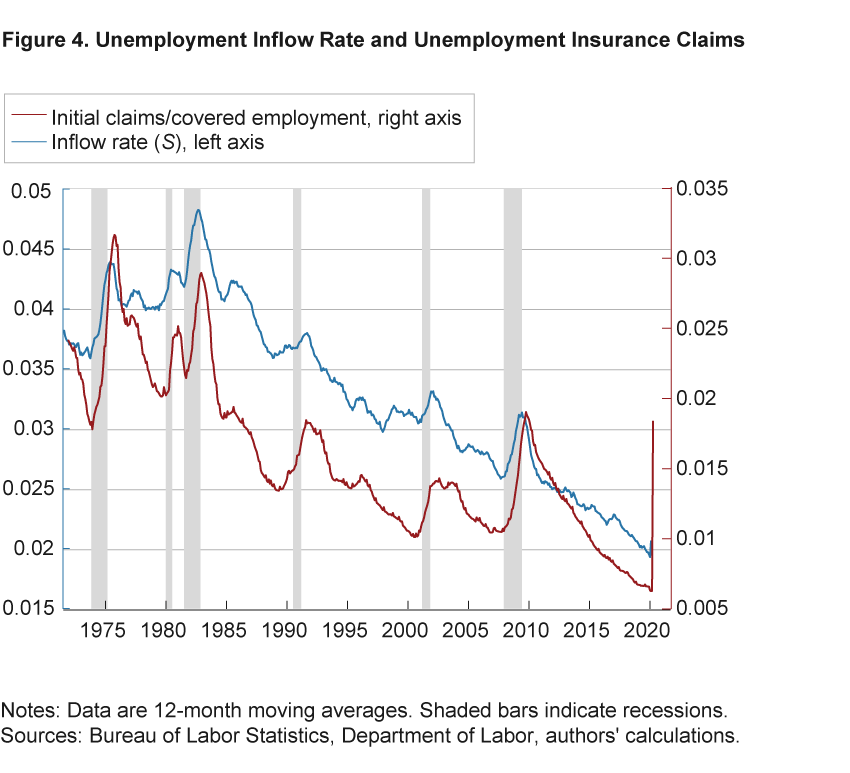

Our projections for the unemployment inflow rate make use of the relationship between initial claims and unemployment inflows. These two series are closely related since surges in job losses are typically accompanied by sharp rises in initial claims for unemployment insurance. Figure 4 shows the evolution of these two rates since 1970, with initial claims plotted as a fraction of the employment that is covered by the unemployment insurance system to translate claims into a rate similar to the unemployment inflow rate.

While there is a striking comovement between two series, they display differences in levels and cyclicality that arise from time variation in unemployment insurance eligibility, take-up rates, and movement into unemployment from out of the labor force. The time variation in these factors is captured by the inflow rate but not by initial claims as discussed in Hobijn and Şahin (2011). To estimate the relationship between the rates more accurately given these differences, we run a regression of the form:

log(st )= β0 + β1log(Initial Claimst / Covered Employmentt ) + εt .

This regression suggests that when the ratio of initial claims to covered employment rises by 1 percentage point, the inflow rate typically rises by 0.5 percentage points. We use these regression results to translate a path of initial claims into a path of the inflow rate, and from there use the inflow rate to calculate the unemployment rate. The path of initial claims must also be estimated, and we do this through mid-June by taking the initial claims data from the week ending March 21 to the week ending April 25 and projecting the path forward based on the following two assumptions. First, we assume that all the workers identified by Leibovici, Santacreu, and Famiglietti (2020) as having the highest risk of layoff or unemployment will have filed for unemployment insurance by mid-May. Second, we assume that thereafter the path of initial claims will follow the path of sharp declines observed during the Great Recession, averaging around 600,000 and declining gradually to February levels by the end of the year (see table 1).

| Reporting date | Number of workers |

|---|---|

| April 25 | 3,840,000 |

| May 1 | 2,610,000 |

| May 8 | 2,610,000 |

| May 15 | 600,000 |

| May 22 | 600,000 |

| May 29 | 600,000 |

| June 5 | 600,000 |

Note: This table does not reflect the initial claims report released on May 7, 2020.

Sources: Department of Labor, authors’ calculations.

With this path, our projected inflow rate jumps to 10.3 percent, twice the highest rate the US economy has ever experienced since 1948. The rate declines to 8.1 percent in May and then 3.4 percent in June.

Unemployment Outflow Rate Possibilities

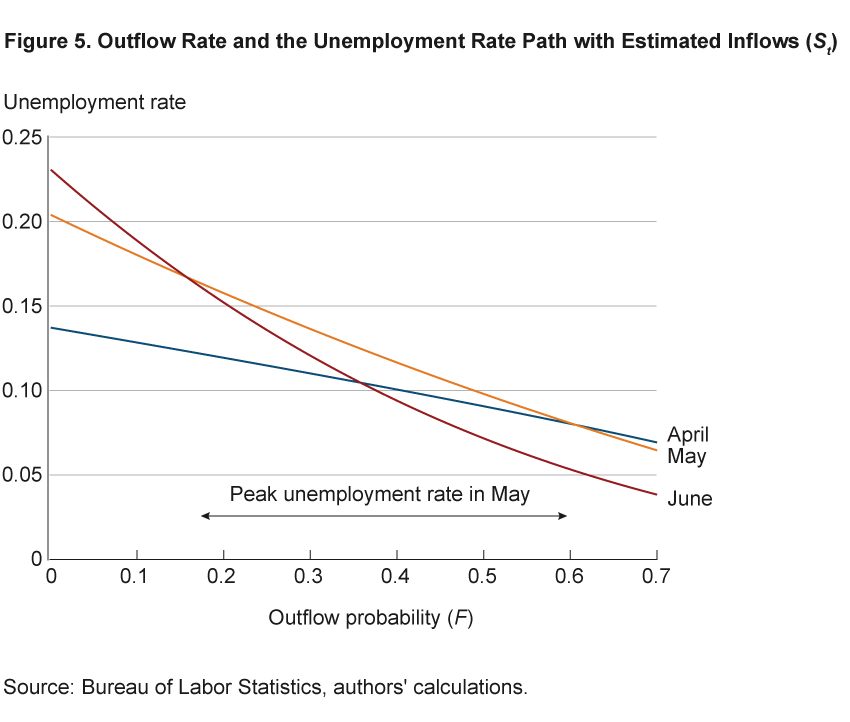

Once we have a forecast for the inflow rates through May, we can narrow down the possible path for the unemployment rate in the next three months. Figure 5 replicates the exercise shown in figure 3 but this time holding the inflow rates at the levels we forecasted using the initial claims data. We see more clarity with this picture in terms of a possible path for the unemployment rate. What stands out is that for a broad range of possible outflow rates over the three-month horizon, the unemployment rate will likely peak in May. Compared to the last actual data point in February (0.45 or 45 percent), any drop in this outflow rate will immediately put us above 10 percent unemployment starting in April.

If we assume that the available data on initial claims allow us to reasonably gauge the path of the unemployment inflow rate, the question becomes how low can the outflow rate go in this episode? Given the unprecedented nature of the labor market stress we are experiencing, we think the trough of the outflow rate will likely be around the low end of the historical range, which is 20 percent. We believe that the lowest it could go is 10 percent. That is because unemployment outflows include not only workers who get jobs but also those who leave the labor force, and typically around 40 percent to 50 percent of unemployed workers leave unemployment in a given month for this reason. So even if no worker manages to find a job, there will still be workers leaving the labor force, presumably at a higher rate during the COVID-19 pandemic due to health concerns, the closure of K-12 schools affecting workers’ availability, and discouragement about job prospects as documented by Coibion, Gorodnichenko, and Weber (2020). Moreover, it is possible that unemployed workers will be able to find jobs. Survey evidence and public announcements about hiring plans of businesses point to strong demand for some services such as logistics, delivery, and specific retail.3

Therefore, we consider two possible projections for the outflow rate. In the baseline projection, we set the outflow rate for the next three months to its historical minimum value of 20 percent. In projecting the unemployment rate over a longer period, we assume that the weakness in the outflow rate will persist beyond 2020 even if job destruction subsides—consistent with the rate’s behavior in post-1990 US recessions. In the more pessimistic projection, we set the outflow rate to 10 percent.

Unemployment Rate Projections

Now that we have projections for the inflow and outflow rates through May, we turn to estimating the unemployment rate going forward. Given these rates, we can forecast the unemployment rate from April to June.

In our baseline forecast with an outflow rate of 0.2, we expect the unemployment rate will reach 12 percent in April and peak at 15.8 percent in May, followed by a small decline in June. Our pessimistic scenario with an outflow rate of 0.10 would instead bring the unemployment rate to 18 percent in May.

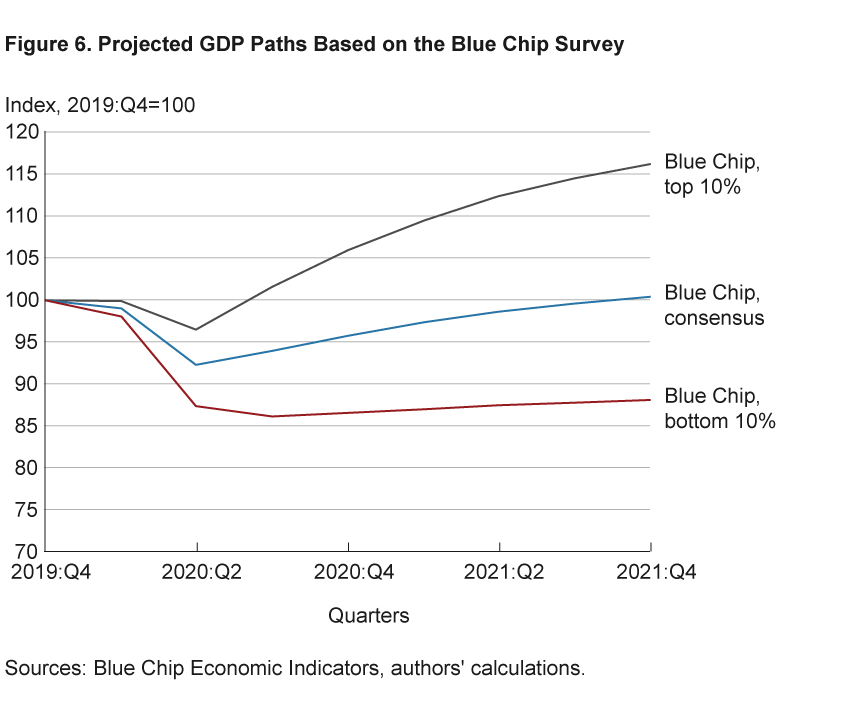

Our projections for the flow rates through June determine the magnitude of the jump in the unemployment rate. However, what happens to the unemployment rate thereafter will depend on the behavior of flow rates after June. We use a statistical model to generate forecasts for the unemployment inflow and outflow rates from 2020:Q3 through 2021:Q4. In particular, we use the model in Tasci (2012), which links flow rates to the state of the economy as captured by GDP. In our implementation, we condition our GDP forecast to follow the path given by the Blue Chip consensus forecast, a resource of Wolters Kluwer Legal and Regulatory Solutions US.

The consensus forecast from the Blue Chip survey sees a sharp contraction in 2020:Q2 followed by a gradual recovery over the course of the next six quarters back to prerecession levels. Obviously, there is a lot of uncertainty around the recovery path of GDP, particularly with the uncertainty concerning the course of the pandemic. So in addition to the GDP path based on the Blue Chip consensus, we also consider more pessimistic and more optimistic paths for GDP. In particular, we also consider the top 10 percent and bottom 10 percent average projections of the Blue Chip panelists.4 Figure 6 shows that the pessimistic case (bottom 10 percent) predicts a persistently depressed economy even by the end of 2021.

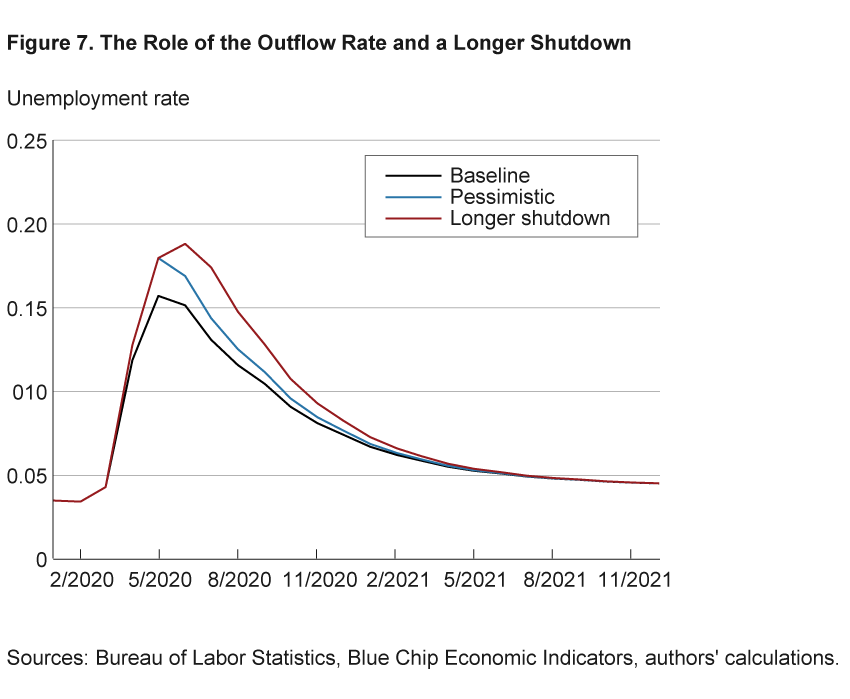

In our baseline forecast, the unemployment rate ends the year at 7.5 percent. In 2021, with a continued recovery of the economy, it reaches 5 percent in July. In our more pessimistic scenario and again assuming continued recovery of GDP, the unemployment rate peaks at 18 percent in May and ends the year at 7.8 percent and reaches 5 percent in July 2021 (see figure 7).

We also calculate a longer shutdown scenario, which assumes one more month of the pessimistic outflow rate scenario. The timing of the peak is moved to June (rather than May), and the peak unemployment rate moves up from 18 to 18.9 percent. This exercise suggests that an additional month of keeping the economy-wide restrictions in place would bump the peak unemployment rate up less than 1 percent and would not affect the unemployment rate at the end of 2020 provided the economy starts growing and the labor market starts functioning. Of course, this does not mean that an additional month of restrictions in the interest of public health would be without economic cost in the short run (e.g., additional income would be lost).

Together these three scenarios, our baseline forecast, pessimistic forecast, and longer shutdown forecast, highlight the role the outflow rate plays in determining unemployment dynamics in the near future. Figure 7 depicts these scenarios, which converge before the end of the year. Note that this convergence could be realized even if no one who is unemployed manages to find a job but the unemployed leave the labor force at a rate that is not that high compared to earlier recessions. This outcome would of course lower the labor force participation rate substantially.

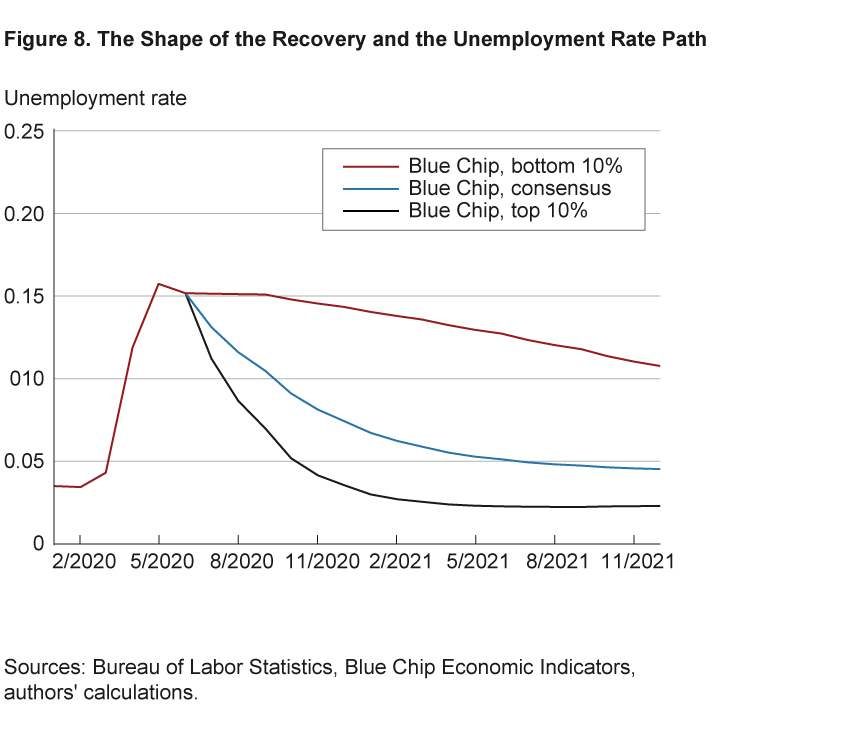

Finally, we quantify the effects of a stronger or weaker recovery on our unemployment rate projections. As noted above, in our baseline scenario, the recovery of economic activity in the second half of the year leads to a significant improvement in unemployment, with half of the overall jump in the unemployment rate (6 percentage points) unwinding by October. Obviously, if the economic recovery is more robust (as in the top 10 percent projection of GDP forecasts in the Blue Chip survey) unemployment will normalize much more quickly.5 Conversely, if the recovery is very shallow (as in the bottom 10 percent case), unemployment could stay stubbornly above 10 percent throughout the forecast horizon. Figure 8 highlights the differences in the unemployment path under these different GDP forecast scenarios.

Conclusion

Our analysis of historical flow rates in and out of unemployment implies that the unemployment rate will likely peak below 20 percent and will come down rather swiftly over the last two quarters of this year provided that the labor market is at least partially functional. We find that an additional month of drastic mitigation efforts could add another 1 percentage point to the peak unemployment rate and push it to June. However, while our estimate is the one we judge to be most likely, there is considerable uncertainty around it, particularly given the uncertainty surrounding the course of the pandemic. It is important to remember that our estimate depends on our assumptions that the shock to GDP growth is temporary and that job destruction and job creation will normalize slowly, consistent with typical recessions. If, however, we start seeing business bankruptcies and other permanent dislocations, or if the public health emergency does not pass soon, the effects on the labor market might be notably different from what we find here.

Footnotes

- The University of Washington’s Institute for Health Metrics and Evaluation provides model-based evaluations for each state over the course of the pandemic and now predicts that for a majority of the states, relaxing social distancing could be possible by sometime in June with some additional containment strategies such as testing, contact tracing, limiting of gathering size, and isolation. See https://covid19.healthdata.org/united-states-of-america (Accessed on April 28, 2020). Return

- To simplify the exposition, we assume one value for F or S for this forecast duration. Since the March employment report provided us with the flow rates for February, this means that assuming a hypothetical path for them for March, April, and May would be sufficient to pin down an unemployment rate for June. Return

- A Challenger, Gray & Christmas, Inc., report in March highlights hiring announcements amounting to about 800,000 employees. See www.challengergray.com/press/press-releases/2020-march-job-cut-report-222288-cuts-announced-march-most-jan-2009-covid (accessed on April 21, 2020). Return

- These forecasts are computed as the averages of the top 10 percent and bottom 10 percent from the range of individual Blue Chip projections for GDP growth. Return

- Note that the unemployment rate projections in figure 8 are not the unemployment rate projections from the Blue Chip survey itself. We use the corresponding GDP path from the survey to generate our own forecast from the flow model of Tasci (2012). Return

References

- Barnichon, Regis, and Christopher J. Nekarda. 2012. “The Ins and Outs of Forecasting Unemployment: Using Labor Force Flows to Predict the Labor Market.” Brookings Papers on Economic Activity, 43: 83-131. https://doi.org/10.1353/eca.2012.0018.

- Challenger, Gray & Christmas, Inc. 2020. “2020 March Job Cut Report: 222,288 Cuts Announced in March, Most Since Jan 2009; COVID Claims 141,844.” www.challengergray.com/press/press-releases/2020-march-job-cut-report-222288-cuts-announced-march-most-jan-2009-covid (accessed on April 21, 2020.)

- Coibion, Oliver, Yuriy Gorodnichenko, and Michael Weber. 2020. “Labor Markets During the COVID-19 Crisis: A Preliminary View.” Unpublished manuscript. https://eml.berkeley.edu/~ygorodni/CGW_covid19.pdf.

- Crump, Richard K., Marc Giannoni, Stefano Eusepi, and Ayşegül Şahin. 2019. “A Unified Approach to Measuring u*.” Brookings Papers on Economic Activity, 219(1): 143–238. https://doi.org/10.1353/eca.2019.0002.

Hobijn Bart, and Ayşegül Şahin. “Do Initial Claims Overstate Layoffs?” 2011. Federal Reserve Bank of San Francisco, Economic Letter, 2011-04. https://www.frbsf.org/economic-research/publications/economic-letter/2011/february/claims-layoffs-overstated/. - Meyer, Brent, and Murat Tasci. 2015. “Lessons for Forecasting Unemployment in the U.S.: Use Flow Rates, Mind the Trend.” Federal Reserve Bank of Cleveland, Working Paper No. 15-02. https://doi.org/10.26509/frbc-wp-201502.

- Leibovici, Fernando, Ana Maria Santacreu, and Matthew Famiglietti. 2020. “Social Distancing and Contact-Intensive Occupations.” Federal Reserve Bank of St. Louis, On the Economy Blog (March 24). https://www.stlouisfed.org/on-the-economy/2020/march/social-distancing-contact-intensive-occupations.

- Shimer, Robert. 2012. “Reassessing the Ins and Outs of Unemployment.” Review of Economic Dynamics, 15(2): 127–148. https://doi.org/10.1016/j.red.2012.02.001.

- Tasci, Murat. 2012. “The Ins and Outs of Unemployment in the Long Run: Unemployment Flows and the Natural Rate.” Federal Reserve Bank of Cleveland, Working Paper No. 12-24. https://doi.org/10.26509/frbc-wp-201224.

Suggested Citation

Şahin, Ayşegül, Murat Tasci, and Jin Yan. 2020. “The Unemployment Cost of COVID-19: How High and How Long?” Federal Reserve Bank of Cleveland, Economic Commentary 2020-09. https://doi.org/10.26509/frbc-ec-202009

This work by Federal Reserve Bank of Cleveland is licensed under Creative Commons Attribution-NonCommercial 4.0 International