- Share

Merger Control in the Banking Sector

This Commentary discusses the implications of merger control policy on merger activity in the banking sector, drawing on an analysis of the European banking sector during a period in which stricter merger policies were being introduced. It identifies several changes to the bank mergers taking place after the introduction of the stricter policies that are consistent with higher expected returns for shareholders and more procompetitive transactions. The evidence suggests that the new merger policy was successful in preventing mergers that are excessively anticompetitive, while it also led to banks’ finding mergers that are expected to deliver greater efficiency.

The views authors express in Economic Commentary are theirs and not necessarily those of the Federal Reserve Bank of Cleveland or the Board of Governors of the Federal Reserve System. The series editor is Tasia Hane. This paper and its data are subject to revision; please visit clevelandfed.org for updates.

Advanced economies typically adopt antitrust policies to promote competition and prevent monopolies from forming. Merger control, which sets rules under which mergers can be blocked as anticompetitive, is a key element of such policies. For example, in most settings, a merger creating a monopoly would be considered harmful to competition and prohibited. But banks, which provide essential financial intermediation services and are critical to a functioning advanced economy, have historically been allowed more latitude. More recently, lawmakers have begun to ask whether banks should be subject to the same rules as other types of businesses.

This Commentary discusses the implications of merger control policy for the banking industry, drawing on an analysis of the European banking sector during a period in which stricter merger policies were being introduced. It argues that new merger control legislation has led to bank mergers with larger announcement premiums, that is, increases in stock prices after a merger is announced, which is a proxy for market participants’ perception of the value created. This stock price response is associated with a reduction in the size of the acquiring company and a decrease in the industry overlap of the merging parties, while other important aspects of the mergers remain unchanged. This evidence suggests that firms adjust to the new regulatory environment by focusing on increasing efficiencies rather than exploiting market power, which is consistent with the objective of promoting competitive markets.

Merger Control in the Banking Sector

An efficient and competitive banking sector forms an integral part of a healthy economy. Banks support the real economy by providing functions such as credit intermediation, liquidity provision, monitoring of borrowers, and others. If the banking sector does not perform its functions well, the real economy suffers, as seen in the Great Recession following the global financial crisis of 2008.

Partly because of their central role in the economy and the risk of spillovers from bank failures, the banking industry has not only been heavily regulated but, in many countries outside the United States, has also long been exempted from rigorous enforcement of antitrust policy. The argument for this position has been that vigorous competition could be detrimental to financial stability. More recently, alongside wider banking liberalization in the 1970s and 1980s and newer research showing a positive link between competition and stability, greater attention has been paid to the enforcement of antitrust and competition rules in the banking sector. However, it remains the case that special provisions for banking often limit the extent of these efforts.1

This Commentary describes the results of a recent analysis exploring the effects of merger control policy, one key aspect of antitrust policy, on merger activity in the banking sector (Carletti et al., 2017). The analysis takes advantage of a wave of new merger control legislation in European countries in the 1990s and early 2000s. During that time, there were a total of 18 major new merger control laws introduced in 15 different countries, the effect of which was to strengthen merger control law and its enforcement.2 These changes represent a “shock” to the regulatory environment, similar to a natural experiment, which provide researchers with an opportunity to study the implications of the changes on mergers in the banking sector.

The dataset used in the analysis is taken from the SDC Mergers and Acquisitions database. It includes mergers that occurred between 1986 and 2007, had a minimum purchase value of $5 million (US dollars), and involved an acquired bank (“target”) in one of the European countries with changes in merger-control legislation. For each merger, SDC reports the identity of the parties involved, as well as characteristics of the transaction, including, for example, the dollar size of the deal and whether it was a hostile acquisition. These data are supplemented by stock market and financial data from Datastream, matched with the firms involved in the transactions. Overall, there are 380 transactions in the sample.

Measuring the Impact of New Legislation

To measure the impact of changes in merger-control legislation on merger activity, we would ideally compare the characteristics of mergers that happened after the legislative changes with those that would have happened without these changes. However, this approach faces a key difficulty in that we can never observe the relevant counterfactual, that is, mergers that would have taken place had the legislation changes never been enacted. Mergers are known to vary in frequency and features across different periods (for example, during so-called “merger waves”) as well as in response to differences in national regulations. As a consequence, mergers before the law may be different from mergers after the law simply because of a common time trend or because they take place in different countries, and not because of the effect of the policy concerned. Thus, estimating the effect of the legislation requires a statistical tool designed to address these concerns.

The analysis of the European bank merger data follows a “differences-in-differences” strategy that exploits the staggered timing of the new legislation across the different countries.3 In this approach, an estimate of the effect of the law is provided by measuring the change in an outcome variable before and after the legislation in a country that changed the law and then comparing that change to the change in the same outcome variable in a country that did not. That way, researchers control for both differences between countries and common time trends. Under the assumption that both countries would have moved in parallel but for the change in the law, any remaining deviations identify the effect of the new law.

Higher Announcement Premiums for Targets

Applying this approach to the European bank merger data uncovers several changes in the characteristics of bank mergers following the introduction of the new merger legislation. Notably, this includes an increase of around7 percentage points on average in the announcement premium for those banks that are acquired (table 1). The announcement premium reflects the stock market response to the news of the merger and provides a proxy for the financial market’s expectation of the effect of the transaction on the valuation of the firms involved. As a rule, announcement premiums have been positive on average for targets and zero for the acquirers across many industries, including banking.4 This pattern holds true in the sample of European bank mergers, with an average announcement effect of around 11 percent for targets and around zero for acquirers. Against this background, the observed increase of7 percentage points on average in the announcement effect is significant.

Table 1. Effect of Change in Legislation on Target Announcement Premiums

| Effect of change in legislation (percent) | ||||

|---|---|---|---|---|

| Variable | No controls | With controls | ||

| All mergers | Average effect | +6.5** | +7.4** | |

| Interaction effects | ||||

| Without change in control | −0.1 | +1.2 | ||

| With change in control | +10.4** | +11.1** | ||

| Mergers with change in control | Average effect | +14.4*** | +15.1** | |

| Timing of effect (year) | ||||

| [−3, −2] | −4.2 | −3.7 | ||

| [−1, 0] | −3.4 | −6.3 | ||

| [1, 2] | +24.5** | +23.9** | ||

| [3, 4] | +9.6* | +11.9* | ||

| >4 | +5.7 | +4.6 | ||

Notes: Announcement premiums are measured from 30 days before the merger announcement to 5 days after the announcement. * indicates significance at the 10 percent level, ** indicates significance at the 5 percent level, and *** indicates significance at the 1 percent level.

Source: Analysis based on Carletti et al. (2017).

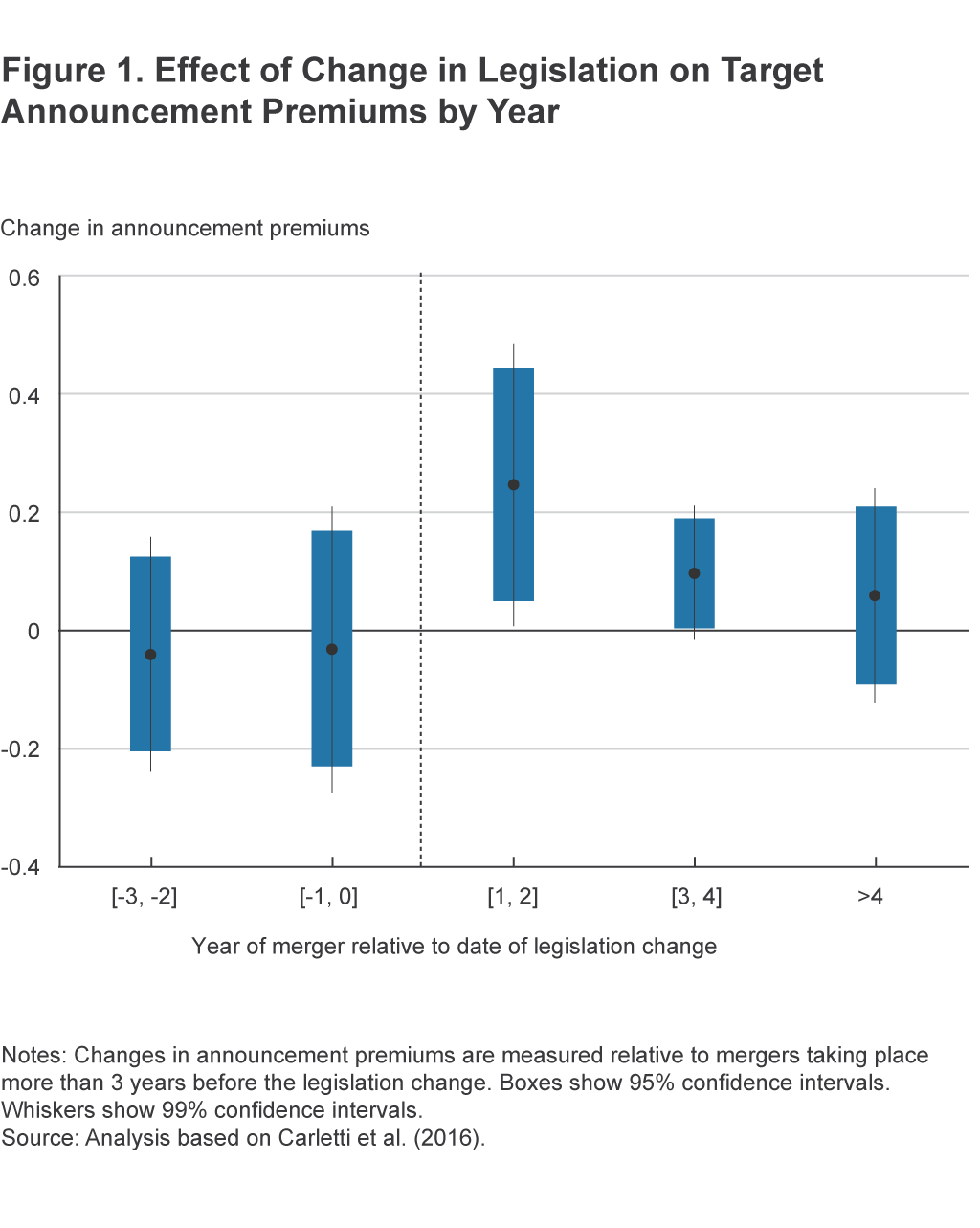

A more granular analysis shows that the effect is concentrated in transactions that involve an explicit change of control, here defined as a transaction that involves an increase of a stake in the target from less than 50 percent to more than50 percent. The data show an effect of close to zero for transactions that do not involve a control change and a statistically significant increase of around 10 percentage points for those that do. In the subsample of mergers with a change of control, the positive effect increases to 14 percentage points. The effect of the merger legislation furthermore appears to be concentrated in the first few years following the introduction of the legislation. An analysis of the control change subsample breaking out the effect by time period suggests that the period with a statistically significant effect covers only the first four years. The estimates for these year bands are large but imprecisely estimated, with relatively large standard errors, as illustrated in figure 1.

Interpretation

What can explain the positive effect of the legislative changes on the stock market’s valuation of a banking firm acquired in a merger? Two general explanations can be put forward. First, it could be that banking mergers after the legislative changes are more valuable and generate higher returns for shareholders. This higher overall value would translate into greater returns for a target’s shareholders. Alternatively, the increase in returns could reflect a transfer of returns from the acquiring firms to the targets. That is, higher returns for a target’s shareholders would come at the expense of the returns of the acquiring firm’s shareholders. However, the data in the merger sample do not show a decline in returns for the shareholders of the acquiring firm as would be expected with such a transfer. The increased merger premium thus appears to be consistent with the explanation that the stock market expects higher profitability of the merging firms in the sample.

There are several plausible sources of the expected increase in profitability, summarized in table 2. First, the higher profitability could simply be due to a greater probability of an announced merger taking place. Stricter merger review processes and the costs involved may force merging parties to put forward only those transactions they reasonably expect to succeed. Under this argument we would expect to see an increase in the share of transactions that are completed after the announcement (“completion rate”). Statistical tests do not find a significant difference, and thus the European merger data do not support this explanation.

Table 2. Summary of Effects of Change in Legislation on Merger Characteristics

| Variable | Effect of change in legislation |

|---|---|

| Main effect: Announcement premium | Increase |

| Possible explanations | |

| Completion rate | None |

| Leverage (pre-merger) | |

| Acquirer | None |

| Target | None |

| Profitability (pre-merger) | |

| Acquirer | None |

| Target | None |

| Market capitalization | |

| Acquirer | Decrease |

| Target | None |

| Ratio of acquirer over target | Decrease |

| Market overlap | |

| By geography | None |

| By industry | Decrease |

Notes: “Completion rate” measures the share of announced mergers that are consummated. “Leverage (pre-merger)” is a summary of results on four different measures of leverage in the year before the announcement of the merger. “Profitability (pre-merger)” represents a summary of results on two profitability measures in the year prior to the merger announcement.

Source: Carletti et al. (2017).

A second potential source of higher announcement premiums could be that the new legislation alters the type of banks that are selected as targets. If the target banks selected after the legislation have greater leverage and pre-merger profits, this difference may explain the observed change in the announcement premium. However, as before, there is no statistical evidence for a change in the pre-merger leverage and profitability of the merging parties in the European bank mergers.

Having rejected explanations based on completion rates and target selection, we conclude the observed higher announcement premiums may simply reflect the expectation that the combined firm will be able to generate higher profits after the merger. Such increased profitability after a merger would be the result of an increase in the combined firm’s market power or its efficiency or both. While the first is seen as anticompetitive, and merger legislation seeks to block transactions creating excessive market power, the second is seen as procompetitive and beneficial to consumers.

Market power in mergers typically derives from the size or overlap of the merging parties. Mergers between larger firms tend to involve larger market shares and thus are more likely to be anticompetitive. In addition to size, antitrust regulators consider mergers between banks with a greater degree of geographic or product overlap more likely to be anticompetitive. No evidence for either mechanism is revealed in this sample of European bank mergers.

The new legislation reduces the size of acquirers in terms of market capitalization, both when measured directly and as a ratio relative to targets’ market capitalization. As regards overlap, the analysis shows that while there is no change in the degree to which mergers involve banks from the same countries and thus no increase in geographic overlap, there has been a decrease in the share of mergers that involve firms sharing an industry code. Thus, after the legislation’s introduction, merged banks exhibit less overlap in the product space than before the legislation.

Overall, the data are inconsistent with mergers after the legislation generating greater market power. Indeed, the results suggest that the transactions involve less market power than before. Greater announcement premiums are thus likely to derive from gains in efficiency in the mergers involved, although the data do not provide sufficient detail for a direct test of this hypothesis.

Taken together, the evidence on European bank mergers is consistent with transactions’ being less anticompetitive after the introduction of merger control legislation, in line with the stated objective of such legislation. This change accompanies an increase in announcement premiums, suggesting that the stricter legislation has led to banks’ finding mergers that are expected to deliver greater efficiency.

Conclusion

This Commentary has explored the effect of merger control policy on merger activity in the banking sector, building on an empirical analysis of a wave of new merger legislation introduced in Europe in the 1990s and 2000s and its implications for bank mergers in the countries affected. It identified several changes to the bank mergers taking place that are consistent with higher expected returns for shareholders and more procompetitive transactions.

These findings highlight two interesting aspects of merger control policy design. First, merger control legislation has an impact on mergers beyond simply preventing the most anticompetitive transactions. While the objective of merger policy is to prevent certain mergers that are excessively anticompetitive, it also changes the characteristics of the mergers that do occur. An assessment of the effects of a policy would do well to take this change into account. Second, merger control policy can affect merger activity even in heavily regulated sectors such as the banking sector. Future research might want to explore further the interactions between merger control and sector-specific regulations. In addition, while this Commentary highlights the effect of such legislation on shareholders, a policymaker will be interested in the effect on customers and other stakeholders, as well.

Footnotes

- For further background on competition policy and the banking sector, see Carletti (2008) and Carletti and Vives (2009). Return to 1

- See Carletti et al. (2015) for a detailed description of these changes. Return to 2

- Specifically, it follows the framework in Bertrand and Mullainathan (2003) for multiple legislation changes. Return to 3

- See Jensen and Ruback (1983) and Becher (2000). Return to 4

References

- Becher, David A., 2000. “The Valuation Effects of Bank Mergers,” Journal of Corporate Finance, 6(2), 189–214.

- Bertrand, Marianne, and Sendhil Mullainathan, 2003. “Enjoying the Quiet Life? Corporate Governance and Managerial Preferences,” Journal of Political Economy, 111(5), 1043–1075.

- Carletti, Elena, 2008. “Competition and Regulation in Banking.” In Handbook of Financial Intermediation and Banking, pp. 449–482. Elsevier.

- Carletti, Elena, and Xavier Vives, 2009. “Regulation and Competition Policy in the Banking Sector.” In Xavier Vives (Ed.), Competition Policy in Europe, Fifty Years of the Treaty of Rome, pp. 260–283. Oxford University Press.

- Carletti, Elena, Philipp Hartmann, and Steven Ongena, 2015. “The Economic Impact of Merger Control Legislation,” International Review of Law and Economics, 42, 88–104.

- Carletti, Elena, Steven Ongena, Jan-Peter Siedlarek, and Giancarlo Spagnolo, 2017. “The Impact of Merger Legislation on Bank Mergers,” Federal Reserve Bank of Cleveland Working Paper No. 16-14R (first version July 2016).

- Council Regulation (EC) No 139/2004 of 20 January 2004 on the control of concentrations between undertakings (the EC Merger Regulation), Official Journal L 24, 29.01.2004, pp. 1–22.

- Jensen, Michael C., and Richard S. Ruback, 1983. “The Market for Corporate Control: The Scientific Evidence,” Journal of Financial Economics, 11(1), 5–50.

Suggested Citation

Siedlarek, Jan-Peter. 2017. “Merger Control in the Banking Sector.” Federal Reserve Bank of Cleveland, Economic Commentary 2017-10. https://doi.org/10.26509/frbc-ec-201710

This work by Federal Reserve Bank of Cleveland is licensed under Creative Commons Attribution-NonCommercial 4.0 International