- Share

Recessions and the Trend in the US Unemployment Rate

The unemployment rate in the United States falls slowly in expansions, and it may not reach its previous low point before the next recession begins. Based on this feature, I document that the frequent recessions prior to 1983 are associated with an upward trend in the unemployment rate. In contrast, the long expansions beginning in 1983 are associated with a downward trend. I then estimate a two-variable vector autoregression (VAR) that includes the unemployment rate and a recession indicator. Long-horizon forecasts from this VAR conditioned on no future recessions project that the unemployment rate will go to 3.6 percent after a long period with no recessions.

The views authors express in Economic Commentary are theirs and not necessarily those of the Federal Reserve Bank of Cleveland or the Board of Governors of the Federal Reserve System. The series editor is Tasia Hane. This paper and its data are subject to revision; please visit clevelandfed.org for updates.

When it comes to analyzing economic indicators to predict where the US economy is headed, the unemployment rate is arguably the variable familiar to most people. It receives attention from academics, policymakers, business economists, and politicians, but also the public at large. An appealing feature of the unemployment rate is its perceived ease of interpretation. A high or rising unemployment rate is a signal of macroeconomic slack or contraction, and a low or falling unemployment rate is a signal of macroeconomic health or expansion.

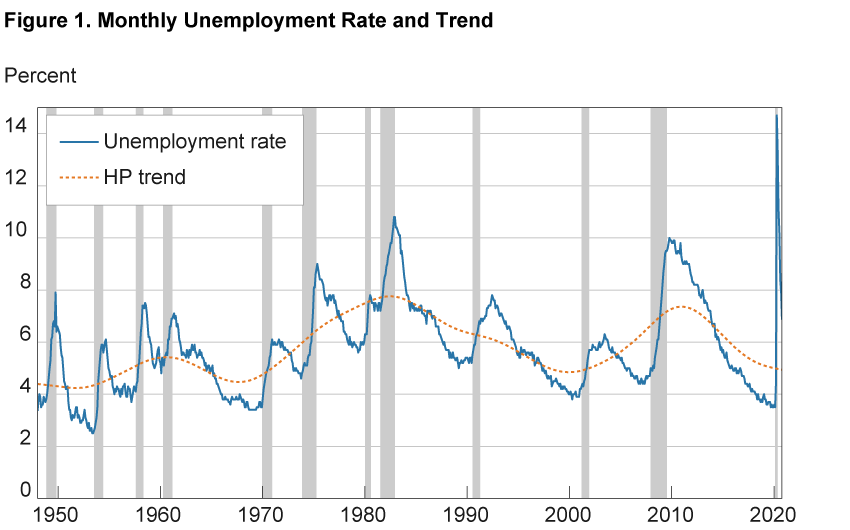

One issue that can confound this simple interpretation is that the unemployment rate may have a slow-moving trend that changes over time. If the trend is not static, then it is hard to know how far the current or forecasted unemployment rates are from the underlying trend. Figure 1 highlights this issue. It shows the monthly unemployment rate from January 1948 to October 2020 along with a line intended to estimate the unemployment rate trend. I compute this line with the statistical technique in Hodrick and Prescott (1997) (HP).1 The trend line shows substantial variation, falling below 5 percent in the 1960s and 1990s and rising above 7 percent in the 1980s and 2010s. Because of this changing trend, an unemployment rate of 6 percent may be viewed as indicating macroeconomic slack in some periods but macroeconomic health in other periods, making it difficult for economists, policymakers, and the public at large to know where the economy stands.2

Notes: Trend computed using a Hodrick and Prescott (1997) filter. Gray bars indicate recession periods.

Sources: US Bureau of Labor Statistics, Unemployment Rate [UNRATE], retrieved from FRED, Federal Reserve Bank of St. Louis (https://fred.stlouisfed.org/series/UNRATE), and author’s calculations.

Researchers and policymakers often acknowledge the trend in the unemployment rate. Researchers typically remove a time-varying trend from the unemployment rate before studying its business cycle properties.3 Policymakers on the Federal Reserve’s Federal Open Market Committee (FOMC) note in their Statement on Longer-Run Goals and Monetary Policy Strategy that the maximum level of employment “changes over time.”4 In fact, the longer-run projections of the unemployment rate in the FOMC’s Summary of Economic Projections have drifted down since 2012.5

Research has attributed much of the trend in the unemployment rate to demographic changes.6 In this Commentary, I suggest an additional, previously unrecognized source of the trend: the frequency of recessions. Because the unemployment rate rises quickly in recessions but falls slowly in expansions, it may not fall to its previous low point if a recession cuts an expansion short.7 Hence, frequent recessions can cause the unemployment rate to trend up over time. Figure 1 shows that this happened in the 1950s and the 1970s. Since 1983, recessions have been less frequent and expansions have been longer, causing the unemployment rate to regularly fall below its previous low point and generating a downward trend in the unemployment rate.8 In February 2020, the unemployment rate fell to 3.5 percent, its lowest level since 1969.

I also estimate the relationship between recessions and the unemployment rate with a statistical model called a vector autoregression (VAR). I use the VAR to make forecasts of the unemployment rate under the hypothetical scenario that there will be no recessions in the future. I intend for this hypothetical scenario to match the spirit of the FOMC’s longer-run projections of the unemployment rate, which are made “in the absence of further shocks to the economy.”9 My forecasts project that the unemployment rate will go to 3.6 percent after a long period with no recessions.

Recessions and Unemployment Rate Trends

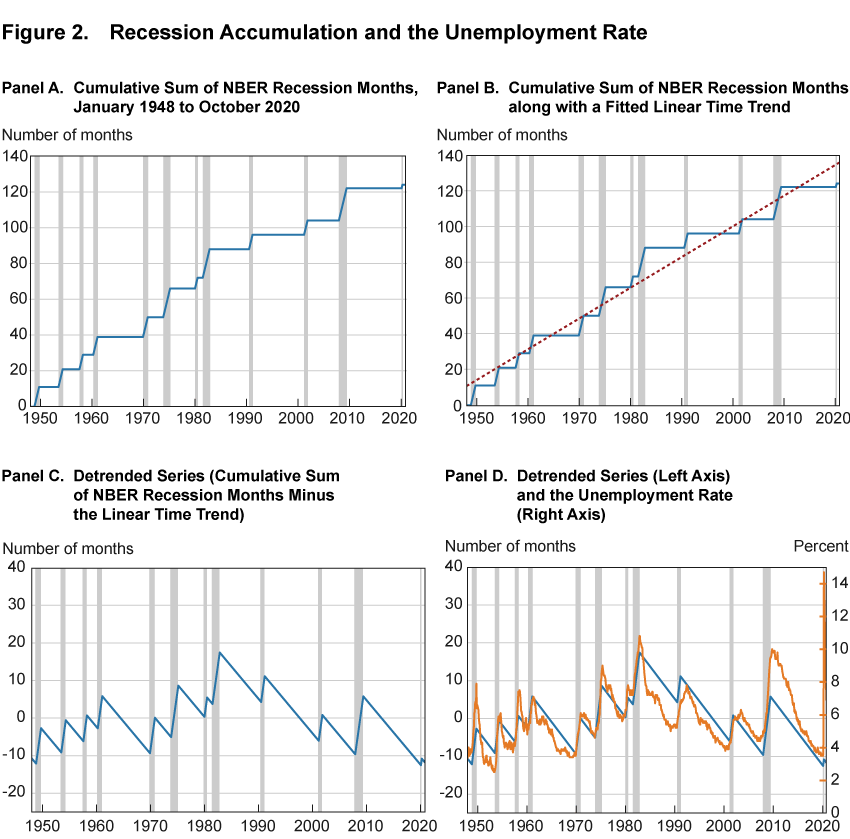

Figure 2 depicts a series of computations that result in a view of the alignment between recessions and the unemployment rate. This view of the alignment (panel D) highlights the intuition that frequent recessions, separated by short expansions, are associated with upward drift in the unemployment rate, while infrequent recessions, separated by long expansions, are associated with downward drift.

Note: Gray bars indicate recession periods.

Sources: US Bureau of Labor Statistics, Unemployment Rate [UNRATE], retrieved from FRED, Federal Reserve Bank of St. Louis (https://fred.stlouisfed.org/series/UNRATE), NBER-based Recession Indicators for the United States from the Period following the Peak through the Trough [USREC], retrieved from FRED, Federal Reserve Bank of St. Louis (https://fred.stlouisfed.org/series/USREC), and author’s calculations.

Panel A of figure 2 shows the cumulative sum of the National Bureau of Economic Research’s (NBER’s) recession months from January 1948 to October 2020. I define a recession as starting in the month following the NBER peak and ending in the month of an NBER trough. For the current period, the NBER announced a business cycle peak in February 2020 but has not announced a subsequent trough. In figure 2, I treat March and April 2020 as recession months.10

In panel B of figure 2, I fit a linear time trend to the cumulative sum of the NBER recession months with ordinary least squares. This time trend gives an estimate of how quickly recessions accumulate on average. Then in panel C, I remove the linear time trend from the cumulative sum and show a detrended cumulative sum of NBER recession months. This detrended cumulative sum shows when recessions have accumulated more quickly and less quickly than average.

The detrended cumulative sum in panel C rises at a constant rate in every recessionary month and falls at a constant but slower rate in every expansionary month. This structure implies that this variable may not fall to its previous low point if a recession cuts an expansion short. As a result, frequent recessions, separated by short expansions, can cause this detrended cumulative sum to drift up over time. This upward drift occurs with the four recessions that begin in 1948, 1953, 1957, and 1960 and again with the four recessions that begin in 1970, 1973, 1980, and 1981. In other words, both 1948 to 1960 and 1970 to 1982 are 13-year periods where recessions accumulated more quickly than average. In contrast, recessions accumulated less quickly than average during the long expansions that occur mostly since 1983 and also in the 1960s. During these periods, the detrended cumulative sum falls below its low point from previous expansions, creating downward drifts in the series.

The periods of rapid recession accumulation, 1948 to 1960 and 1970 to 1982, are also periods when the unemployment rate trend rises in figure 1. In contrast, periods when recessions accumulate less quickly than average, the 1960s, 1983 to 2000, and the 2010s, are all periods when the unemployment rate trend falls in figure 1. To make this comparison between the accumulation of recessionary months and the unemployment rate more explicit, panel D shows the detrended cumulative sum of NBER recession months (left axis) along with the unemployment rate (right axis). The two series move closely together and have a correlation of about 0.7, even including the unusually large spike in the unemployment rate in April 2020.

A positive correlation between the frequency of recessionary months and the unemployment rate is not surprising. The NBER’s Business Cycle Dating Committee uses labor market variables when assigning business cycle peaks and troughs.11 However, what is surprising about panel D is how closely the unemployment rate follows the detrended cumulative sum of recessionary months for such a long time—from 1948 to 2020.12 This is surprising because the US labor market has been driven by a variety of economic shocks along with changing government policies, labor market regulations, and demographics; yet, the unemployment rate closely tracks the stable and linear structure of the detrended cumulative sum of recessionary months. As with the detrended cumulative sum of recessionary months, the unemployment rate rises quickly in recessions but falls slowly in expansions, and these features cause the unemployment rate to trend up with frequent recessions and trend down with infrequent recessions.

Longer-Run Unemployment Rate Projections

The results in the previous section show that the unemployment rate trend is aligned closely with how quickly recessionary months accumulate. Consequently, the unemployment rate trend may not be easily separated from the business cycle with statistical techniques that estimate slow-moving trends, such as in Hodrick and Prescott (1997), to offer just one example. This is because the unemployment rate’s trend is itself related to business cycles.13 Instead, I model the unemployment rate and the NBER recession indicator, which has a value of zero in expansion months and a value of one in recession months, together with a statistical tool known as a VAR.

Using this VAR, I can produce longer-run projections of the unemployment rate in the spirit of the FOMC’s Summary of Economic Projections, which assumes that there will be no shocks to the economy in the future. I do this by producing forecasts of the unemployment rate while imposing that the recession indicator has a value of zero in all future periods.14

There are two important steps for computing the forecasts. First, I use data from January 1948 to February 2020 to estimate the parameters of the VAR. These parameters establish the statistical relationship between the unemployment rate and the recession indicator, allowing me to predict how the unemployment rate will move in the future under the hypothetical scenario of no future recessions. Second, I choose the initial conditions as a starting point for my forecasts.15 For example, I need to decide if I want to start my forecasts from a high unemployment rate or a low unemployment rate. Forecasters often use the most recent data as their starting points. However, they may also choose older data to check how accurate their projections would have been in the past.

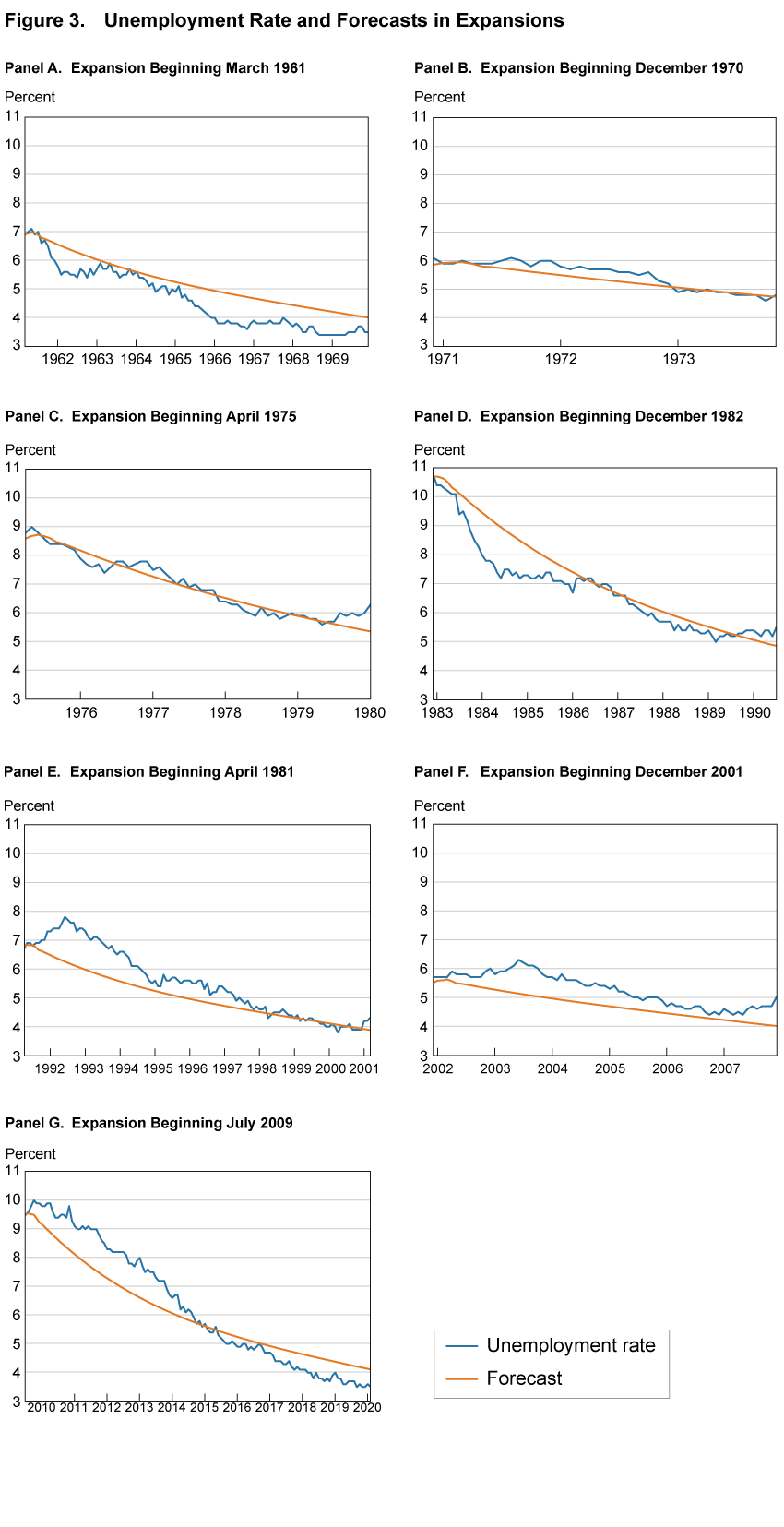

Figure 3 uses this latter approach. Each panel shows the unemployment rate for the 7 most recent NBER expansions.16 In addition, it shows the forecasts from the VAR under the hypothetical scenario of no recessions. I use the months before each expansion started as the starting point for the forecasts.

Note: Forecasts are computed under the hypothetical scenario of no future recessions.

Sources: US Bureau of Labor Statistics, Unemployment Rate [UNRATE], retrieved from FRED, Federal Reserve Bank of St. Louis (https://fred.stlouisfed.org/series/UNRATE), and author’s calculations.

While these forecasts do not perfectly track the unemployment rate over the course of an expansion, they generally match the downward trend of the unemployment rate in expansions. These forecasts also demonstrate relative accuracy in predicting where the unemployment rate will fall at the end of expansions. For the long expansion from 1991 to early 2001, the forecast predicts almost perfectly where the unemployment rate fell. For the other two longest expansions—1961 through 1969 and 2009 to early 2020—the forecast overpredicts where the unemployment rate fell to by about 0.6 percentage points.

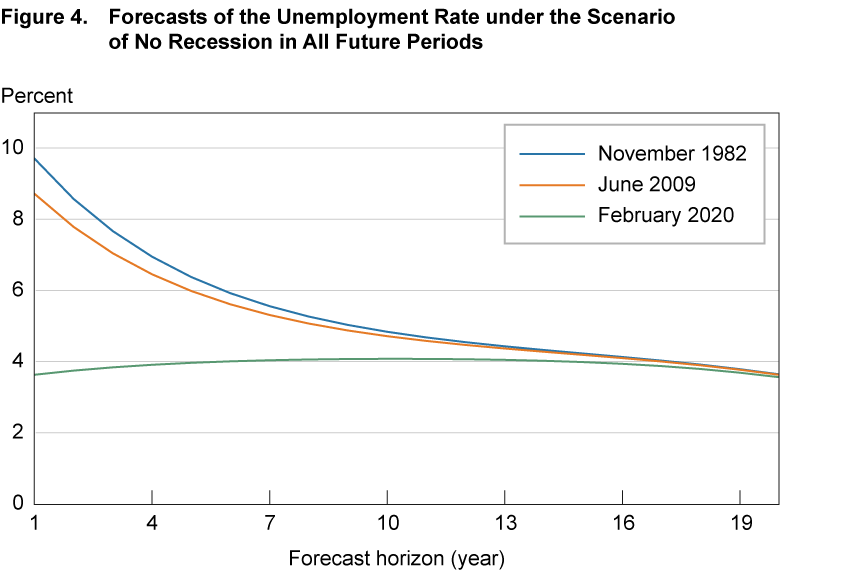

The longest expansion shown in figure 3 (panel G)—July 2009 to February 2020—lasted 10 years and 8 months. In order to compute unemployment rate forecasts in the spirit of the FOMC’s Summary of Economic Projections, which assumes that there will be no shocks to the economy in the future, I next consider how low the unemployment rate could fall in expansions that last much longer than 10 years and 8 months. Specifically, I produce forecasts by imposing no recessions for 20 years.17 In addition, I study the importance of the starting points for the forecasts by considering three different starting points. The first two are November 1982 and June 2009. These are the same starting points that I used in panels D and G of figure 3 and they coincide with the ends of the deepest recessions since 1948. The third starting point is February 2020, which is the last month in my estimation sample.

Figure 4 shows the 20-year forecasts. When using the November 1982 and June 2009 starting points, the forecasts start with the unemployment rate at high levels. This is natural as both of these starting points coincide with the end of recessions. In contrast, the forecasts generated with the February 2020 starting point start with a low level of the unemployment rate, a measure which is consistent with the healthy labor market at the start of 2020.

Note: The three lines correspond to three starting points: November 1982, June 2009, and December 2019.

Source: Author’s calculations.

The forecasts generated with the November 1982 and June 2009 starting points move down over time. The forecasts generated from the February 2020 starting point rise very slightly before falling again. The forecasts with all three initial conditions become very similar at about 20 years, showing that the starting point does not affect how low the VAR projects the unemployment rate will fall as long as expansions are sufficiently long. For each of the three starting points, the VAR projects that the unemployment rate will be about 3.6 percent after 20 years without a recession.18 That is, if one were to use this VAR to make a longer-run projection of the unemployment rate in the absence of further shocks to the economy as done in the FOMC’s Summary of Economic Projections, then one would project 3.6 percent.19

The value of the projections in figure 4 is that they provide an answer to where the unemployment rate could fall in a hypothetical world in which recessions do not occur, which I approximate with 20-year forecasts with no recessions. Of course, other choices of forecast length are possible. With shorter forecasts, the starting point of the forecast still matters. As shown in figure 4, the forecasts generated with the November 1982 and June 2009 starting points are not all the way down to 3.6 percent until about 20 years. I have also considered longer forecasts; however, I do not show these forecasts here because they also yield unemployment rates at 3.6 percent.

To check the robustness of my results, I drop early portions of my estimation sample and recompute the long-run forecasts under the assumption of no future recessions. Using samples of January 1958 to February 2020, January 1968 to February 2020, and January 1978 to February 2020, I compute the long-run forecasts of the unemployment rate to be 3.6 percent, 3.8 percent, and 3.6 percent, respectively. These values indicate that the early portions of my sample do not have a big impact on the results. Alternatively, if I use January 1948 to June 2009 as my sample, the long-run forecast is 3.9 percent. This sample choice shows that the 2010s, which were part of the longest expansion in US history, have only a small impact on the results. Overall, the findings suggest that how low the unemployment rate can fall in an expansion appears to be quite stable over a variety of sample periods.

Finally, to highlight how the assumption of no future recessions affects the forecast of the unemployment rate, I also compute the 20-year forecast of the unemployment rate without this assumption. This unconditional forecast of the unemployment rate is 5.7 percent, more than 2 percentage points above the forecast that assumes no future recessions. Clearly, when making longer-run projections of the unemployment rate, such as those in the FOMC’s Summary of Economic Projections, conditioning upon future recessions can make large changes in the projection.

Conclusions

The unemployment rate in the United States falls slowly in expansions, and it may not reach its previous low point before the next recession begins. This feature suggests that the unemployment rate trends up with frequent recessions and trends down when recessions are infrequent. In this Commentary, I show that the US unemployment rate indeed trended up with the rapid accumulation of recessions prior to 1983 and then trended down again with the slow accumulation of recessions after 1983. In addition, I estimate the relationship between recessions and the unemployment rate with a VAR. Long-run forecasts from this VAR under the scenario of no future recessions can be used to produce longer-run projections of the unemployment rate in the spirit of the FOMC’s Summary of Economic Projections. I find that the unemployment rate moves to 3.6 percent in the absence of future recessions.

Footnotes

- I use a tuning parameter of 106 for the Hodrick and Prescott (1997) filter. This parameter is higher than what academic researchers often use for monthly data. I choose this higher value to highlight the lower frequency variation in the data. Using the filter from Müller and Watson (2015) with frequencies of 12 years or longer produces a similar picture. Return to 1

- For example, Weiner (1993) argues that the natural rate of unemployment was about 6.25 percent in 1993 but about 6.7 percent in 1980. An important point is that Weiner (1993) accounts for inflation in his estimate of the natural rate of unemployment. However, the HP filter in figure 1 does not account for inflation, nor do I throughout this Commentary. Return to 2

- For example, see the handbook chapter of Rogerson and Shimer (2011), which like many other studies, uses the Hodrick and Prescott (1997) filter to separate the trend and cycle components of the unemployment rate. Return to 3

- See https://www.federalreserve.gov/monetarypolicy/files/FOMC_LongerRunGoals.pdf. Return to 4

- For the April 2012 FOMC meeting, the range of longer-run unemployment rate projections was 4.9 percent to 6.0 percent. For the September 2020 FOMC meeting, this longer-run unemployment rate range had fallen to 3.5 percent to 4.7 percent. Return to 5

- Weiner (1993), also discussed in footnote 2, emphasizes demographic change. See Crump, Eusepi, Giannoni, and Șahin (2019) for more recent analysis and discussion of demographics and the unemployment rate. Return to 6

- Neftçi (1984) and Sichel (1993) have previously documented that the unemployment rate changes asymmetrically over the business cycle, rising quickly in recessions and falling slowly in expansions. This Commentary draws out the implication that this asymmetry can affect the longer-run trend in the unemployment rate. Return to 7

- Consistent with the slower accumulation of recession months, 1983 roughly corresponds to beginning of the “Great Moderation,” a period in US history in which many economic variables became less volatile (Kim and Nelson, 1999; McConnell and Perez-Quirós, 2000; Stock and Watson, 2002). The results in this Commentary link the Great Moderation to theoretical models of unemployment rate asymmetry, such as Dupraz, Nakamura, and Steinsson (2019) and Lepetit (2020), who find that more stable economic environments imply lower average unemployment rates. That is, the general downward trend in the unemployment rate after 1983 is consistent with theoretical models that show that the average unemployment rate can fall with a reduction in economic volatility. Return to 8

- See the notes to table 1 of https://www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20200916.pdf. Return to 9

- See https://www.nber.org/research/data/us-business-cycle-expansions-and-contractions for a list NBER peaks and troughs. Return to 10

- The NBER’s Business Cycle Dating Committee also uses gross domestic product, gross domestic income, personal consumption expenditures, and personal income less transfers when assigning business cycle peaks and troughs. For an example of the Business Cycle Dating Committee’s reasoning, see https://www.nber.org/news/business-cycle-dating-committee-announcement-june-8-2020. Return to 11

- Consistent with this finding, Hall and Kudlyak (2020) document that the pace of reduction of the unemployment rate in expansions has been roughly stable for 70 years. Additionally, figure 2 implies that the pace of unemployment rate increases in recessions has also been roughly stable for 70 years. Return to 12

- Separating trends and business cycles is challenging for a wide variety of economic indicators. For example, Coibion, Gorodnichenko, and Ulate (2018) show that the Congressional Budget Office has historically made large changes to its measure of potential output around recessions. Return to 13

- I use the conditional forecasting approach in Doan, Litterman, and Sims (1983). I provide details of the VAR and the conditional forecasting exercise in a supplemental appendix. Return to 14

- Mathematically, these initial conditions are the values of the right-hand side variables in the VAR that are needed to produce the forecasts. See the supplemental appendix for additional details. Return to 15

- I exclude the expansion that began in August 1980 because this expansion lasted only one year. Return to 16

- I choose 20 years because that is the horizon at which forecasts appear to converge for all of the initial conditions in figure 4. If I only use a 15-year forecast horizon, the November 1982 and June 2009 initial conditions yield forecasts of the unemployment that fall to 3.8 percent, but it does not fall all the way to 3.6 percent as shown in figure 4. If I use horizons of 25 or 30 years, then the unemployment rate falls to 3.6 percent for all the initial conditions shown in figure 4, but it does not fall further. Return to 17

- This finding uses a VAR with 6 lags and is sensitive to the number of lags included in the VAR. I have checked lag lengths from 1 to 13 and found that the 20-year unemployment rate projection varies from a low of about 2.9 percent (with 13 lags) to a high of about 3.7 percent (with 1 lag). Hence, the results that I provide are conservative in the sense that different lag choices may yield materially lower unemployment rate projections, but none yields materially higher unemployment rate projections. Return to 18

- This long-run projection of 3.6 percent is very similar to Hall and Kudlyak’s (2020) steady-state unemployment rate of 3.5 percent. Hence, my results provide empirical support for Hall and Kudlyak’s choice of a steady state. In contrast, my long-run projection is materially above the steady-state of Dupraz, Nakamura, and Steinsson (2019), which is 4.6 percent. In addition, the conditional forecasts that I produce can provide data moments that may help researchers estimate labor market congestion functions as in Section 5.3 of Hall and Kudlyak (2020). Return to 19

References

- Coibion, Olivier, Yuriy Gorodnichenko, and Mauricio Ulate. 2018. “The Cyclical Sensitivity in Estimates of Potential Output.” Brookings Papers on Economic Activity, Fall: 343–411. https://www.doi.org/10.1353/eca.2018.0020.

- Crump, Richard K., Stefano Eusepi, Marc Giannoni, and Ayşegül Șahin. 2019. “A Unified Approach to Measuring u*.” Brookings Papers on Economic Activity, Spring: 143–214. https://www.doi.org/10.1353/eca.2019.0002.

- Doan, Thomas, Robert Litterman, and Christopher A. Sims. 1983. “Forecasting and Conditional Projection Using Realistic Prior Distributions.” NBER Working Paper, No. 1202. https://www.doi.org/10.3386/w1202.

- Dupraz, Stéphane, Emi Nakamura, and Jón Steinsson. 2019. “A Plucking Model of Business Cycles.” NBER Working Paper, No. 26351. https://www.doi.org/10.3386/w26351.

- Hall, Robert E., and Marianna Kudlyak. 2020. “Why Has the US Economy Recovered So Consistently from Every Recession in the Past 70 Years?” NBER Working Paper No. 27234. https://www.doi.org/10.3386/w27234.

- Hodrick, Robert J., and Edward C. Prescott. 1997. “Postwar US Business Cycles: An Empirical Investigation.” Journal of Money, Credit, and Banking, 29(1): 1–16. https://www.doi.org/10.2307/2953682.

- Kim, Chang-Jin, and Charles R. Nelson. 1999. “Has the US Economy Become More Stable? A Bayesian Approach Based on a Markov

- Switching Model of the Business Cycle.” Review of Economics and Statistics, 81(4): 608–616. https://www.doi.org/10.1162/003465399558472.

- Lepetit, Antoine, 2020. “Asymmetric Unemployment Fluctuations and Monetary Policy Trade-Offs.” Review of Economic Dynamics, 36: 29–45. https://doi.org/10.1016/j.red.2019.07.005.

- McConnell, Margaret M., and Gabriel Perez-Quirós. 2000. “Output Fluctuations in the United States: What Has Changed since the Early 1980s?” American Economic Review, 90(5): 1464–1476. https://doi.org/10.1257/aer.90.5.1464.

- Müller, Ulrich K. and Mark W. Watson, 2015. “Low-Frequency Econometrics.” NBER Working Paper, No. 21564. https://www.doi.org/10.3386/w21564.

- Neftçi, Salih N. 1984. “Are Economic Time Series Asymmetric over the Business Cycle?” Journal of Political Economy, 92(2): 307–328. https://www.doi.org/10.1086/261226.

- Rogerson, Richard, and Robert Shimer. 2011. “Search in Macroeconomic Models of the Labor Market.” Handbook of Labor Economics, Volume 4a, Chapter 7, 619-700. https://www.doi.org/10.1016/S0169-7218(11)00413-8.

- Sichel, Daniel E. 1993. “Business Cycle Asymmetry: A Deeper Look.” Economic Inquiry, 31(2): 224–236. https://www.doi.org/10.1111/j.1465-7295.1993.tb00879.x.

- Stock, James H., and Mark W. Watson. 2002. “Has the Business Cycle Changed and Why?” NBER Macroeconomics Annual, 17: 159–218. https://www.doi.org/10.1086/ma.17.3585284.

- Weiner, Stuart E. 1993. “New Estimates of the Natural Rate of Unemployment.” Federal Reserve Bank of Kansas City, Economic Review, Fourth Quarter: 53–63. https://ideas.repec.org/a/fip/fedker/y1993iqivp53-69nv.78no.4.html.

Suggested Citation

Lunsford, Kurt G. 2021. “Recessions and the Trend in the US Unemployment Rate.” Federal Reserve Bank of Cleveland, Economic Commentary 2021-01. https://doi.org/10.26509/frbc-ec-202101

This work by Federal Reserve Bank of Cleveland is licensed under Creative Commons Attribution-NonCommercial 4.0 International