- Share

Have Stress Tests Impacted Small-Business Lending?

The Federal Reserve conducts stress tests of the largest bank holding companies to ensure that the banking system has sufficient capital to stay financially sound in the event of worsening economic conditions. Some groups have raised concerns that the stress tests will reduce lending to small businesses. This article describes recent research investigating the impact of the stress tests on small-business lending. It finds that the banks that are most affected by stress tests have reduced their small-business credit, but aggregate credit to small businesses has not fallen.

The views authors express in Economic Commentary are theirs and not necessarily those of the Federal Reserve Bank of Cleveland or the Board of Governors of the Federal Reserve System. The series editor is Tasia Hane. This paper and its data are subject to revision; please visit clevelandfed.org for updates.

The 2008 financial crisis led to dramatic changes in the regulation and supervision of financial institutions, including one new requirement for a select group of large bank holding companies (BHCs): the annual stress test. Stress testing aims to ensure that in the event of worsening economic conditions, banks will have sufficient capital to absorb losses and be able to continue supplying credit to the economy.

Stress tests provide an estimate of how much capital a BHC might lose during a severe economic downturn, and that estimate is then translated into a forecast of the regulatory capital ratios the BHC would be required to hold under various economic scenarios. If the stress tests project large shortfalls in a BHC’s capital, the banks owned by that BHC are likely to be given the incentive to respond by reducing the risks in their current loan portfolios or by improving their current capital ratios by, for example, reducing planned dividend distributions or share repurchases.

Because lending to small businesses may be considered riskier than lending to large businesses, concerns have been raised that the stress tests might induce banks to reduce their lending to this market.1 The research on this topic suggests that banks facing regulatory capital constraints cut their lending, and stress tests create a direct link from bank lending risk to capital.2

This Commentary discusses new research that assesses the impact that stress tests have had on small-business lending (Cortés et al., forthcoming). We show that the banks most affected by stress tests reallocate small-business credit away from riskier markets to safer ones. They also raise interest rates on small-business loans in the markets in which they continue to lend. Loan quantities fall most in high-risk markets where stress-tested banks own no branches, and prices rise mainly where they have branches. These facts suggest that due to a stress-test-projected shortfall in regulatory capital, banks increase small-business loan prices in markets in which the banks have local knowledge and to exit markets in which they do not. Stress tests do not, however, reduce aggregate small-business credit. In geographies where small firms formerly relied on stress-tested lenders, small firms see no reduction in credit and likely find it from other local lenders.

A Brief History of Stress Testing

The first stress test in the United States was conducted by the Federal Reserve in 2009 during the financial crisis. Called the Supervisory Capital Assessment Program (SCAP), it was introduced to ensure that banks had sufficient capital coming out of the crisis to absorb losses in the event of another crisis. After the SCAP concluded, the Federal Reserve decided to continue stress testing on an annual basis, renaming the program the Comprehensive Capital Analysis and Review (CCAR). CCAR began in 2011 with the same set of large BHCs as the SCAP, those with total assets in excess of $100 billion, but in 2012, the set was expanded to include all 32 of the BHCs with assets above $50 billion. Starting in 2013, the Federal Reserve began implementing dual stress tests, one based on the CCAR process and the other based on compliance with the Dodd-Frank Act, called DFAST. The key difference between the two tests is that under CCAR, each BHC provides a proposed capital distribution plan that regulators incorporate into the stress test; under DFAST, regulators assume the bank’s capital distribution is held at its current level.3 The tests were originally disclosed in March of each year, but in 2016, the report date for the stress-test disclosure was moved to late June.4

Both CCAR and DFAST aim to evaluate what happens to each BHC’s capital under three possible economic scenarios—“baseline,” “adverse,” and “severely adverse”—nine quarters into the future. The scenarios reflect possible paths for aggregate economic variables. In 2017, the variables included “six measures of economic activity and prices: percent changes (at an annual rate) in real and nominal gross domestic product (GDP); the unemployment rate of the civilian noninstitutional population aged 16 years and over; percent changes (at an annual rate) in real and nominal disposable personal income; and the percent change (at an annual rate) in the consumer price index.”5 The stress tests map the effects of these variables’ hypothetical values on the capital ratios of each BHC over the course of the forecast.

By focusing on measures of economic activity and prices, the possible scenarios focus on aggregate rather than idiosyncratic risks to banks. This approach helps minimize the macroprudential risk of banks’ capital becoming collectively constrained during broad economic downturns. However, data on individual BHC positions and exposures to various risk factors are also incorporated into the stress tests. Thus, the results of the stress tests are based on common scenarios and a common model (i.e., the one developed by the Federal Reserve), but they account for differences in asset composition.6 The results are watched closely, not only by regulators, but also by bank managers, analysts, and investors, as they might lead to forced reductions in a BHC’s planned capital distributions, along with other operating changes, if the simulated decline in capital is sufficiently large. Stress tests have been widely adopted by regulatory authorities outside the United States, such as the Bank of England and the European Central Bank.

Research Methodology

In a recent study, my coauthors and I evaluate the effects of the stress tests on small-business lending during the 2012–2015 period (Cortés et al., forthcoming). We begin by developing several measures of the impact of the stress-test results on each stress-tested BHC in each year, that is, the degree to which capital ratios are projected to fall short of requirements in the various scenarios. We call these measures of “stress-test exposure.” Using these measures, we investigate whether the BHCs more affected by stress tests cut the supply of small-business lending more than those less affected.

Generally, there are two components to a cut in lending supply: One is a drop in the number of loans originated and the other is an increase in loan prices. Thus, we consider quantity and price separately. Finally, in addition to evaluating whether the stress tests reduced stress-tested banks’ lending to small businesses, we evaluate whether stress tests affected the overall supply of small-business loans.

Measuring Stress-Test Exposure

The Federal Reserve discloses the results of the stress tests for three capital ratios: the Tier 1 capital ratio, the total risk-based capital ratio, and the Tier 1 leverage ratio. The results reported are the projected values of these ratios (“stressed ratios”) for each BHC under the three scenarios over the forward-looking nine-quarter planning horizon in each annual test cycle.7 Stressed capital ratios thus capture changes in the value of BHC portfolios under stress. We use these stressed ratios to create our measure of stress-test exposure. For each BHC, we take the difference between each of the three stressed ratios and its respective regulatory threshold (6 percent for the Tier 1 ratio; 8 percent for the total risk-based capital ratio; and 4 percent for the Tier 1 leverage ratio) and then use the smallest difference of the three as that BHC’s degree of stress-test exposure:

Stress-test exposure = minimum (stressed Tier 1 capital − 6%; stressed total risk-based capital − 8%; stressed leverage ratio − 4%)

BHCs whose specific portfolios have the greatest downside risk would have the most stress-test exposure and would be closest to one of the regulatory capital ratio thresholds. Banks owned by these BHCs likely face pressure from the regulators either to reduce risk or improve their current capital ratios (for example, by reducing planned dividend distributions or share repurchases).

Finally, we identify the banks that are owned by each of the 32 CCAR stress-tested BHCs. We use Call Reports for this information. We assume measures taken by BHCs to address the results of the stress test will manifest in the behavior of their subsidiary banks.

The Impact of Stress-Test Exposure on Loan Quantities

To capture the response of small-business loan quantities to stress-test exposure, we use CRA loan origination data from 2012–2015, collected by the Federal Financial Institutions Examination Council at the subsidiary bank level. CRA reports include data on loans with commitment amounts below $1 million that are originated by financial institutions with more than $1 billion in assets. CRA data provide us with a complete record of new lending quantities by subsidiary banks of the stress-tested BHCs at the county–year level. We use these data to build the annual growth rate of new loan originations under $1 million, a threshold we interpret as loans to small businesses.

We merge the annual CRA data with stress-test exposure data based on the identity of a subsidiary bank’s parent BHC. Since the stress-test results were published in March during our study period, we operate under the assumption that the majority of the effect from the stress tests on small-business lending manifests within the next nine months of the year of the disclosure. In line with this assumption, we match, for example, CRA loan growth from December 2013 to December 2014 to the stress-test results reported in March 2014.8

We expect that the subsidiaries of BHCs with higher stress-test exposure will reduce their lending to small businesses. One can argue, however, that banks that are more inclined to take risks would both grow their loan portfolios faster and experience higher stress-test exposure, thus biasing up the direct effect of stress-test exposure on loan growth. To mitigate this concern, instead of evaluating the direct effect of stress-test exposure on CRA loan growth, we focus on interactions between stress-test exposure and risk and between stress-test exposure and access to soft information (measured by branch proximity to borrowers).

If a bank attempts to reduce its loan-risk exposure because of stress-test results, we should observe steeper reductions of small-business loan quantities in riskier markets. In addition, this reduction in the quantity of loans should be most pronounced in markets without branches. Without the close relationships to customers that branches enable, banks are less able to “price in” the higher capital burden from stress-test exposure in higher interest rates and instead they exit the market.

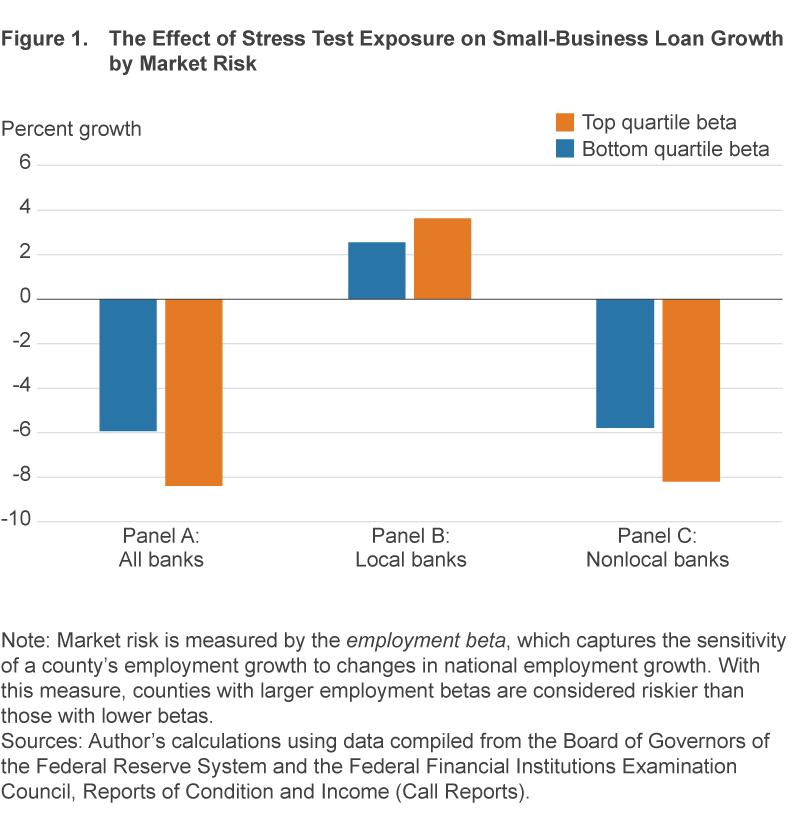

Since CRA data do not provide information about individual borrower risk, we build a county-level risk measure as a proxy measure for borrower risk. Using county employment data, we construct the employment beta, which captures the sensitivity of a county’s employment growth to changes in national employment growth. With this measure, counties with larger employment betas are considered riskier than those with lower betas.

The results suggest that banks with higher stress-test exposure are more likely to exit risky markets (counties). The estimates reported in panel A of 1 suggest that in response to a one standard deviation increase in stress-test exposure (=1.4 percent), markets in the top quartile of the employment beta distribution (beta = 1.36) would see a 2.5 percent greater decline in small-business loan originations than those in the bottom beta quartile (beta = 0.96).

We augment this analysis to evaluate whether the effect of stress testing on lending quantities differs across markets in which banks have and do not have an informational advantage through a branch presence. Panel B of figure 1 demonstrates small-business lending sensitivity to stress-test exposure in counties in which subsidiary banks have at least one branch; panel C demonstrates the results for counties in which lenders do not have a branch. We find that the effect of stress-test exposure on loan quantities is pronounced in markets in which banks have no branches, yet the effect is virtually nonexistent in markets in which banks have branches.

The evidence provided here offers a direct link between small-business loan originations and stress-test exposure. The decline in supplied loan quantities is more pronounced in riskier markets and in markets in which banks lack local knowledge because of the absence of a branch presence.

The Impact of the Stress-Test Exposure on Loan Prices

To analyze the impact of stress tests on loan prices, we use data from the Survey of Terms of Business Lending (STBL) covering a 2012:Q2–2017:Q2 sample. The Federal Reserve instituted the STBL to obtain timely information on the business-lending environment in the United States. The STBL collects data on loans originated by a random sample of banks during a full business week every three months (in February, May, August, and November). The selection of banks is conducted in a way that creates a representative sample of commercial and industrial loans. Consequently, large banks are more likely to be surveyed. The STBL data cover banks owned by 26 of the 32 stress-tested BHCs and provide detailed loan characteristics including loan size, the nominal interest rate, maturity, whether or not the loan comes with a prepayment penalty, collateral status, the state of the borrower, and so on. In addition to these characteristics, the STBL reports the lender’s internal risk rating for each loan. The rating ranges from 1 to 4, with 1 representing loans with the lowest risk level and 4 representing those with the highest risk level.9 Capturing loan risk helps alleviate the alternative explanations stemming from the bank risk preferences discussed earlier.

We map these quarterly STBL data to the annual BHC-level stress-test exposure data on a rolling basis based on the identity of a bank’s parent BHC. Since we want stress-test exposure to be predetermined with respect to our outcomes, we map each stress-test result into the next four STBL quarterly surveys. For example, we map the March 2013 values of stress-test exposures into STBL data from May 2013, August 2013, November 2013, and February 2014. Since 2016 stress-test results are reported in June, we map 2016 stress-test exposure measures to STBL data from August 2016, November 2016, February 2017, and May 2017. We then merge the STBL data with BHC financial characteristics by using Call Reports as of the last date available prior to the STBL loan cohort date. For example, we merge the STBL survey taken in August of 2013 with the (last available prior to August) June 2013 Call Report data.

Using a statistical model, we evaluate the impact of stress-test exposure on loan interest rates. Because factors other than stress-test results may explain why some loans carry higher or lower interest rates, we include in our model a loan risk level, other loan characteristics, BHC characteristics, and an indicator of whether a bank is local in a state, that is, if a bank has branches in a locality in which it lends. We also include a measure capturing local market demand (in statistical terms, state-quarter fixed effects). Based on the estimated results, we find that higher stress-test exposure corresponds to higher interest rates. In addition, stress tests affect loan pricing more in markets where banks have a local branch presence. Specifically, a one standard deviation higher stress-test exposure is associated with an increase in interest rates of 38 basis points in markets in which banks have a branch presence and with an increase of only 14 basis points in markets in which they do not have branches. The results are consistent with the notion that because of their informational advantage, banks with local knowledge are more able to increase prices without borrowers’ switching to other lenders.

We then split our analysis by borrower risk. Based on the estimated results, prices of low-risk loans do not change reliably with a bank’s stress-test exposure. Interest rates on medium-risk and high-risk loans, however, do increase robustly with higher stress-test exposure. The effect on rates in these two categories is also larger in areas in which banks have a local branch presence. Moreover, the impact of stress-test exposure on loan rates is the greatest for the high-risk loans in local markets.

Overall, banks more affected by stress tests increase interest rates on risky local loans more than banks that are less affected. In contrast, interest rates on low-risk loans do not change. These findings are consistent with the CRA-based evidence on quantities that suggests stress tests induce a shift away from riskier nonlocal markets toward local markets in which banks have an informational advantage.

The Impact of Stress-Test Exposure on Aggregate Small-Business Lending

Our results indicate that individual banks’ credit supply was affected by their exposure to stress tests. But this leaves the question of whether the stress tests constrain overall credit production. Perhaps lenders that were not affected by stress tests step in to lend to the displaced borrowers formerly served by stress-tested banks. And, as we have discussed, local stress-tested banks raise prices on risky loans and thus may continue to provide credit. To address this question, we revisit the CRA quantity data, but we now evaluate aggregate annual origination volumes in different markets (counties).

In our empirical model, we evaluate growth rates in small-business loan originations at the county level in each year. Given that local and nonlocal banks respond differently to stress-test exposure, we construct two county-level measures of exposure. The first, local banks’ stress-test exposure, equals the average exposure for all banks with branches in each county and year, weighted by banks’ local loan share in 2010 (before the first year of our sample). The second county-level exposure measure, nonlocal banks’ stress-test exposure, is built similarly and equals the average for banks without branches in each county and year and is also weighted by banks’ local loan share in 2010. If stress tests lead to tightening of aggregate small-business credit, then the estimated impact of the tests would be negative because an increase in stress-test exposure at a county level would be associated with credit contraction. Furthermore, since we find that nonlocal banks cut credit more than local ones, we might expect the results for the nonlocal measure to be larger in magnitude than for the local measure. To capture overall economic conditions at the county level, we include county and year fixed effects, along with possible local time-varying drivers of loan demand (housing price growth, employment growth, and income growth). Based on our results, we find no difference in aggregate credit origination across markets, regardless of local market reliance on small-business lending from local or nonlocal stress-tested banks.

One possible explanation for this result is that nontested (smaller) banks fill in the gap and lend to businesses that the stress-tested banks no longer serve. To test this conjecture, we examine the relationship between stress-test exposure and the share of loans originated by local banks unaffected by stress tests: banks with assets below $10 billion.10 We empirically confirm that small, local banks increase their share when stress-tested banks are closer to binding capital requirements. These results, taken together with the results discussed earlier, suggest that small banks unaffected by stress testing, and perhaps nonbank lenders as well, substitute in for large, nonlocal banks in lending to small businesses.

Conclusions

Our results suggest that banks more affected by stress tests have reduced their supply of loans to small businesses, and this reduction has been concentrated among relatively riskier small-business borrowers and riskier markets. Loan quantities fall more in markets in which stress-tested banks do not own branches near borrowers, and prices rise predominantly where they do. These differential responses emphasize the importance of market structure and branch location in mediating the impact of capital requirements on credit supply. Aggregate credit, however, has not been adversely affected by stress tests. Instead, credit seems to be supplied by small, local lenders when large stress-tested banks exit those markets.

Our results suggest that stress tests qualitatively work as intended. We observe that tested lenders either reduce their exposure to risk or, when they don’t, they increase their compensation for bearing that risk. These changes would be efficiency-enhancing if large banks were taking on too much risk and extending too much credit prior to the financial crisis, as they would under theories of moral hazard incentives from deposit insurance and “too big to fail” expectations. Regulations that accurately tie loan risk to required capital can help alleviate these distortions. Stress tests may help with these objectives by moving small-business credit supply from large, nonlocal lenders toward smaller banks with more local knowledge.

Footnotes

- The Clearing House, an advocate for banks, points specifically to the stress tests as imposing unduly harsh (implicit) capital requirements on small-business loans and on residential mortgages (Covas, 2017a and 2017b). Return to 1

- A large academic literature on bank “capital crunches” documents that shocks to bank equity capital have large contractionary effects on the supply of lending (Bernanke, 1983; Bernanke, Lown, and Friedman, 1991; Kashyap and Stein, 1995; Kashyap and Stein, 2000; Houston, James, and Marcus, 1997; Peek and Rosengren, 1997; Peek and Rosengren, 2000; Campello, 2002; Calomiris and Mason, 2003; Calomiris and Wilson, 2004; Cetorelli and Goldberg, 2012; Cortés and Strahan, 2017). Return to 2

- There are other differences between the CCAR and DFAST; see the following documentation for more details: https://www.federalreserve.gov/newsevents/press/bcreg/dfast_2013_results_20130314.pdf. Return to 3

- For 2019, the Federal Reserve proposed more changes to the stress tests, “providing relief to less-complex firms from stress testing requirements and CCAR by effectively moving the firms to an extended stress test cycle for this year. The relief applies to firms generally with total consolidated assets between $100 billion and $250 billion.” https://www.federalreserve.gov/newsevents/pressreleases/bcreg20190205b.htm. We do not use the most recent data for our analysis. Return to 4

- 2017 Supervisory Scenarios for Annual Stress Tests Required under the Dodd-Frank Act Stress Testing Rules and the Capital Plan Rule: https://www.federalreserve.gov/newsevents/pressreleases/files/bcreg20170203a5.pdf. Return to 5

- Banks are required to create their own models of stress testing but neither the Federal Reserve’s nor the banks’ internal models are available to the public. Return to 6

- Our data for 2012 are taken from the Federal Reserve’s CCAR disclosure, but we use the series of results that do not include the bank’s capital distribution plan. Data from 2013–2016 are taken from the disclosure under the Dodd-Frank Act. In other words, our sample includes only the CCAR banks, but the measure of exposure is the one used for compliance with DFAST, which does not incorporate the bank’s capital distribution plan. Several other regulatory capital ratios are used in some of the stress-test cycles, but the three we use are the only ones available consistently across all cycles. Return to 7

- We limited the period of our analysis to 2012–2015 because the publication date of the results was moved in 2016 from March to June. At the time of our research, we had data through the end of 2016, but because CRA data are annual and the 2016 stress test results would not be released until June, lending adjustments made in response to the stress-test results were unlikely to be properly captured by 2016 annual data on small-business lending growth. Return to 8

- The risk rating in the raw data ranges from 0 to 5. We exclude from consideration distressed loans (risk rating = 5) that do not reflect new originations. Furthermore, since controlling for risk is an important factor in our identification strategy, we exclude from consideration unrated loans (risk rating = 0). Return to 9

- We use the $10 billion cut-off to ensure the banks are not affected by any stress tests. In 2014, the stress-test process was expanded to banks with total assets between $10 billion and $50 billion under the Dodd-Frank Act. However, stress tests of banks with assets between $10 billion and $50 billion were not disclosed before 2016. Return to 10

References

- Bernanke, Ben S. 1983. “Nonmonetary Effects of the Financial Crisis in the Propagation of the Great Depression.” American Economic Review, 73(3): 257–276. http://www.jstor.org/stable/1808111

- Bernanke, Ben S., Cara S. Lown, and Benjamin M. Friedman. 1991. “The Credit Crunch.” Brookings Papers on Economic Activity, 1991(2): 205. https://www.doi.org/10.2307/2534592

- Board of Governors of the Federal Reserve System. 2013. “Dodd-Frank Act Stress Test 2013: Supervisory Stress Test Methodology and Results.” Technical Report, Board of Governors of the Federal Reserve System. https://www.federalreserve.gov/newsevents/press/bcreg/dfast_2013_results_20130314.pdf

- Board of Governors of the Federal Reserve System. 2019. “Federal Reserve Board Releases Scenarios for 2019 Comprehensive Capital Analysis and Review (CCAR) and Dodd-Frank Act Stress Test Exercises.” Press Release. https://www.federalreserve.gov/newsevents/pressreleases/bcreg20190205b.htm

- Calomiris, Charles W., and Joseph R. Mason. 2003. “Fundamentals, Panics, and Bank Distress during the Depression.” American Economic Review, 93(5): 1615–1647. http://www.jstor.org/stable/3132145

- Calomiris, Charles W., and Berry Wilson. 2004. “Bank Capital and Portfolio Management: The 1930s ‘Capital Crunch’ and the Scramble to Shed Risk.” The Journal of Business, 77(3): 421–455. https://www.doi.org/10.1086/386525

- Campello, Murillo. 2002. “Internal Capital Markets in Financial Conglomerates: Evidence from Small Bank Responses to Monetary Policy.” The Journal of Finance, 57(6): 2773–2805. https://doi.org/10.1111/1540-6261.00512

- Cetorelli, Nicola, and Linda S. Goldberg. 2012. “Banking Globalization and Monetary Transmission.” The Journal of Finance, 67(5): 1811–1843. https://doi.org/10.1111/j.1540-6261.2012.01773.x

- Cortés, Kristle R., Yuliya Demyanyk, Lei Li, Elena Loutskina, and Philip Strahan. Forthcoming. “Stress Tests and Small Business Lending.” Journal of Financial Economics. https://doi.org/10.1016/j.jfineco.2019.08.008

- Cortés, Kristle R., and Philip E. Strahan (2017). “Tracing Out Capital Flows: How Financially Integrated Banks Respond to Natural Disasters.” Journal of Financial Economics, 125(1): 182–199. https://doi.org/10.1016/j.jfineco.2017.04.011

- Covas, Francisco. 2017a. “The Capital Allocation Inherent in the Federal Reserve’s Capital Stress Test.” Technical Report, The Clearing House. https://www.theclearinghouse.org/research/articles/2017/01/-/media/20d957fe6fdc4607b5c24eb8506a5de5.ashx

- Covas, Francisco. 2017b. “Capital Requirements in Supervisory Stress Tests and Their Adverse Impact on Small Business Lending.” The Clearing House, Staff Working Paper 2017-2. https://www.theclearinghouse.org/research/articles/2017/08/capital-requirements-supervisory-stress-tests-adverse-impact-small-business-lending

- Houston, Joel, Christopher James, and David Marcus. 1997. “Capital Market Frictions and the Role of Internal Capital Markets in Banking.” Journal of Financial Economics, 46(2): 135–164. https://doi.org/10.1016/s0304-405x(97)81511-5

- Kashyap, Anil K., and Jeremy C. Stein. 1995. “The Impact of Monetary Policy on Bank Balance Sheets.” Carnegie-Rochester Conference Series on Public Policy, 42: 151–195. https://doi.org/10.1016/0167-2231(95)00032-u

- Kashyap, Anil K., and Jeremy C. Stein. 2000. “What Do a Million Observations on Banks Say about the Transmission of Monetary Policy?” American Economic Review, 90(3): 407–428. https://doi.org/10.1257/aer.90.3.407

- Peek, Joe, and Eric S. Rosengren. 1997. “The International Transmission of Financial Shocks: The Case of Japan.” American Economic Review, 87(4): 495–505. https://www.jstor.org/stable/2951360

- Peek, Joe, and Eric S. Rosengren. 2000. “Collateral Damage: Effects of the Japanese Bank Crisis on Real Activity in the United States.” American Economic Review, 90(1): 30–45. https://doi.org/10.1257/aer.90.1.30

Suggested Citation

Demyanyk, Yuliya. 2019. “Have Stress Tests Impacted Small-Business Lending?” Federal Reserve Bank of Cleveland, Economic Commentary 2019-19. https://doi.org/10.26509/frbc-ec-201919

This work by Federal Reserve Bank of Cleveland is licensed under Creative Commons Attribution-NonCommercial 4.0 International