- Share

What Constitutes Substantial Employment Gains in Today's Labor Market?

The Federal Open Market Committee (FOMC) has tied its asset purchases to a “substantial improvement” in labor market conditions. While we don’t speculate on what the FOMC means by substantial improvement, we do explore the level of monthly job gains that would gradually deliver the underlying trend unemployment rate within a reasonable timeframe, under several plausible scenarios. We find that the path of monthly job gains, which is highly dependent on a few key parameters, is likely to be smaller than the path associated with previous recoveries.

The views authors express in Economic Commentary are theirs and not necessarily those of the Federal Reserve Bank of Cleveland or the Board of Governors of the Federal Reserve System. The series editor is Tasia Hane. This paper and its data are subject to revision; please visit clevelandfed.org for updates.

The Federal Open Market Committee (FOMC) announced in its December 2012 statement that asset purchases will continue as long as the outlook for labor markets does not improve substantially.1 This made the overall size of the purchase program a function of the labor market outlook, along with the program’s “likely efficacy and costs.”

There are many measures of labor market conditions, and the FOMC is likely to consider a broad range of indicators when it determines whether improvement qualifies as substantial.2 Nonetheless, employment growth and the unemployment rate are the most closely followed labor market measures and the best contemporaneous indicators of labor market conditions.3 Looking at those two measures, we explore the level of employment growth that might best represent a substantial employment gain.

One way to approach the question is to look back at periods of strong growth in past recoveries. We have data going back to 1939, and looking at the best six-month period of employment growth in the U.S. economy (February 1946 to August 1946), we observe job gains of over a half million per month. With the size of today’s labor market, that rate of growth would represent almost 2 million new jobs per month! Even the 75th percentile for growth in any six-month period since then suggests a monthly rate of job gains now of around 450,000.

Obviously, these numbers would be great going forward, but any current benchmark should fall within the realm of possibility given today’s labor markets. Moreover, simple comparisons across previous recoveries don’t account for potential changes over time in the underlying determinants of employment growth. So instead of a historical comparison, we use an economic model to evaluate the employment gains associated with progress on the unemployment rate.

The model allows us to explore the impact of three critical factors influencing employment growth trends. These factors are the projected level of aggregate output growth, slowing growth of the U.S. labor force, and less dynamism in the U.S. labor market relative to the 1980s. We show that each of these channels has important effects on the expected path of improvements in the labor market. For us, an improvement in the labor market corresponds to a reduction in labor market slack—that is, a decline in the unemployment rate toward its long-run trend (or natural rate), which is estimated to be 5.8 percent. Our figure is on high side of the central tendencies of the FOMC’s projections for long-run unemployment, which go from 5.2 to 6 percent.4 Ultimately, the level of improvement that is deemed “substantial” will be in the eye of the beholder, but we will consider outlooks which make steady and meaningful progress in lowering unemployment toward this natural rate.

Overall, we find that the current economic environment is associated with smaller employment gains than have been typically seen in the past. Indeed, the scenarios that we view as relevant in today’s economic environment would produce average employment gains of 150,000 per month or less for the current year.

A Simple Model of Output and Labor Markets

In order to quantify the extent of the employment gains that would be consistent with an improvement in the labor market, given current conditions, our model of labor markets explicitly incorporates the level of economic growth, the labor force participation rate, and the level of dynamism in the labor market as defined by job finding and separation rates. The model is based on Tasci (2012), which accounts for the effects of job finding and job separation rates on the unemployment trend, modified to incorporate changes in the labor force participation rate.5

Our model treats each of the four variables as a combination of a trend component, which moves relatively slowly over time, and a cyclical component, which fluctuates with the business cycle. Cyclical changes in the job separation, job finding, and labor force participation rates are related directly to the movements in the cyclical component of real output. For instance, a deep recession will generate a sharp decline in the job finding rate and a large rise in the separation rate, as well as a decline in the participation rate. As the cyclical component of output gradually disappears, output growth will gradually return to its long-run trend, and the unemployment flow and labor force participation rates will return to their trend levels at a rate based on their past adjustment history.

Using data on unemployment flow rates, labor force participation rates, and real GDP between 1948:Q1 through 2013:Q1, we estimate the model and calculate the trend components for all the variables.6 We call this our model scenario. These trend estimates are based on the historical behavior of all the variables in the model. The model indicates a current unemployment rate trend of 5.8 percent (which can be interpreted as a natural rate), along with a significant output gap (−2 percentage points as of last quarter).

The model indicates that today’s labor force participation rate of 63.3 percent is essentially very close to its trend, 63.6 percent—no doubt a reflection of the length of time that the participation rate has declined since the end of the recession and its history of being only slightly cyclical. Finally, our estimates confirm that the flows of people into and out of unemployment continue to be low, primarily reflecting a long-run decline in turnover trends that has been previously identified in related work (Tasci, 2012; Tasci and Zaman, 2010).

Based on the typical cyclical response to an output gap, the model projects a relatively strong recovery in economic growth for the current year (3.1 percent), which reduces the output gap to below 1 percent by the end of the year. In this model, that recovery path reduces the projected unemployment rate gradually to below 6.5 percent by 2014:Q3. Given this path of the unemployment rate and the modeled labor force participation rate, we can calculate an expected number of monthly employment gains that is consistent with a relatively strong labor market recovery.7 This employment gain is defined in terms of the household survey (which is used in the unemployment rate calculation), but, on average, over time, the payroll employment gains should be similar.

Two results stand out in this projection under the model scenario. First, once the unemployment rate reaches 5.8 percent in the long run, employment gains of only 46,000 a month would be sufficient to keep it there. This is a direct consequence of the slow labor force growth projected by the declining trend in the participation rate in our model scenario. Second, monthly gains of 149,000 are sufficient to bring the unemployment rate down gradually to 7 percent by the end of the year and to lower the unemployment rate below 6.5 percent by the third quarter of 2014. Labor market slack is completely eliminated by the end of 2015.

While the model estimates are interesting, they build in statistical estimates, and therefore modeling assumptions, for the three critical factors cited above when determining the employment gains per month. Each of these factors is subject to some debate, and alternative estimates are worth considering. For example, the economic forecasts of most economists suggest that the baseline projection for GDP growth in our model is overly optimistic in the near term. Similarly, other researchers have suggested that the labor force participation rate might have more of a cyclical component than our model projection implies. Finally, since labor market turnover declined significantly over time, exploring its potential impact would be useful.

To investigate the quantitative importance of these factors, we construct three additional scenarios using alternative assumptions for each.

Near-Term Output Growth

The model generates projections without considering any data other than the four variables described previously. Other data, such as personal consumption, investment, and trade, which are typically used by economic forecasters to improve the precision of near-term growth estimates, are not included. In the model scenario, we project an average growth rate of 3.1 percent for output this year, which gradually slows until it reaches its trend growth rate of 2.2 percent in 2016. We think this is an overly optimistic forecast for the current year, given the concerns about the fiscal drag and weak global demand.

To highlight the importance of a slower recovery of output, we construct another scenario from our model, in which the near-term GDP path follows the projections of the Survey of Professional Forecasters (SPF).8 We call this the SPF GDP scenario. The SPF expectation for growth this year is much lower, around 2.3 percent.9 When it is incorporated into the model, the picture for employment growth is considerably weaker, and improvement in the unemployment rate is relatively slow (table 1). In particular, unemployment dips only to 7.3 percent by year-end and then takes until 2015:Q3 to decline below 6.5 percent. The implied gradual improvement is consistent with employment growth, barely 108,000 jobs per month in 2013, and 92,000 in 2014. Comparing the model and SPF GDP scenarios highlights the significant role that near-term output growth plays in the employment growth picture.

Table 1. Employment Growth under Different Scenarios

| Average monthly employment gains, thousands | |||||

|---|---|---|---|---|---|

| Model scenario | SPF GDP | Cyclical LFPR | 1980s labor market | SPF GDP with cyclical LFPR | |

| Turnover: Low GDP: High LFPR: Trend |

Turnover: Low GDP: Low LFPR: Trend |

Turnover: Low GDP: High LFPR: Cyclical |

Turnover: High GDP: High LFPR: Trend |

Turnover: Low GDP: Low LFPR: Cyclical |

|

| 2013 | 149 | 108 | 147 | 222 | 106 |

| 2014 | 160 | 92 | 225 | 119 | 165 |

| 2015 | 104 | 156 | 174 | 80 | 224 |

| Long run | 46 | 46 | 84 | 46 | 84 |

| 6.5 percent unemployment rate by … | 2014:Q3 | 2015:Q3 | 2014:Q3 | 2013:Q4 | 2015:Q3 |

Note: Monthly employment gains for 2013 include the Q1 average of only 21,000 per month from the household survey.

Cyclical Participation

In our model scenario projection, we estimate the trend and cyclical components of the labor force participation rate over time by projecting the historical behavior of the variables in the model forward. Since historical participation rate movements have been only mildly cyclical, the model predicts a very small cyclical component for the participation rate in the future. But this prediction might not be very reliable if the current episode represents a breakdown in this historical pattern—which seems a possibility, given that the response of the labor force participation rate in this recession has been exceptionally drastic relative to past recessions.

Ultimately, the degree to which the labor force participation rate recovers will depend on how much of the recent decline in the rate is cyclical and how much is trend. This is hard to forecast, and there is evidence on both sides.

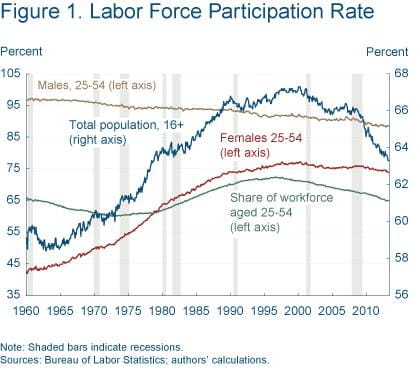

It is very clear, for example, that demographic trends that are not related to cyclical factors have driven the participation rate up and down substantially over time. Since the 1950s, two key demographic trends have significantly altered the participation trend. First, from 1950 until around 2000, more women continuously joined the labor force, driving a strong secular increase in the overall participation rate (figure 1). Second, from the 1970s until the late 1990s, a large baby boom generation drove up the share of the population that was in its prime working years, which also served to boost the participation rate. Neither of these factors has boosted participation recently, and models which account for the demographic structure of the population have been projecting declines in participation for some time, for example, Fallick and Pingle 2007.

Note: Shaded bars indicate recessions.

Sources: Bureau of Labor Statistics: authors' calculations.

Over the same period, movements in the participation rate and the business cycle were weakly correlated. During recessions, the overall participation rate declined somewhat and later reversed course as the recovery picked up. One can expect some recently unemployed workers to get discouraged and temporarily drop out of the labor force during a recession. Similarly, potential new entrants to the labor force and the recently unemployed might choose to go to school instead of looking for work, thereby reducing the participation rate during a recession. These patterns might be reversed as the economy recovers and participation increases. Recent research on the participation rate has argued that cyclical factors such as these might have played a bigger role in the current episode than otherwise thought, and some of the recent decline might be temporary.10

But in the most recent recoveries, there has been little indication of a post-recession bounce back in labor force participation. Therefore, the trend reversal around 2000, partly due to retirement of the baby boomers and the aging workforce, seems to have dominated the overall labor force participation picture in the last 15 years.

In the model scenario, the trend participation rate stands at 63.6 percent and is projected to decline by 0.33 percentage points per year. This view may be somewhat pessimistic, but recent work by Aaronson and Brave (2013) carefully explores the implication of the labor force participation trend and argues that trend employment growth per month will fall to around 35,000 by the end of the decade. Their results are consistent with our long-run estimates in the model scenario.

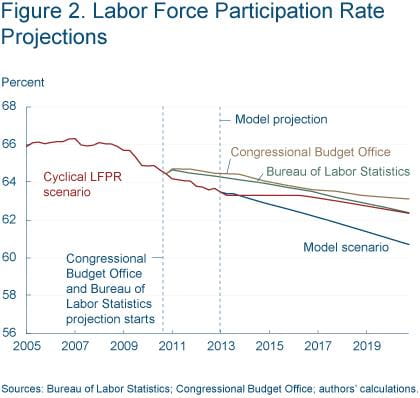

To illustrate the impact that a more significant cyclical component would have on the near-term labor force participation rate, we construct the cyclical LFPR scenario. It assumes that the actual trend of the participation rate is higher than our baseline estimate, at 64 percent, and the annual decline in the underlying trend is similar to the level estimated prior to the recession, 0.2 percentage points per year. Under this projected path, the labor force participation rate stays at its current level until it reaches the trend, implying a gradual cyclical recovery in the participation rate relative to trend, similar to the path projected by Van Zandweghe (2012). We believe the two different paths for the labor force participation rate from the model and cyclical LFPR scenarios provide an interesting contrast in outcomes within the plausible set of alternatives.

Figure 2 shows a comparison of these two paths with the most recently available participation rate projections from two public sources: the Bureau of Labor Statistics (BLS) and the Congressional Budget Office (CBO),11 although both sources have substantially underestimated the extent of the decline within the past two years by as much as one full percentage point. Neither of these published alternatives have been updated for the recent data, but the more optimistic path (cyclical LFPR scenario) gradually converges toward the BLS projections and runs nearly parallel to the CBO projections, once the cyclical nonparticipation is absorbed.

Sources: bureau of Labor Statistics: Congressional Budget Office; authors' calculations.

To understand the impact on employment growth of a more cyclical response in the participation rate relative to the baseline, we compare the model scenario and the cyclical LFPR cases, since the assumptions about output and flow rates are the same. The comparison highlights the long-term differences, as well as the medium-term adjustment in terms of employment gains. While both outcomes converge to similar unemployment rates over a similar period of time, the higher labor force participation rate in the cyclical LFPR scenario leads to more employment growth throughout the projection period, including almost twice as much employment growth in the long run when unemployment reaches its trend value.

Slowdown in Labor Market Turnover

Another crucial factor that will affect progress in the labor market is the role of labor market turnover, more specifically, the average rates at which workers find and lose jobs. Turnover is important, because it determines the speed with which labor markets reshuffle workers in response to the shock of a recession.

Labor market adjustment, the process through which people find jobs and jobs find people, takes time and resources. Even in the best of times, unemployment and job openings might coexist. In a dynamic labor market, where both of the underlying flow rates are high, the reshuffling happens much more quickly and as a result, unemployment adjusts quickly to its long-run level. If the flow rates are low, adjustment to the long-run trend takes place more slowly. Note that it is only the adjustment time that is a function of the churning process, not necessarily the unemployment rate trend.

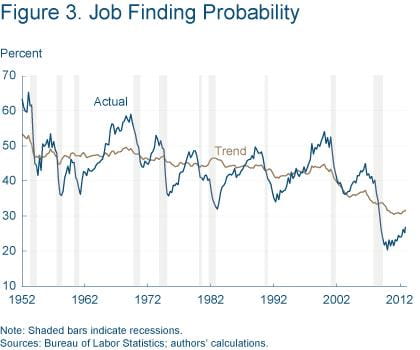

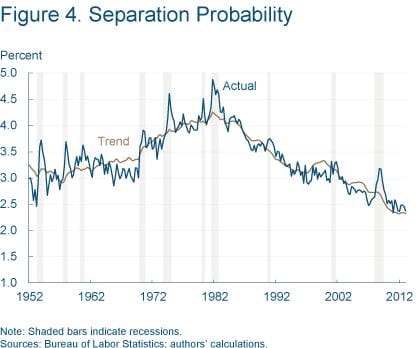

One defining feature of the U.S. labor market over the last decade has been the marked decrease in both of these flow rates, hence a slowdown in overall turnover (figures 3 and 4). This trend, which started in the 1980s, has been well documented for the separation rate. More recently, our research has found that even the average job finding rate has suffered a notable decline, and it has become more pronounced in the last decade and a half.12

Note: Shaded bars indicate recessions.

Sources: Bureau of Labor Statistics: authors' calculations.

Note: Shaded bars indicate recessions.

Sources: Bureau of Labor Statistics: authors' calculations.

This slower rate of turnover has hampered progress on the unemployment rate. The same mechanism also implies that average payroll gains per month will be substantially smaller in the short run, as unemployment approaches its natural rate, than in more dynamic labor markets.

To highlight the importance of labor turnover, we contrast the results from the model scenario with those of a counterfactual scenario in which we assume levels of turnover that were observed in the 1980s. This scenario, labeled 1980s labor market in table 1, has both job finding and separation trend rates higher than current rates by almost 70 percent, such that the implied long-run unemployment rate is just below 6 percent, identical to the other cases.13

This specific, and unfortunately highly unlikely, combination of high turnover and strong output recovery implies an exceptionally quick adjustment in the unemployment rate, ending in 2013 at 6.5 percent. This path of improvement in the labor market implies almost 50 percent higher employment gains per month in 2013, relative to the model scenario. The dynamism and the stronger output growth of this scenario were characteristic of the early 1980s. Not surprisingly, the early 1980s recovery had a sharp rebound in employment accompanied by a sharp decline in unemployment, similar to the 1980s labor market scenario.

Conclusion

Having walked through a range of different assumptions and scenarios in table 1, it should be clear that unless labor markets swiftly return to the dynamism of the 1980s, we are unlikely to see sustained employment gains above 200,000 per month this year. Indeed, several of the scenarios we considered pointed to significantly smaller expected employment gains.

To clarify this expectation, we also produced a scenario in which we combine some plausible alternatives. This scenario is not a forecast, but instead represents a particularly interesting combination of factors that influence expected employment growth. It includes a continuation of current labor market turnover rates, the GDP growth path currently forecasted by professional forecasters, and, perhaps most optimistically, a cyclical bounce-back in the participation rate. It’s labeled SPF GDP with cyclical LFPR in table 1.

This combination of factors produces employment growth this year of 106,000. This growth rate picks up (165,000 workers per month next year and then 224,000 in 2015) as output growth accelerates, ultimately driving the unemployment rate below 6.5 percent by the third quarter of 2015. Importantly, given the economic conditions built into this projection, these are outcomes that could be characterized as consistent with the economy making steady progress to full employment.

What is very clear about this scenario, and most of the other scenarios that we considered, is that the buoyant monthly employment gains that accompanied prior recoveries are not likely to be repeated. Indeed, even if GDP growth were to surprise on the high side (3.1 percent for 2013 as illustrated in the cyclical LFPR scenario), employment growth generated by our model would still be just 147,000 per month in the current year, even though the economy would be on a path to a 6.5 percent unemployment rate by the third quarter of 2014.

Ultimately, the degree of change in employment growth or the unemployment rate required to represent a “substantial” amount of progress in the labor market outlook is a subjective judgment. However, the pattern of employment growth that the economy will generate over a multiyear span depends importantly on output growth, the trend paths of labor market dynamism, and labor force participation. In this Commentary we used a simple model of labor markets to demonstrate why it is reasonable to think that the monthly pace of employment gains is likely to be smaller than the U.S. has seen in past recoveries.

References

- Aaronson, Daniel, and Scott Brave, 2013. “Estimating the Trend in Employment Growth,” Federal Reserve Bank of Chicago, Chicago Fed Letter, 2013-312.

- Aaronson, Daniel, Jonathan Davis, and Luojia Hu, 2012. “Explaining the Decline in the U.S. Labor Force Participation Rate,” Federal Reserve Bank of Chicago, Chicago Fed Letter, 2012-296.

- Erceg, Christopher J., and Andrew T. Levin, 2013. “Labor Force Participation and Monetary Policy in the Wake of the Great Recession,” Federal Reserve Bank of Boston, paper.

- Fallick, Bruce, and Jonathan Pingle, 2007. “A Cohort-Based Model of Labor Force Participation,” Finance and Economics Discussion Series 2007-09. Federal Reserve Board.

- Hotchkiss, Julie L., and Fernando Rios-Avila, 2013. “Identifying Factors behind the Decline in the U.S. Labor Force Participation Rate,” Business and Economic Research, 3(1). Macrothink Institute.

- Pissarides, Christopher A., 2000. Equilibrium Unemployment Theory. Cambridge, MA: MIT Press.

- Schweitzer, Mark, and Jennifer Ransom, 1999. “Measuring Total Employment: Are a Few Million Workers Important?” Federal Reserve Bank of Cleveland, Economic Commentary.

- Tasci, Murat, and Saeed Zaman, 2010. “Unemployment after the Recession: A New Natural Rate?” Federal Reserve Bank of Cleveland, Economic Commentary, 2010-11.

- Tasci, Murat, 2010. “The Ins and Outs of Unemployment in the Long Run: Unemployment Flows and the Natural Rate,” Federal Reserve Bank of Cleveland, working paper no. 2010-17R (revised in November 2012).

- Van Zandweghe, William, 2012. “Interpreting the Recent Decline in Labor Force Participation,” Federal Reserve Bank of Kansas City, Economic Review.

Footnotes

- It should be noted that the statement also stresses maintaining price stability and examining the efficacy and costs of the asset purchases (see the FOMC statement, December 12, 2012).Return

- See the transcript of Chairman Bernanke’s press conference <accessed May 1, 2013>.Return

- Over long periods, both the establishment survey, Current Employment Statistics (CES), and the household survey, Current Population Survey (CPS), give similar results. However, since the household survey data come from a smaller sample, monthly changes are a bit more volatile relative to the establishment survey results. For a more detailed discussion of these differences, see Schweitzer and Ransom (1999).Return

- Most recently confirmed in the March 2013 Summary of Economic Projections of the FOMC.Return

- For a less technical exposition of the basic model, see Tasci and Zaman (2010).Return

- Our estimation uses the “second” estimate for first-quarter GDP, based on BEA revisions released on May 30, 2013.Return

- In order to come up with a number for employment gains, we use the most recent publicly available population projection produced by the BLS. BLS population projections can be accessed on its website. The BLS projections were last updated in February 2012. We normalize these projections to 2013:Q1 levels in all the exercises below.Return

- We use the forecasts based on the latest release of the survey, dated May 10, 2013, which includes the next five quarters, through 2014:Q2.Return

- This outlook is similar to the median in the March Summary of Economic Projections of the FOMC.Return

- Aaronson et al. (2012), Van Zandweghe (2012), Erceg and Levine (2013), and Hotchkiss et al. (2013).Return

- CBO projections are based on the background paper, “CBO’s Labor Force Projections through 2021,” March 2011.Return

- For a detailed analysis of this issue in addition to a discussion of the implications for the natural rate, see Tasci (2012). For a less technical exposition, see Tasci and Zaman (2010).Return

- Mechanically, this requires a one-time increase in the random walk trend component of both of the flow rates.Return

Suggested Citation

Schweitzer, Mark E., and Murat Tasci. 2013. “What Constitutes Substantial Employment Gains in Today's Labor Market?” Federal Reserve Bank of Cleveland, Economic Commentary 2013-07. https://doi.org/10.26509/frbc-ec-201307

This work by Federal Reserve Bank of Cleveland is licensed under Creative Commons Attribution-NonCommercial 4.0 International