- Share

Understanding Post-Pandemic Surprises in Inflation and the Labor Market

Since the COVID-19 pandemic, the United States has experienced sharply rising then falling inflation alongside persistent labor market imbalances. This Economic Commentary interprets these macroeconomic dynamics, as represented by the Beveridge and Phillips curves, through the lens of a macroeconomic model. It uses the structure of the model to rationalize the debate about whether the US economy can expect a hard or soft landing. The model is surprised by the resiliency of the labor market as the US economy experienced disinflation. We suggest that the model’s limited ability to capture this resiliency is a feature of using a linear model to forecast the historically unprecedented movements seen after the pandemic among inflation, unemployment, and vacancy rates. We explain how, by adjusting the model to mimic congestion in a tight labor market and greater wage and price flexibility in a high-inflation environment, as during the post-pandemic period, the model can then capture what has been a path consistent with a soft landing.

The views authors express in Economic Commentary are theirs and not necessarily those of the Federal Reserve Bank of Cleveland or the Board of Governors of the Federal Reserve System. The series editor is Tasia Hane. This paper and its data are subject to revision; please visit clevelandfed.org for updates.

Introduction

The post-pandemic economic landscape has witnessed extreme fluctuations in vacancy and inflation rates. By mid-2022, two years after COVID-19 was declared a pandemic by the World Health Organization in March 2020, the United States saw inflation rise from its position close to the Federal Open Market Committee’s 2 percent target to about 6 percent, alongside the doubling of the ratio of vacancies to unemployment, a popular measure of labor market tightness, from close to 1 to close to 2. These movements marked a departure into uncharted economic territory, as they deviated dramatically from the historical relationship between vacancy and unemployment rates (the Beveridge curve) and between inflation and unemployment rates (a version of the Phillips curve). These deviations led to debate about the costs in terms of lost jobs of reducing inflation back to the FOMC’s 2 percent target. Contrary to predictions informed by historical regularities over the 1959–2019 period––with expectations of highly persistent shifts in the Beveridge curve and significant unemployment costs to curb vacancies and inflation––the period from mid-2022 through 2023 saw a swift decline in both vacancies and inflation with minimal upticks in unemployment rates.

In this Economic Commentary, we illustrate such predictions through a prominent economic debate in the third quarter of 2022, and we describe issues in forecasting during abnormal circumstances using a standard macroeconomic model estimated on historical data over 1959–2019 and detailed in Gelain and Lopez (2023). Models such as this one, a medium-scale dynamic stochastic general equilibrium (DSGE) model, typically simplify complex structural equations by linearly approximating them, a practical strategy that is appropriate to describe the economy in normal times. In this context, looking at the predictions of the Gelain¬¬–Lopez model (henceforth referred to as the “GL model”) in the third quarter of 2022, we can see that the model exemplifies why some economists felt a marked economic slowdown, or “hard landing,” was needed to bring inflation down. Yet, such concerns turned out to be overstated, an example of the dangers of relying on past data for projections in novel economic scenarios and on linear approximations amidst the extreme conditions of the post-pandemic US economy.

To address these modeling challenges, we propose certain ad hoc adjustments essential for maintaining the model’s linearized framework amid such volatility and helping us understand what is needed to bring about a soft landing. Specifically, we suggest that the model can explain the key variables over 2022–2023 by a combination of a faster recovery in how employees and employers find a match—matching efficiency—and a lower degree of nominal price and wage stickiness than in previous decades. Given the constraints that prevent us from solving the model through nonlinear methods, we posit that these modifications are a practical strategy to approximate what would be the actual outcomes of a more complex economic model, especially during this unique period.

Abnormal Economic Conditions

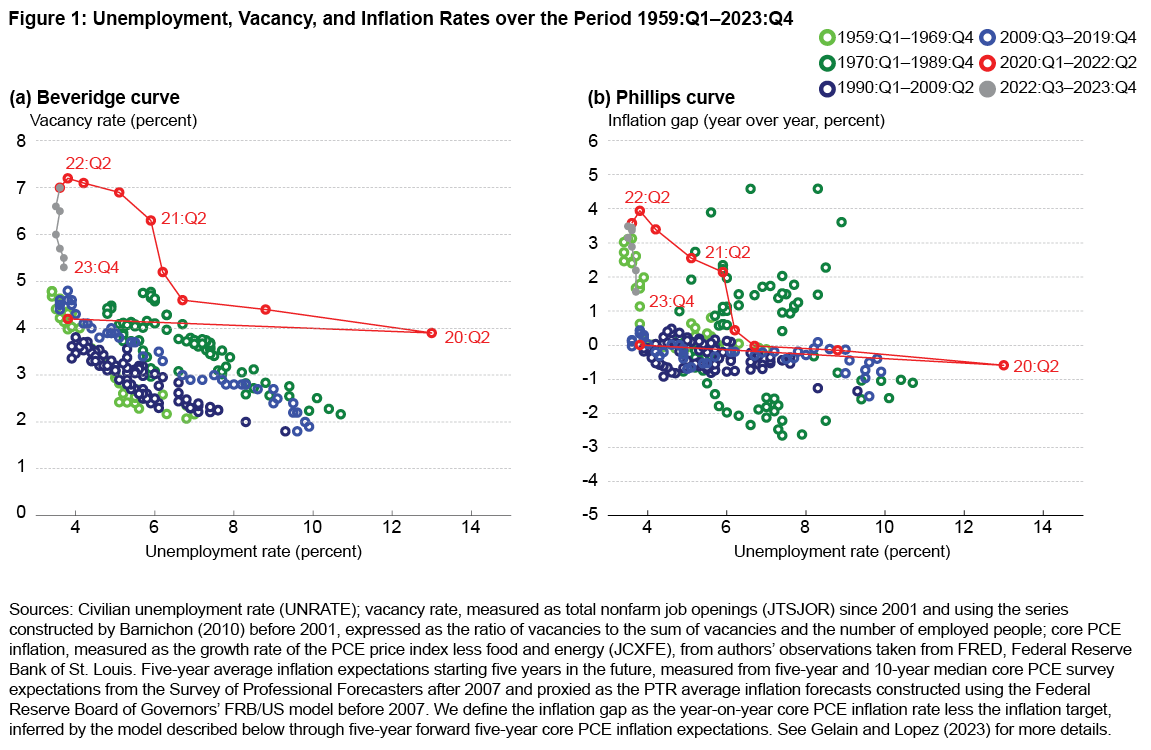

Figure 1 plots the quarterly data since 1959 for the unemployment and vacancy rates and for the unemployment rate and the inflation gap, defined as core inflation relative to the time-varying inflation target. This chart delineates the Beveridge curve through the relationship between unemployment and vacancy rates and a version of the Phillips curve through the relation between unemployment rates and the inflation gap.

Looking at the Beveridge curve, shown in panel (a), a consistently linear relation with periodic vertical shifts every decade or two is noticeable until the onset of the pandemic, marked by red dots. The pandemic significantly elevated the curve, propelling us into unprecedented territory in 2022, a scenario in which historical patterns of persistent vertical shifts proved to be of little guidance. Indeed, the data, plotted in grey, spanning from 2022:Q3 to 2023:Q4, the period during which monetary policymakers raised the federal funds rate to bring down inflation, show a swift decline in vacancy rates with little repercussion on real activity, as evidenced by the stable unemployment rates during this period.

Looking at the Phillips curve, shown in panel (b), we can likewise see a stable relationship from 1990 until the pandemic’s disruption, which initiated a noticeable upward shift starting in 2021, altering the stable relationship that existed in the previous two decades. Notable is also the flatness of this curve, a shape which is often interpreted as implying high costs in terms of unemployment to achieve a given reduction in inflation. However, the picture also illustrates a period of instability during the 1960s, 1970s, and 1980s, a reminder that the Phillips curve is not a structural relation in the model in the sense that inflation and unemployment rates do not always move together. Notably, the 1960s, represented by light green dots, show a vertical trajectory, a path that seemed to repeat from 2022:Q3 to 2023:Q4. However, this apparent similarity is deceptive; in the 1960s, the economy ascended this vertical path, contrasting with a descent in the recent period, indicating that past dynamics offer limited predictive content for the recent movements. Indeed, the data over the 2022:Q3–2023:Q4 period showed a swift fall in inflation rates with minimal increase in the unemployment rate.

Debate in the Outlook around Mid-2022

During the summer of 2022, at a pivotal moment depicted by the final red dots in Figure 1 as inflation and labor market tightness peaked, a prominent debate unfolded between Blanchard, Domash, and Summers (2022) on one side and Figura and Waller (2022) on the other. The discussion centered on the future trajectory along the Beveridge curve and whether the United States, as the FOMC raised interest rates in a sequence of rate hikes from March 2022, could disinflate without having unemployment increase. Despite the shared premise that a reduction in vacancy rates was necessary to decrease inflation—thus simplifying the debate to primarily examining the Beveridge curve’s implications—Blanchard et al. and Figura and Waller had very different outlooks.

Namely, Blanchard et al. (2022) argued that decreasing vacancy rates, something assumed necessary to reduce inflation, would necessitate a significant uptick in unemployment levels. They argued that achieving such a reduction in vacancies would require a strong improvement in matching efficiency, a factor beyond the FOMC’s influence and with no historical precedent to suggest its imminent realization, as shown in Figure 1. This perspective was echoed by Ball, Leigh, and Mishra (2022) in their work during the same period, work which included a pessimistic forecast predicated on the economy’s adjustment along the new, elevated Beveridge curve depicted in red in Figure 1, a shift presumed to persist after the pandemic.

Conversely, Figura and Waller (2022) projected a different outcome. Drawing on theoretical insights, they anticipated a pronounced nonlinearity in labor market dynamics resulting from congestion, characterized by high vacancy levels amid low unemployment, as predicted by standard models of the labor market based on a costly matching between unemployed workers and employers with vacancies. They predicted a swift downward adjustment of the Beveridge curve driven by a rapid, endogenous improvement in matching efficiency that would keep the unemployment rate near its current level, hence one that would imply only a small increase in the unemployment rate as inflation decreased.

The Perspective of a DSGE Model

We discussed above how it turned out that post-2022:Q3 developments validated the predictions by Figura and Waller (2022). In this context, we reinterpret the debate through the lens of a DSGE model and describe the outlook in 2022:Q3 of a general equilibrium model that describes both developments in the Beveridge curve and movements in the rest of the economy, including in the Phillips curve. We use a medium-scale New Keynesian model with search and matching frictions in the labor market, as detailed by Gelain and Lopez (2023). The GL model is estimated on US data spanning from 1959:Q1 to 2019:Q4 and aims to closely represent the empirical behavior of key economic variables, including output, consumption, investment, and real wages, alongside inflation, interest rates, unemployment, vacancy rates, and job-finding rates.1 Given its scale, the GL model’s solution is linearized; the solution is therefore appropriate to characterize the model’s implications around a neighborhood of the model’s steady state, but not necessarily after large movements that send the economy away from such a steady state, such as those implied by the pandemic.

Crucial to the debate are two aspects of the GL model. First is the inclusion of unexpected shifts in matching efficiency to capture changes in the ability of vacancies to turn into filled jobs. These shifts in matching efficiency capture historical changes in the Beveridge curve relationship between unemployment and vacancy rates. Second is the inclusion of costs for firms of adjusting nominal prices and wages that imply larger resource costs the larger the desired changes in the inflation rate. These adjustment costs are paramount in modeling the relationship between inflation and unemployment rates, hence the Phillips curve. It is important to note that, within the GL model, the Beveridge curve represents a structural relationship, while the Phillips curve’s connection between inflation and unemployment rates is indirect, mediated through real marginal costs, markup fluctuations, variations in the inflation target over time, and past inflation rates.

In the model’s estimation, the persistence of the exogenous matching efficiency is pinned down as part of the estimation procedure. Consistent with the evidence in Figure 1, we estimate a very high value for the persistence parameter of matching efficiency. Specifically, the shifts in the Beveridge curve seen in the sample are very persistent, with a half-life of approximately 20 years. Therefore, we confirm in estimation that the historical data indicate rare and persistent shifts in the Beveridge curve. Furthermore, the model’s estimation reveals a relatively high cost to adjusting nominal wages and prices and thus a high degree of nominal price and wage rigidities.

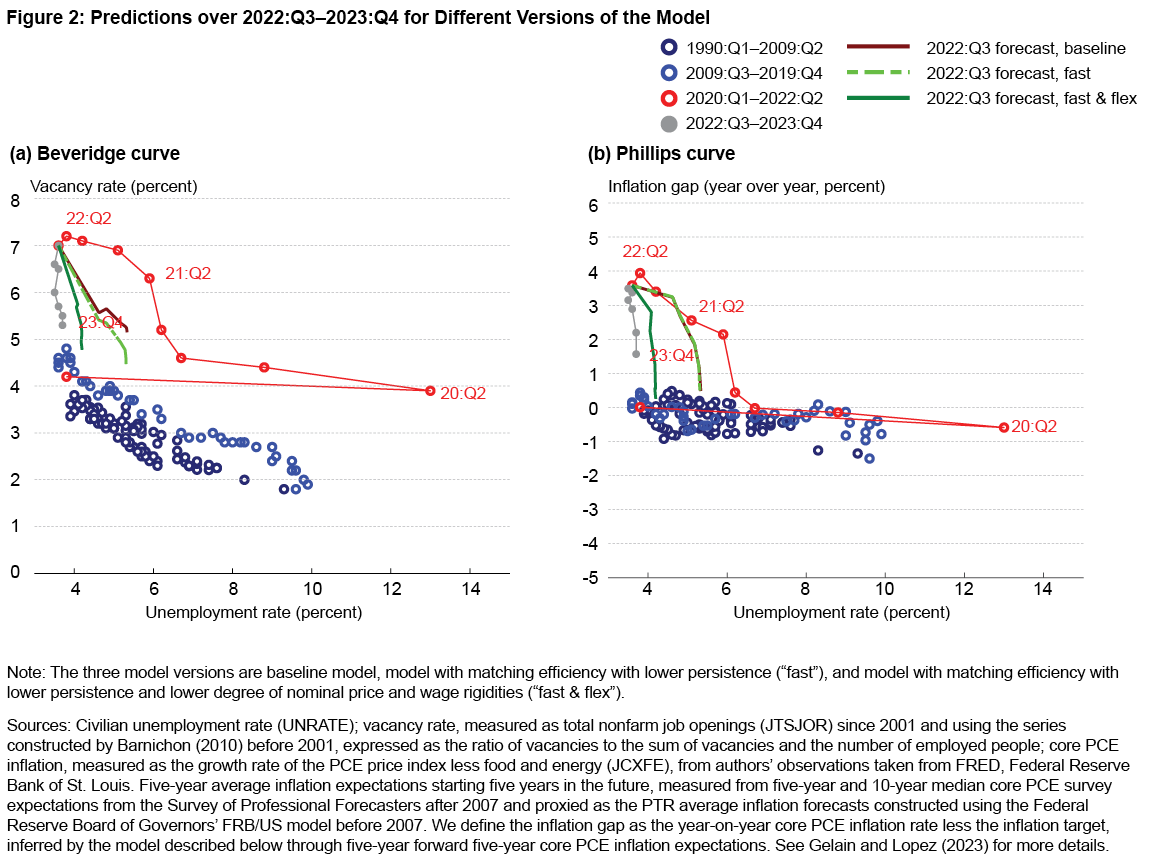

Unsurprisingly, when faced with the data available through 2022:Q3, the model interpreted the significant post-pandemic shifts in the labor market and inflation to be processes that are gradual and challenging to reverse quickly, according to the historical persistence inferred. As illustrated in Figure 2, using dark red to highlight the model’s forecasts as of 2022:Q3, the GL model projected a scenario in which reducing vacancy and inflation rates would be accompanied by a marked increase in unemployment. This projection anticipated that adjustments along both the Beveridge and Phillips curves would come with substantial economic costs, a forecast that therefore aligned with the perspective offered by Blanchard et al. (2022). The GL model perceived the Beveridge curve’s upward shift as a significant decrease in matching efficiency, a change expected to have lasting effects, consistent with historical patterns observed from the 1959–2019 data used in the model’s estimation.

However, the unfolding reality since 2022:Q3 presented a contrasting picture. With the advantage of hindsight, actual data indicated that the economy was capable of moving down the Beveridge and Phillips curves with a surprisingly minimal impact on unemployment. This divergence from the GL model’s predictions suggests a more dynamic labor market and pricing mechanism than previously estimated. We now turn to how we can explain these abnormal conditions through the structure of a DSGE model.

Adjustments to the DSGE Model

To make sense of the post-2022:Q3 period through the lens of our model, we introduce two modifications to the baseline GL model. These modifications are both aimed at better capturing the unexpected economic dynamics observed over the 2022–2023 period and helping us economically understand the surprising developments after 2022:Q3. The first modification incorporates into the GL model a lower persistence of matching efficiency after 2022:Q3. Namely, in Figure 2, we illustrate how the forecast as of 2022:Q3 changes if we let the half-life of the baseline matching efficiency process, represented by the light green dashed line, be two years rather than 20 years. By reducing the matching efficiency persistence, the model more accurately reflects the labor market’s resilience and its ability to recover without significantly elevating unemployment rates. Mechanically, a lower number of vacancies is now necessary to generate the level of matches required to keep the unemployment rate stable. This temporary change allows for a faster downward shift of the Beveridge curve. However, as shown by the light green dashed line in Figure 2, this adjustment has little impact on the Phillips curve dynamics, underscoring the need for an additional modification. This lack of impact suggests that along with a marked increase in matching efficiency, other structural changes have taken place in the economy, as well.

The second adjustment we introduce to the GL model is an exogenous increase in price and wage flexibility after 2022:Q3. Namely, in Figure 2, represented by the dark green solid line, we illustrate how the forecast as of 2022:Q3 changes if we reduce the adjustment cost of nominal prices and wages. This change is crucial for explaining how inflation was reduced from around 4 percentage points to around 1.5 percentage points above the target with minimal impact on the real economy. As shown in Figure 2, by incorporating lower nominal stickiness, the model features a decrease in inflation alongside stable unemployment rates, more closely aligning with the observed data. This lower stickiness is important to generate realistic dynamics for both curves, but it is especially significant for the Phillips curve, enabling it to more accurately reflect the downward vertical shift observed in the data. The inclusion of both fixes––fast improvements to matching efficiency and increased price and wage flexibility––results in a DSGE model that better matches the post-pandemic recovery.

These adjustments, while useful practical fixes, are simplifications meant to retain the model’s linearized solution, and thus its tractability, in the face of complex phenomena. They represent an exogenous approach to capturing what we think of ultimately as endogenous dynamics. We have two examples in mind. First, a more accurate solution method would capture the theoretical nonlinearity in the Beveridge curve that implies fast endogenous improvements in matching efficiency in a congested labor market in which a very high number of vacancies chase a limited number of unemployed workers, as emphasized by Figura and Waller (2022). Second, a richer price setting theory would imply endogenously lower costs to nominal price and wage adjustments in a high-inflation environment (capturing a story that goes back at least to Ball, Mankiw, and Romer, 1988).2 Thus, while our modifications enhance the model’s explanatory power, they should be viewed as approximations that capture the observed economic conditions, rather than precise mechanisms, and that are not expected to persist as economic conditions normalize.

For economists and policymakers, these model adjustments offer valuable insights into capturing and responding to unusual economic conditions. By understanding how matching efficiency and nominal stickiness evolve in abnormal states of the economy, decisionmakers can better anticipate labor market responses and inflationary pressures in similar future scenarios. These adjustments to medium-scale linearized New Keynesian models underscore the need to consider flexible responses in economic modeling and their implications for policy formulation, especially when faced with data that deviate from traditional patterns, such as those observed over 2022–2023.

Conclusion

The economic landscape of high inflation and labor market imbalances as of 2022:Q3 presented unique challenges and anomalies, particularly in the labor market and inflation dynamics. Standard linearized medium-scale DSGE models, given that they aim to capture historical relationships, face a challenge when capturing these data. To address these challenges, we propose some ad hoc adjustments to such models, including incorporating lower persistence in matching efficiency and increased flexibility in price and wage adjustments to preserve their linear structure and thus their tractability. These modifications enhance the model’s alignment with observed economic data, and they help us understand how and why the disinflation of 2023 was not accompanied by higher unemployment rates.

This analysis underscores the need for models and their users to be flexible to respond to unprecedented economic conditions. Despite their advantage in modeling many economic variables jointly within a structural framework, the post-2022:Q3 period illustrates some of the pitfalls of medium-scale linearized DSGE models after large shifts in economic fundamentals, necessitating adjustments to maintain their relevance. The ad hoc approach described above strikes a balance between complexity and tractability. It serves as a proxy for capturing the nonlinearities inherent to the Beveridge curve and the varying stickiness of nominal prices and wages as inflation levels change.

References

- Ball, Laurence M., Daniel Leigh, and Prachi Mishra. 2022. “Understanding US Inflation during the COVID-19 Era.” Brookings Papers on Economic Activity 2022 (Fall): 1–54. https://www.brookings.edu/articles/understanding-u-s-inflation-during-the-covid-era/.

- Ball, Laurence M., N. Gregory Mankiw, and David Romer. 1988. “The New Keynesian Economics and the Output-Inflation Trade-Off.” Brookings Papers on Economic Activity 1988 (1): 1–82. https://doi.org/10.2307/2534424.

- Blanchard, Olivier J., Alex Domash, and Lawrence H. Summers. 2022. “Bad News for the Fed from the Beveridge Space.” Policy Brief PB22-7. Peterson Institute for International Economics. https://www.piie.com/publications/policy-briefs/bad-news-fed-beveridge-space.

- Figura, Andrew, and Christopher J. Waller. 2022. “What Does the Beveridge Curve Tell Us about the Likelihood of a Soft Landing?” FEDS Notes. Board of Governors of the Federal Reserve System. https://doi.org/10.17016/2380-7172.3190.

- Gelain, Paolo, and Pierlauro Lopez. 2023. “A DSGE Model Including Trend Information and Regime Switching at the ZLB.” Working paper 23-35. Federal Reserve Bank of Cleveland. https://doi.org/10.26509/frbc-wp-202335.

- L’Huillier, Jean-Paul, and Raphael S. Schoenle. 2020. “Raising the Inflation Target: How Much Extra Room Does It Really Give?” Working paper 20-16. Federal Reserve Bank of Cleveland. https://doi.org/10.26509/frbc-wp-202016.

- Waller, Christopher J. 2023. “The Unstable Phillips Curve.” Speech. Macroeconomics and Monetary Policy, a Conference Sponsored by the Federal Reserve Bank of San Francisco. Board of Governors of the Federal Reserve System. https://www.federalreserve.gov/newsevents/speech/waller20230331a.htm.

Endnotes

- Less important for our current purposes, the Gelain–Lopez model (2023) also incorporates low-frequency components that capture trends in growth, inflation, interest, and unemployment rates and a strategy to capture how the model’s dynamics change when the zero lower bound on the interest rate set by the central bank is binding. Return to 1

- See also L’Huillier and Schoenle (2022) and Waller (2023) for discussions on recent microevidence indicating a higher frequency of price adjustments during the post-pandemic recovery. Return to 2

Suggested Citation

Gelain, Paolo, and Pierlauro Lopez. 2024. “Understanding Post-Pandemic Surprises in Inflation and the Labor Market.” Federal Reserve Bank of Cleveland, Economic Commentary 2024-11. https://doi.org/10.26509/frbc-ec-202411

This work by Federal Reserve Bank of Cleveland is licensed under Creative Commons Attribution-NonCommercial 4.0 International