- Share

Understanding Which Prices Affect Inflation Expectations

The views authors express in Economic Commentary are theirs and not necessarily those of the Federal Reserve Bank of Cleveland or the Board of Governors of the Federal Reserve System. The series editor is Tasia Hane. This paper and its data are subject to revision; please visit clevelandfed.org for updates.

Introduction

Inflation expectations are key components in canonical macroeconomic models. They play an important role in prices and output formation, influencing firm and consumer decisions. In recent years, policymakers have focused on measuring and eventually influencing inflation expectations to stabilize output and prices and to provide additional stimulus to an economy when there are constraints to conventional monetary and fiscal tools (Coibion et al., 2020a). In recent months, inflation has received significant attention as inflationary pressures have been more persistent than initially believed. This attention on the price dynamics has led to a natural adjustment of consumers’ inflation expectations and has been reflected in recent survey evidence.

While inflation expectations are consistently measured in surveys, factors that drive differences in expectations across consumers and different subgroups remain poorly understood. In this Economic Commentary, we focus on understanding differences in the implicit weights assigned to specific price changes by consumers and professional forecasters when determining their inflation expectations. The fact that typical consumers may prioritize different basket components relative to those prioritized by professional forecasters generates a rift in inflation expectations between the two groups. Understanding the prevalence and magnitudes of these wedges can help inform policies that aim to anchor consumers’ expectations more generally.

Our analysis is predicated on using standard model selection techniques to understand what basket components consumers and professional forecasters prioritize in forming expectations. The implicit priority weights these two groups place on different baskets of goods shed light onto what factors drive wedges between their inflation expectations. We then assess the differences in the relationship between well-established consumer price index (CPI) weights and our estimated group priority weights. We use a similar approach to Berge (2018), but we focus on only prices to obtain implicit weights for consumers and professional forecasters. We find striking differences between the factors that the two groups prioritize. While professional forecasters’ expectations appear to weight different categories of prices approximately in line with the weights of those categories in the CPI, consumers seem to look to specific prices related to food and vehicles, among others. These differences generate sharp wedges between consumer and professional forecaster expectations.

These results have important implications. One interpretation of our findings is that consumers pay significant attention to a subset of items rather than weighting them in line with their spending, the latter method being more consistent with the weights in the CPI. This discrepancy is highly relevant today as the onset of the COVID-19 pandemic induced idiosyncratic increases in price levels for different goods, generating potential rifts in how consumers adjusted their inflation expectations relative to how professional forecasters adjusted theirs. For example, at the beginning of the pandemic, we saw abnormal increases in food prices and car prices. Our findings suggest that these increases disproportionally affected consumers’ inflation expectations while slightly affecting professional forecasters’ measures. Recent empirical evidence shows that consumers’ inflation expectations affect their economic decisions, so changes in those expectations have the potential to affect aggregate economic variables such as consumption. Our findings show that consumers may pay disproportional attention to some prices; if so, then communication about the nature of those specific price changes can potentially help to avoid systematic increases in inflation expectations that might result in systematically higher inflation outcomes.

Methodology

Despite the policy importance of inflation expectations, there is no consensus on the best measure of inflation expectations or on their relevance. There are generally two groups of inflation expectation measures. One relies on professional forecasters, who are asked to predict inflation at various horizons. Professional forecast expectations, made by attentive and informed agents, are typically close to actual inflation. This makes these inflation expectations very useful for forecasting purposes (Verbrugge and Zaman, 2021). The second is to ask consumers or firm managers about their inflation expectations.1 These measures are generally higher than the actual inflation value, and there is a high level of disagreement among respondents (Afrouzi et al., 2015; Binder, 2017; Candia et al., 2021); thus, they don’t predict inflation well, especially in countries with low and stable inflation. Nevertheless, there is mounting evidence demonstrating that consumer- and firm-level expectations rationalize macroeconomic data, indicating they are meaningful to understanding microeconomic decisions (Coibion and Gorodnichenko, 2015; Binder, 2015). In addition, there is causal evidence showing that firm-level decisions are indeed influenced by their inflation expectations (Coibion et al., 2018, and Coibion et al., 2020b).

While there is evidence of the importance of inflation expectations, few studies seek to understand what determines inflation expectations. Berge (2018) is one notable exception in looking at different variables that predict inflation expectations. Other papers have focused on specific prices that consumers see when setting their inflation expectations (Cavallo et al., 2017; Coibion and Gorodnichenko, 2015; Wong, 2015). We focus on examining the prices that could influence inflation expectations. Our methodology is used to measure whether current price changes in certain goods affect consumer predictions of inflation. For example, let us assume that consumers purchase only food and pay rent. Then, when forming expectations, consumers would likely put some weight on the price changes that they see from these components.2 If food prices increase by 5 percent and rent increases by zero percent over one year, consumers might use that information to form expectations. This is relevant because in this scenario inflation is a weighted average of these two components, depending on how much consumers spend on these goods on average. Generally speaking, if half of one’s average spending goes to food and the other half goes to rent, inflation in this example would be 2.5 percent. But if consumers pay more attention to food prices, then their expectations could be higher as they project a higher inflation from the current level of food inflation. We test if this is the case, allowing the possibility that none of these components in the example are relevant.

It is straightforward to estimate implicit weights in the case with two components. In practice, however, many factors enter consumers’ inflation expectations, making calculating inflation expectations a higher-dimensional problem with many components that change similarly. For example, the price index of fruits and vegetables could have a similar trajectory compared with the indices of other foods such as cereals and bakery products. Although inflation expectations may depend on many different components, consumers are likely to form expectations using a relatively sparse list of components, those most salient to their day-to-day expenditures (D’Acunto et al., 2021). Therefore, our empirical goal is twofold: First, we aim to identify one set of components that is most predictive of expectations for consumers and one for professional forecasters; and, second, we aim to estimate the relative importance of those components to each of these groups.

In the parlance of the statistics literature, our problem amounts to variable selection, or the problem of selecting among similar components. While consumers may be considering a multitude of potentially similar components when forming inflation expectations, there is a subset that optimizes predictive power. To this end, we use the popular statistical procedure known as “least absolute shrinkage and selection operator” (LASSO) to determine our statistical model for explaining inflation expectations.

LASSO selects the most important components, discarding the components that add less to the forecast. With this technique, the model can select the most predictive components among many that might move similarly.3

Data

We use three sources of data. First, we use the University of Michigan Survey of Consumer Expectations (MSC) to obtain consumers’ inflation expectations. The University of Michigan has released a monthly survey of consumers’ expectations since 1978. We make use of its quarterly data through 2020:Q2 over various demographic groups: age, geographic region, gender, income, and education level. We use its question that asks consumers what percent they expect prices to change during the next year. The second is the Survey of Professional Forecasters (SPF), which is a quarterly survey going back to 1968. For this Commentary, we consider the forecast for CPI inflation over the next year (that is, the next four quarters) using the median expectations for each group. Finally, the Bureau of Labor Statistics (BLS) releases measures of CPI inflation for categories at various levels of aggregation. For our purposes, we consider 20 different categories and the combined measure for all items.4 These categories do not overlap, meaning that no category is contained in another used in this exercise. The categories are consistent across the sample and represent most of the CPI. This setup allows us to interpret the regression coefficients in our exercise as implicit weights that consumers or professional forecasters place on the different components. We download the monthly levels across the sample period and calculate the 12-month percent change, using the final month of the quarter in the analysis. All categories are available for the entire sample.

Results

We run LASSO over three different timeframes on consumers, professionals, and the CPI itself using the simple specification below.

In the specification, the dependent variable is median consumer inflation expectations, median professional forecasters’ inflation expectations, or the CPI for all items in quarter t. The time frames are the entire sample (1978–2020:Q2), after 1989, and after 1999. Furthermore, we split up consumers into five different demographic categories based on gender, geographic region, income, age, and education level. Then, we run LASSO on the different consumer demographic categories across the three different timeframes. Each time LASSO is run, it outputs coefficients for each of the 20 CPI categories of interest.5 The larger the relative size of a coefficient, the more impact it has on the dependent variable: consumer inflation expectations, professional forecaster inflation expectations, and the CPI itself.

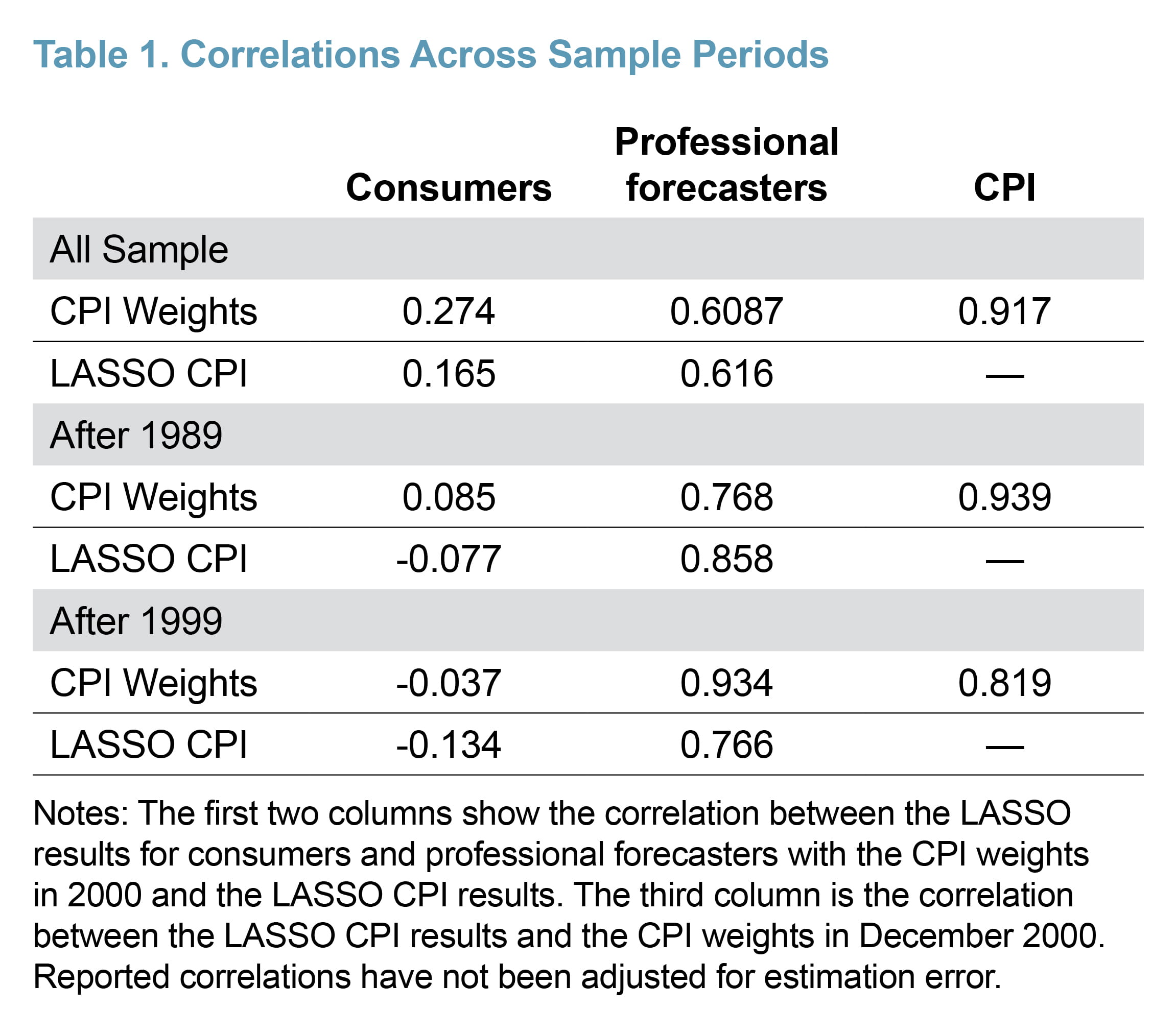

We start by showing how the coefficients of LASSO correlate with the actual CPI weights. We use the actual CPI weights from 20006 as a midpoint, and we run LASSO for the whole sample, from 1990:Q1–2020:Q2, and from 2000:Q1–2020:Q2. Figure 1 plots the coefficient for each component found in this exercise and compares it with its actual weight in the CPI.

The scatter plots in Figure 1 plot the CPI weights of the 20 categories in the analysis on the y-axis and the coefficients from the LASSO analysis on the x-axis. The dotted and dashed lines are linear fits of the data for each respective group. The solid line is the 45-degree line, which is where the data points should be if their LASSO coefficients are exactly equal to their CPI weights. We can see a high correlation between the LASSO estimates for the CPI and the actual weights for the CPI, one which validates our exercise. We also see a high correlation between the SPF and the LASSO CPI lines in all the samples. This similarity is showing that professional forecasters seem to anticipate that changes in prices will be similar to current changes in price components and are weighting them in a similar way as the weights in the CPI. In the case of consumers, we see a very low correlation, one that has become flatter over time.

Table 1 shows the correlation between the 20 coefficients of the CPI categories from the LASSO results for consumers, professional forecasters, and the CPI in each column and the actual CPI weights. We run LASSO over the CPI as a way to validate our methodology. The weights used for the actual CPI are fixed as the December 2000 weights but are generally stable, making the midpoint of our entire sample a reasonable selection. We get a high correlation between the LASSO estimates and the actual weights used for the construction of the CPI, a circumstance which means that our regression approach can obtain weights for the CPI that are close to the actual weights even if we are allowing for some categories to drop out of the model.

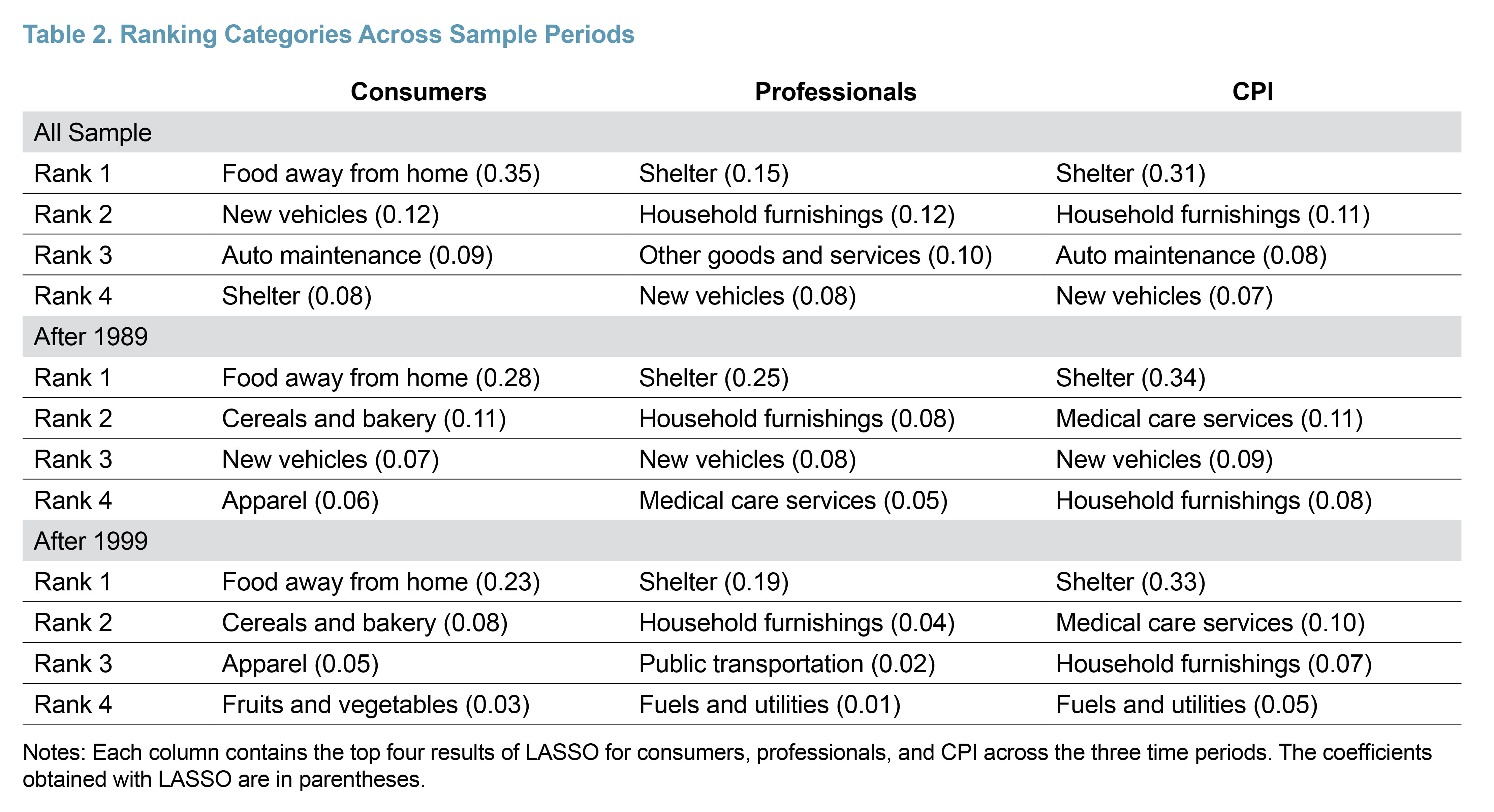

Table 1 also shows the correlation between the LASSO results for consumers and professional forecasters and the LASSO results for the CPI. We do this using the entirety of the sample (1978 through 2020:Q2), after 1989, and after 1999. Professional forecaster coefficients are strongly correlated with both, meaning the weights given to categories that are important for the professional forecasters are similar to the CPI LASSO results and the actual CPI weights. The correlation between the professional forecasters’ coefficients and both the CPI weights and the LASSO CPI has increased as we restrict the sample, telling us that as time has gone on and as inflation became generally more stable, the expectations of professional forecasters have been influenced largely in line with the factors affecting the CPI. Consumer weights are by far the least correlated with the CPI weights. The results for consumers have also become less correlated with both the CPI weights and the CPI LASSO results as we restrict the sample, indicating that as time has gone on, the items that have been most important for explaining variation in consumers’ inflation expectations have tended to diverge from the items driving movements in the CPI. This finding may help to explain why some studies have found that consumers are less likely to accurately predict inflation in the short run. It is important to highlight that both professional forecasters and consumers are asked to predict future inflation, not current inflation. Current prices can influence these expectations because they project a persistent change for these prices. To see what components are most important for each measure, we rank the top four categories in Table 2.

Looking at the results for consumers, food away from home is the most important category across the sample. This fact suggests consumers’ inflation expectations are most affected by how the price of food away from home is moving. Professional forecasters’ results show that shelter and household furnishings are the top two indicative categories throughout the entire sample. Finally, for the CPI itself, shelter and household furnishings are consistently in the top four. While shelter shows up as the fourth-highest weighted for consumers in the entire sample, it only has a magnitude of 8.49 percent, whereas it is 15.2 percent for professional forecasters and 31.0 percent for the CPI. These variances are what lead to the drastic differences in the correlations seen in Table 1. The top four categories do change over time for all three; for example, new vehicles slowly drops out of the top four in the consumer column as we restrict the sample period to the more recent period. For the CPI, medical care services has increased in relevance.

These tables help us understand the CPI categories that best predict current expectations of short-term inflation. On the one hand, the results could imply that consumers are more attentive to prices of certain items or services. For example, even though consumers’ average expenditure share on housing is roughly one-third, they face new prices in this category far less often than they face price changes at restaurants they visit frequently. In the same vein, individual consumers rarely purchase a new vehicle compared with the frequency of regular expenditures on other consumption goods, but they still seem to place substantial weight on new vehicles’ prices. This latter observation points to systematic differences in both consumers’ perceptions of relevant goods and the markets of goods in which they frequently participate. Regardless of the explanation that drives these differences, the results can inform policymakers regarding how to communicate with consumers to nudge their inflation expectations to better fit what is happening. They can directly address changes in prices of food away from home, new vehicles, apparel, and shelter to assuage any worries.

Figure 2 plots the LASSO results for some of the top CPI categories for various demographic groups from the MSC using the entire sample. The higher the value of the LASSO coefficient, the more the category was deemed important by LASSO. Food away from home is the top category across all demographics. Auto maintenance is the second highest category for high school graduates and people with some college experience and for the second income quartile, and it is a close third for the third income quartile. Education follows a similar pattern to income, and that makes sense given their strong correlation.

Figure 2 also shows us that for practically every demographic, there is one category that dominates the LASSO results, food away from home. New vehicles, shelter, and auto maintenance are also relatively consistently close behind, but the coefficients begin to fall very close to zero after that.

We believe this exercise provides useful insights into some of the factors driving inflation expectations. If inflation expectations are mostly impacted by the price fluctuations in a few categories of goods, we can use those measures to understand where consumers’ expectations might be going. One of these measures, new vehicles, has especially increased during the COVID-19 pandemic, mostly because of the microchip shortage.7 This category’s being the second most important for almost all demographics could explain why consumer inflation expectations have increased for one-year-ahead inflation but not as much for three-year-ahead inflation.8

Predictions

To test our model’s ability to predict inflation expectations, we look at the results from the 2000:Q1–2020:Q2 period. Using these LASSO results for consumers and professional forecasters and the actual values of these CPI categories going back to 2010:Q1, we can calculate the inflation expectations based on the LASSO model. We then compare these predicted inflation expectations to the actual inflation expectations during this time. Using the actual CPI category inflation rates through 2021:Q3, beyond the modeling period, we use our LASSO regression coefficients to predict how inflation expectations would have evolved if the relationships prior to the COVID-19 pandemic had remained constant. The plots of the model predictions from 2010:Q1–2021:Q3, actual survey results, and actual CPI inflation can be seen below in Figure 3.

The LASSO predictions for both consumers and professional forecasters are close to actual inflation expectations throughout the modeling period. The model also does a fairly good job at forecasting how inflation expectations evolved after the start of the pandemic based on the movements in the various inflation components, tending to underpredict inflation expectations for consumers and slightly overpredict for professional forecasters, with the biggest misses coming from underpredicting consumers’ inflation expectations in late 2021. This large discrepancy may be due to unforeseen shocks that change the implicit weights consumers place on various goods. An example of an unforeseen shock is the large amount of news coverage on inflation. This phenomenon is less likely to impact professional forecasters because they focus less on media coverage and more on data, and, as such, we see more stable predictive patterns for professional forecasters during the pandemic.

Conclusion

We provide evidence that consumers and professional forecasters have historically appeared to place different weights on different inflation components. Consumers’ inflation expectations have tended to move with inflation rates in food, apparel, and new vehicles, items that may be particularly salient to most household budgets. By contrast, the inflation expectations of professional forecasters have tended to move with inflation in shelter and household furnishings, categories that have tended also to be relatively more important in the CPI. We see that during the pandemic, our LASSO results, which were limited to a small list of salient inflation components, were able to pick up some of the increase in consumers’ expectations.

These results can have important implications today. At the beginning of the COVID-19 pandemic, while inflation was low, we saw an increase in inflation expectations. This could be a result of food prices that were growing at a faster rate than other prices because of supply chain restrictions. Later, we saw increases in car prices and other components that pushed inflation upward. Consumers seem to place a lot of weight on these goods when forming their expectations.

The difference in weights may have relevant policy implications. While professional forecasters may be little fazed by large increases in some components of inflation, consumers might be highly weighting these categories and raising their inflation expectations, thereby affecting their economic decisions and thus future inflation. Communicating with the public about why prices are changing in certain key sectors may help avoid any long-lasting changes in consumers’ inflation expectations.

Endnotes

- For example, see a new measure of indirect consumer inflation expectations in Hajdini et al. (2022). Return to 1

- Coibion et al. (2022) find that consumers update their inflation expectations after having information on past inflation. Return to 2

- LASSO balances the bias-variance tradeoff problem inherent in most statistical models by penalizing component weights that do not add much predictive power to a model, effectively setting many implicit weights to zero. As mentioned earlier, this sparsity assumption is plausible as consumers likely form expectations using price changes among their most salient components. Return to 3

- The categories we consider are apparel; cereals and bakery; meat, poultry, fish, and eggs; fruits and vegetables; nonalcoholic beverages and beverage materials; other food at home; alcoholic beverages; other goods and services; shelter; fuels and utilities; household furnishings and operations; medical care commodities; medical care services; dairy and related products; food away from home; new vehicles; motor fuel; motor vehicle maintenance and repair; motor vehicle insurance; and public transport. Return to 4

- With this approach, we can get some negative weights, a situation which means that the residualized correlation between inflation expectations and price changes is negative. There could be many reasons to explain a negative value, especially considering that we are using realized prices. For simplicity, in this Commentary we use these weights, but further investigation could be done in order to consider the adequate weights and potential restrictions under more specific structural assumptions. Return to 5

- We selected December 2000, but the weights are very stable over the sample. After 2000, some new goods were added. CPI weights can be found here: https://www.bls.gov/cpi/tables/relative-importance/home.htm. Return to 6

- See Krolikowski and Naggert (2021) and Boudette (2021). Return to 7

- https://www.newyorkfed.org/microeconomics/sce#/ Return to 8

References

- Afrouzi, Hassan, Olivier Coibion, Yuriy Gorodnichenko, and Saten Kumar. 2015. “Inflation Targeting Does Not Anchor Inflation Expectations: Evidence from Firms in New Zealand.” Brookings Papers on Economic Activity 2015 (2): 151–208. https://doi.org/10.1353/eca.2015.0007.

- Berge, Travis J. 2018 “Understanding Survey-based Inflation Expectations.” International Journal of Forecasting 34: 788–801. https://doi.org/10.1016/j.ijforecast.2018.07.003.

- Binder, Carola Conces. 2015. “Whose Expectations Augment the Phillips Curve?” Economics Letters 136 (November): 35–38. https://doi.org/10.1016/j.econlet.2015.08.013.

- Binder, Carola Conces. 2017. “Measuring Uncertainty Based on Rounding: New Method and Application to Inflation Expectations.” Journal of Monetary Economics 90 (October): 1–12. https://doi.org/10.1016/j.jmoneco.2017.06.001.

- Boudette, Neal E. 2021. “‘The Market Is Insane’: Cars Are Sold Even Before They Hit the Lot.” The New York Times, July 15, 2021, sec. Business. https://www.nytimes.com/2021/07/15/business/car-sales-chip-shortage.html.

- Candia, Bernardo, Olivier Coibion, and Yuriy Gorodnichenko. 2021. “The Inflation Expectations of US Firms: Evidence from a New Survey.” Working paper 28836. National Bureau of Economic Research. https://doi.org/10.3386/w28836.

- Cavallo, Alberto, Guillermo Cruces, and Ricardo Perez-Truglia. 2017. “Inflation Expectations, Learning, and Supermarket Prices: Evidence from Survey Experiments.” American Economic Journal: Macroeconomics 9 (3): 1–35. https://doi.org/10.1257/mac.20150147.

- Coibion, Olivier, and Yuriy Gorodnichenko. 2015. “Is the Phillips Curve Alive and Well after All? Inflation Expectations and the Missing Disinflation.” American Economic Journal: Macroeconomics 7 (1): 197–232. https://doi.org/10.1257/mac.20130306.

- Coibion, Olivier, Yuriy Gorodnichenko, and Saten Kumar. 2018. “How Do Firms Form Their Expectations? New Survey Evidence.” American Economic Review 108 (9): 2671–2713. https://doi.org/10.1257/aer.20151299.

- Coibion, Olivier, Yuriy Gorodnichenko, Saten Kumar, and Mathieu Pedemonte. 2020a. “Inflation Expectations as a Policy Tool?” Journal of International Economics 124 (May): 103297. https://doi.org/10.1016/j.jinteco.2020.103297.

- Coibion, Olivier, Yuriy Gorodnichenko, and Tiziano Ropele. 2020b. “Inflation Expectations and Firm Decisions: New Causal Evidence.” Quarterly Journal of Economics, vol 135 (1). February: 165–219. https://doi.org/10.1093/qje/qjz029.

- Coibion, Olivier, Yuriy Gorodnichenko, and Michael Weber. 2022. “Monetary Policy Communications and Their Effects on Household Inflation Expectations.” Journal of Political Economy forthcoming (January). https://doi.org/10.1086/718982.

- D’Acunto, Francesco, Ulrike Malmendier, Juan Ospina, and Michael Weber. 2021. “Exposure to Grocery Prices and Inflation Expectations.” Journal of Political Economy 129 (5): 1615–39. https://doi.org/10.1086/713192.

- Hajdini, Ina, Edward S. Knotek II, Mathieu Pedemonte, Robert Rich, John Leer, and Raphael Schoenle. 2022. “Indirect Consumer Inflation Expectations.” Economic Commentary, no. 2022–03 (March). https://doi.org/10.26509/frbc-ec-202203.

- Krolikowski, Pawel, and Kristoph Naggert. 2021. “Semiconductor Shortages and Vehicle Production and Prices.” Economic Commentary, no. 2021–17 (July). https://doi.org/10.26509/frbc-ec-202117.

- US Bureau of Labor Statistics. 2022. “Consumer Price Index: Relative Importance and Weight Information for the Consumer Price Indexes.” February 28, 2022. https://www.bls.gov/cpi/tables/relative-importance/home.htm.

- Verbrugge, Randal J., and Saeed Zaman. 2021. “Whose Inflation Expectations Best Predict Inflation?” Economic Commentary, no. 2021–19 (October). https://doi.org/10.26509/frbc-ec-202119.

- Wong, Benjamin. 2015. “Do Inflation Expectations Propagate the Inflationary Impact of Real Oil Price Shocks?: Evidence from the Michigan Survey.” Journal of Money, Credit and Banking 47 (8): 1673–89. https://doi.org/10.1111/jmcb.12288.

Suggested Citation

Campos, Chris, Michael McMain, and Mathieu Pedemonte. 2022. “Understanding Which Prices Affect Inflation Expectations.” Federal Reserve Bank of Cleveland, Economic Commentary 2022-06. https://doi.org/10.26509/frbc-ec-202206

This work by Federal Reserve Bank of Cleveland is licensed under Creative Commons Attribution-NonCommercial 4.0 International