- Share

The Federal Funds Market since the Financial Crisis

Before the financial crisis, the federal funds market was a market in which domestic commercial banks with excess reserves would lend funds overnight to other commercial banks with temporary shortfalls in liquidity. What has happened to this market since the financial crisis? Though the banking system has been awash in reserves and the federal funds rate has been near zero, the market has continued to operate, but it has changed. Different institutions now participate. Government-sponsored enterprises such as the Federal Home Loan Banks loan funds, and foreign commercial banks borrow.

The views authors express in Economic Commentary are theirs and not necessarily those of the Federal Reserve Bank of Cleveland or the Board of Governors of the Federal Reserve System. The series editor is Tasia Hane. This paper and its data are subject to revision; please visit clevelandfed.org for updates.

Although monetary policy has focused on setting an appropriate level for the federal funds rate since well before the financial crisis, the mechanics since the crisis have changed. In response to the crisis, several new policies were enacted that altered the structure of the federal funds market in profound ways. On the borrowing side, the Fed’s large-scale asset purchases (LSAPs) flooded the banking system with liquidity and made it less necessary to borrow. In addition, the Federal Deposit Insurance Corporation (FDIC) introduced new capital requirements that increased the cost of wholesale funding for domestic financial institutions. On the lending side, the Federal Reserve now pays some financial institutions interest on their excess reserves (IOER). When institutions have access to this low-risk alternative, they have less incentive to lend in the federal funds market.

In this environment, the institutions willing to lend in the federal funds market are institutions whose reserve accounts at the Fed are not interest-bearing. These include government-sponsored entities (GSEs) such as the Federal Home Loan Banks (FHLBs). The institutions willing to borrow are institutions that do not face the FDIC’s new capital requirements and do have interest-bearing accounts with the Fed. These include many foreign banks. As such, the federal funds market has evolved into a market in which the FHLBs lend to foreign banks, which then arbitrage the difference between the federal funds rate and the rate on IOER.

This Commentary describes the evolution of the federal funds market since the crisis. While research is ongoing about the effect these shifts in the market will have on the Fed’s ability to conduct monetary policy, events of the past decade highlight the large effect that small interventions like FDIC capital requirements can have on the structure of the financial system.

The Federal Funds Market before the Crisis

Before the financial crisis, the federal funds market was an interbank market in which the largest players on both the demand and supply sides were domestic commercial banks, and in which rates were set bilaterally between the lending and borrowing banks. The main drivers of activity in this market were daily idiosyncratic liquidity shocks, along with the need to fulfill reserve requirements. Rates were set based on the quantity of funds available in the market and the perceived risk of the borrower.

Although the Federal Open Market Committee (FOMC) sets a target for the federal funds rate, the actual funds rate is determined in the market, with the “effective” rate being the weighted average of all the overnight lending transactions in the federal funds market. When the effective rate moved too far from the Fed’s target before the financial crisis, the FOMC adjusted it through open market operations. For example, if the Fed wanted to raise the effective rate, it would sell securities to banks in the open market. Buying those securities reduced the funds banks had available for lending in the federal funds market and drove the interest rate up. The Fed’s portfolio of securities consisted mainly of treasury bills, generally of short maturity, and its balance sheet was small.

Transition

The financial crisis—and the policies enacted to deal with its consequences—led to great change in the federal funds market. Three developments caused most of the change: the Fed’s balance sheet expanded in size, new banking regulations were enacted, and the Fed began paying interest to banks on funds they held in their reserve accounts at the Fed.

The Vast Increase in Cash Reserves

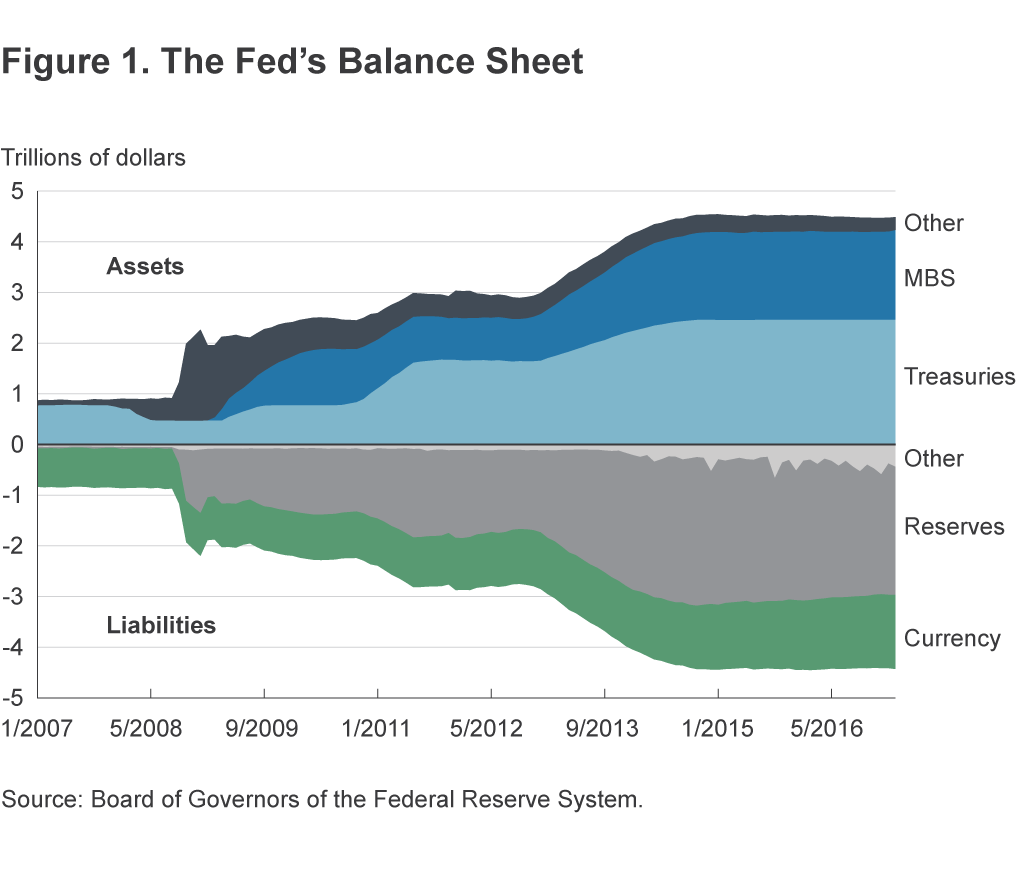

Between January 2008 and the end of the financial crisis in June 2009, the Federal Reserve’s balance sheet increased by 130 percent, swelling to $2.1 trillion (figure 1). Since then, the balance sheet has increased by an additional $2.3 trillion and now stands at $4.4 trillion. It consists of $2.46 trillion in treasuries, $26.81 billion in agency debt, and $1.76 trillion in mortgage-backed securities.

The reason for the rapid increase is the introduction of quantitative easing (QE) programs by the Fed. The Fed purchased large amounts of longer-term securities like US Treasury debt and mortgage-backed securities that are guaranteed by GSEs like Fannie Mae and Freddie Mac. By reducing the supply of these securities, the Fed increased their prices and lowered their yields, an approach designed to buoy mortgage markets and promote recovery. The first QE program was introduced in 2008, and two more rounds followed in 2010 and 2012. The QE programs flooded the banking system with liquidity and made it less necessary for banks to borrow in the federal funds market.

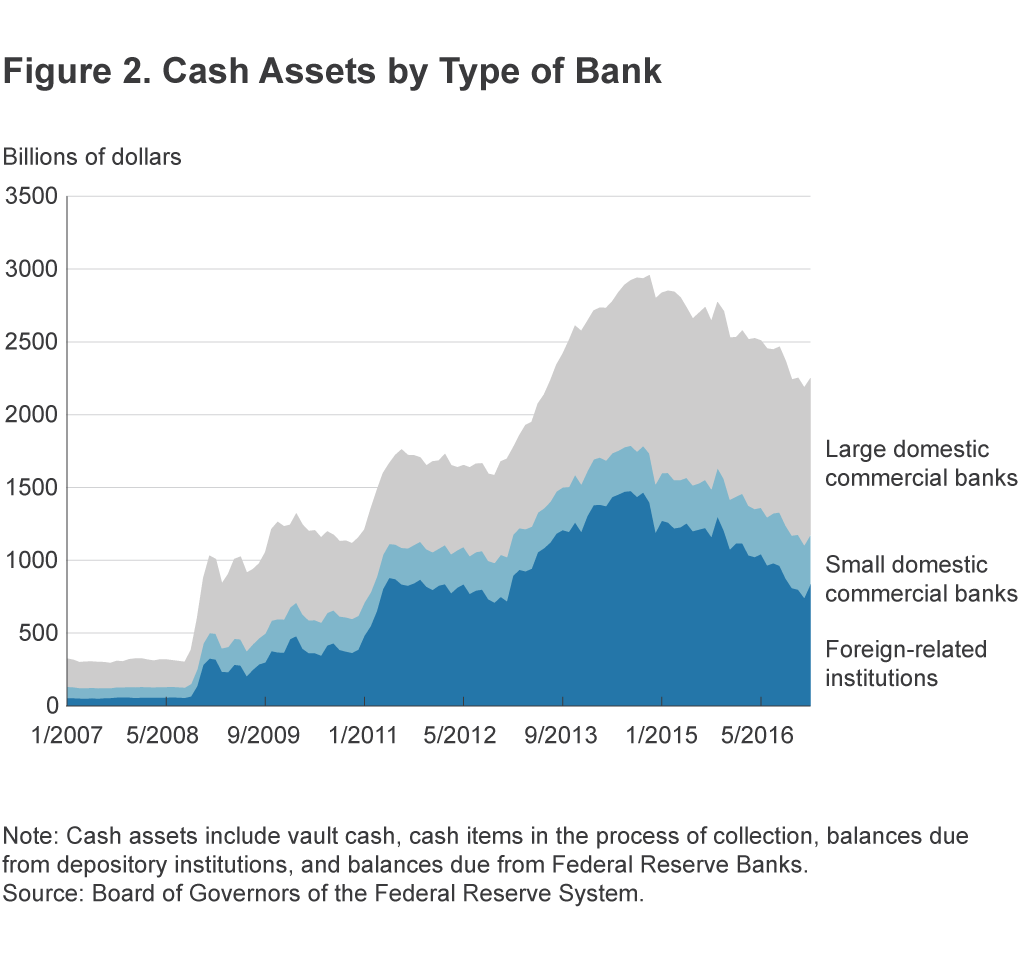

The Fed’s balance sheet growth has been mirrored in the cash holdings of commercial banks (figure 2). The cash assets of domestic commercial banks increased by 467.4 percent between 2007 and 2016, with both large and small banks experiencing increases.1 The US branches of foreign-related institutions and the agencies of foreign banks experienced a huge increase in cash assets as well, of 1,647.6 percent.

While the Fed was responding to the financial crisis and the ensuing recession with three rounds of quantitative easing, Congress was responding with the Dodd–Frank Act. Included in this large act were small changes to the FDIC’s regulatory standards, changes which have had a direct effect on the incentives that banks have to hold cash assets.

The FDIC levies charges on US banks when it provides them with deposit insurance. In April 2011, the FDIC amended its regulations to comply with the Dodd–Frank Act, changing how it would assess an institution’s holdings when the charges for insurance were calculated. Before the regulation was amended, a bank’s fee was based on its deposits; now it is based on its assets. Because cash holdings are a part of assets, the change affects the cost of holding cash. Holding cash received through wholesale funding (borrowing on the interbank market) is costlier now by about 2.5 basis points to 4 basis points (McCauley and McGuire 2014). Foreign banks usually do not have US deposits to insure, and banks with no deposits do not fall under the FDIC’s umbrella and so do not incur this cost.

A second requirement facing the largest domestic banks will take effect in early 2018, when the largest US bank holding companies and their large depository subsidiaries will be required to have achieved an “enhanced supplementary leverage ratio” by January 31. The requirement is based on the ratio of regulatory capital to all balance sheet assets (including cash reserves) and certain off-balance-sheet assets. Expanding the regulation to include cash reserves effectively makes them more costly. All else equal, an increase in cash reserves increases the assets of the institution, which incurs a higher cost from the regulators. As such, it is costlier to borrow in the federal funds market and hold the borrowed cash as reserves. One estimate for a large US bank suggests the cost for holding these reserves could be as high as 35 basis points by January 2018, when the new requirements take effect (Stella 2015). Again, these requirements do not affect foreign banks.

A quick look at banks’ balance sheets suggests that the new leverage ratio requirement has had a significant effect on the cash holdings of both domestic and foreign banks. Foreign banks went from holding about 19.1 percent of the cash reserves held by the banking system in June 2008 to 42.9 percent of the reserves at the end of March 2015. At the same time, the nonreserve assets of foreign banks decreased by $432 billion during this period. Meanwhile, domestic institutions have been charging fees to discourage large investors from making large deposits with them.2

Interest Paid on Reserves

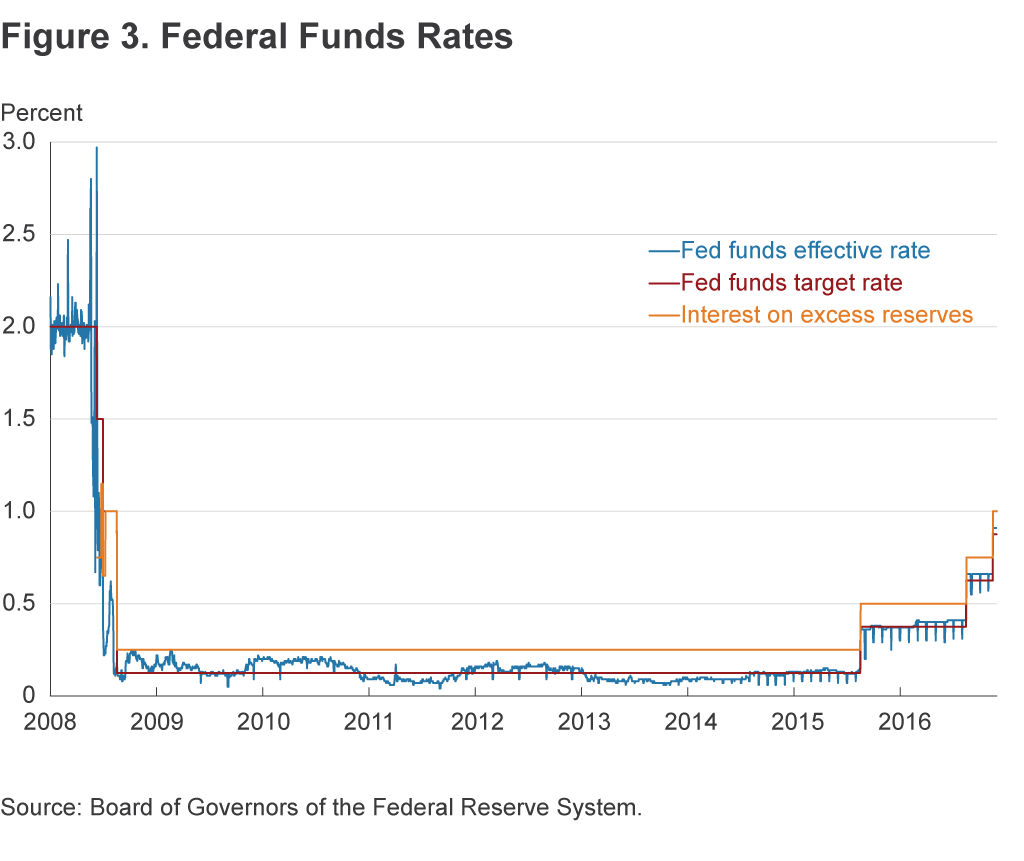

The Fed began paying interest of 25 basis points on excess reserve balances in December 2008, increasing the rate to 50 basis points in December 2015. At first blush, this would seem to give the federal funds rate a floor, a rate below which it would not go. The expectation was that an institution that wished to lend in the federal funds market and earn interest could always hold its reserves with the Federal Reserve (effectively “lending” to the Fed) and earn IOER, which would remove the incentive to accept a rate lower than that in the federal funds market. However, the effective federal funds rate has been consistently lower than the IOER rate since its inception (figure 3). The reason for this is that there are institutions that have reserve accounts at the Fed and participate in the federal funds market but that are not eligible for IOER. Primarily, these institutions are the GSEs Fannie Mae, Freddie Mac, and the FHLBs. These institutions are willing to accept a rate in the federal funds market that is lower than the IOER rate, and this drives the effective federal funds rate below the IOER rate.

The Federal Funds Market Now

Because domestic depository institutions can receive IOER and the effective federal funds rate is below the IOER rate, they have largely ceased lending in the overnight market. This role is now mainly played by the GSEs, especially the FHLBs. On the borrowing side, domestic institutions are awash with reserves from the Fed’s asset purchases, and the FDIC’s new capital requirements penalize them for holding reserves. On the other hand, foreign institutions, many of which have reserve accounts with the Fed, are not under the FDIC’s regulatory umbrella. A foreign bank with an interest-bearing reserve account can borrow from the FHLBs at the federal funds rate, store the cash in its reserve account, and earn IOER minus the rate paid on the federal funds.

Some of the difference in behavior between the foreign and domestic banks in their borrowing may be driven by the fact that the domestic banks are able to get funds from domestic deposits and from cash advances directly from the FHLBs. However, when we observe the total holdings of foreign-related institutions, we see their total asset growth has been driven mostly by their cash assets. Cash made up 5.34 percent of foreign-related institutions’ total assets at the beginning of 2007. By May 2016, it made up 43.77 percent. Foreign-related institutions have increased their holdings of cash by $0.80 trillion since the end of the financial crisis. One explanation for this is that the domestic banks have moved out of the business of arbitraging the difference between the federal funds rate and the IOER rate. They currently fund less of their operations with wholesale cash relative to foreign banking organizations because the foreign banking organizations are taxed less from a capital or insurance requirement standpoint than domestic organizations.

Going Forward

The large increase in the Fed’s balance sheet greatly changed the environment in which the FOMC declares its intention for interest rates by setting a target federal funds rate. Before the crisis, the public announcement of a rate increase was accompanied by a policy at the Fed’s trading desk in which the amount of reserves allocated to the federal funds market was directly reflected in a rate that banks paid one another for overnight liquidity. The further transmission of this policy from the overnight rate into the real economy could be a mystery, but it was plausible to think that affecting the borrowing costs of large domestic financial institutions would affect their domestic counterparties: firms and citizens seeking credit.

Now that the Fed and the FDIC have unilaterally enacted policies that have decreased the role of domestic institutions and increased the role of foreign institutions in the federal funds market, the link between federal funds policy and the real economy is more complex. When a target rate increase is announced, is it accompanied by an increase in the IOER rate? Is the increase accomplished by a sale of securities that are held by the Fed, or is it accomplished by even less straightforward means, such as the Fed’s participation in the repo market?

Each of these decisions affects market institutions and their constituent participants differently. Under some regimes, foreign banks may be affected more than small commercial domestic banks and so forth. Until the various possible effects can be sorted out, we might expect the Fed to behave in a way that is as neutral as possible in the sense of not inducing massive institutional shifts. Making interest rate increases neutral while still changing the rate at which banks lend to each other is harder now. Because the current balance sheet is so huge, an announced policy rate increase could possibly generate surprising results.

Footnotes

- Large banks are defined as the top 25 domestically chartered commercial banks ranked by domestic assets. The small banks are all banks not included in the top 25. Return to 1

- “Banks Urge Clients to Take Cash Elsewhere,” Wall Street Journal, Kirsten Grind, James Sterngold, and Juliet Chung, December 7, 2014. Return to 2

References

- Stella, Peter, 2015. “Exiting Well.” Paper presented at the Joint Central Bank Conference sponsored by the Swiss National Bank, the Bank of Canada, the Federal Reserve Bank of Atlanta, and the Federal Reserve Bank of Cleveland.

- McCauley, Robert, and Patrick McGuire, 2014. “Non-US Banks’ Claims on the Federal Reserve,” BIS Quarterly Review, March, 89–97.

Suggested Citation

Craig, Ben R., and Sara E. Millington. 2017. “The Federal Funds Market since the Financial Crisis.” Federal Reserve Bank of Cleveland, Economic Commentary 2017-07. https://doi.org/10.26509/frbc-ec-201707

This work by Federal Reserve Bank of Cleveland is licensed under Creative Commons Attribution-NonCommercial 4.0 International