- Share

Excess Reserves: Oceans of Cash

Excess reserves—cash funds held by banks over and above the Federal Reserve’s requirements—have grown dramatically since the financial crisis. Holding excess reserves is now much more attractive to banks because the cost of doing so is lower now that the Federal Reserve pays interest on those reserves. The fact that banks are holding excess reserves in response to the risks and interest rates that they face suggests that the reserves are not likely to cause large, unexpected increases in bank loan portfolios. However, it is not clear what banks are likely to do in the future when the perceived conditions change.

The views authors express in Economic Commentary are theirs and not necessarily those of the Federal Reserve Bank of Cleveland or the Board of Governors of the Federal Reserve System. The series editor is Tasia Hane. This paper and its data are subject to revision; please visit clevelandfed.org for updates.

Since the financial crisis, American banks have increased their excess reserves, that is, the cash funds they hold over and above the Federal Reserve’s requirements. Excess reserves grew from $1.9 billion in August 2008 to $2.6 trillion in January 2015.

Why are U.S. banks holding the liquidity being pumped into the economy by the Federal Reserve as excess reserves instead of making more loans? The answer to this question has implications for monetary policy and the real economy, but it is elusive because the current economic environment is complex and still new. However, a first step toward an answer is understanding why banks choose to hold excess reserves in the first place and how their choices have been affected by new Federal Reserve policies introduced in the wake of the financial crisis.

We show that the crisis has altered the trade-off that banks make when calculating their desired levels of excess reserves. Banks now encounter an environment where holding reserves is much more attractive because the cost of holding them—in the form of foregone interest—is significantly lower than it was before the crisis. The Federal Reserve has embarked on several policies designed to pump large amounts of reserves into the banking system, fostering conditions in which it is both easier and more attractive for banks to hold huge amounts of excess reserves.

Choosing the Level of Excess Reserves

One reason banks hold reserves is because they are required to. Currently the Federal Reserve’s Board of Governors mandates that, for net transaction accounts in 2015, the first $14.5 million will be exempt from reserve requirements. A 3 percent reserve ratio will be assessed on net transaction accounts over $14.5 million and a 10 percent reserve ratio will be assessed on net transaction accounts in excess of $103.6 million. Any balances held above this threshold are considered excess reserves.1

Banks also hold reserves to meet their unknown needs for liquidity. Like a tourist who misjudges his cash and must resort to an extremely high-priced foreign ATM machine, a bank’s cash shortfalls cost it money, some of which might have been saved by holding higher amounts of reserves. Reserves can be used for payments, servicing deposit withdrawals, and responding quickly to opportunities for asset purchases and lending that require immediate action.

Deciding how much to hold as reserves rests with the bottom line. Banks actively manage their reserves in order to balance their liquidity needs with the opportunity cost of holding reserves instead of interest-bearing assets. That is, banks measure the cost of carrying more reserves by comparing what they might earn by parking the funds in an alternative asset (“forgone interest”) with the cost of last-minute borrowing to cover an unforeseen shortfall in reserves. The optimal level of excess reserves is usually not zero, because liquidity needs are not perfectly known beforehand.

Before the Crisis

Before October 2008, the costs and benefits of holding reserves were clear. The cost included foregone interest, and the benefits included guarding against last-minute outflows that required immediate cash, much as a depositor might set aside cash to cover emergency expenses, or an investor might hold reserves enabling him to seize an unforeseen opportunity. If a bank did need additional funds, it could obtain reserves through an overnight loan in the federal funds market, where banks with extra reserves lend to other banks. The difference between what a bank could lend and what it could borrow represented the benefit of holding a reserve asset versus the opportunity cost of lending it out.

The total amount of reserves in the banking system was set by the Federal Reserve, largely through open-market operations that supplied and withdrew reserves from the market, in order to stabilize the federal funds rate. There were no interest payments on excess reserves, whether they were held as vault cash or in a Fed account.

From 1959 to just before the financial crisis, the level of reserves in the banking system was stable, growing at an annual average of 3.0 percent over that period. This was about the same as the growth rate of deposits. Moreover, excess reserves as a percent of total reserves in the banking system were nearly constant, rarely exceeding 5.0 percent. Only in times of extreme uncertainty and economic distress did excess reserves rise significantly as a percent of total reserves; the largest such increase occurred in September 2001.

The Current Environment

To deal with the 2008 financial crisis, the Federal Reserve pumped large amounts of reserves into the banking system and introduced new programs that altered the terms of the trade-off banks make when deciding their level of excess reserves. In short, the marginal benefit of holding additional reserves has increased, whereas the marginal cost has decreased. As a result of these new Federal Reserve policies, holding reserves is now much more attractive to banks. It is more attractive because the cost of holding excess reserves—in the form of forgone interest—is significantly lower than it was before the crisis.

One reason for the increased marginal return of holding reserves is that the Federal Reserve now pays interest on all reserves. Since December 2008, the Federal Reserve has paid interest of 25 basis points on all reserves.2

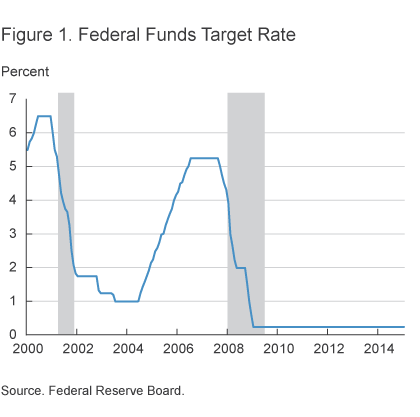

Before the crisis, banks commonly parked their cash in the federal funds market for short periods. The interest rate in this market, hovering between 7 and 20 basis points since the crisis, has actually lagged the interest rate paid by the Federal Reserve for excess reserves (figure 1).

The marginal cost of excess reserves has also declined, when measured by the opportunity cost of other uses for the reserves. Other short-term parking places where banks commonly earned interest have experienced rate drops that make them less favorable. For example, since the Federal Reserve began to pay interest on excess reserves, three-month Treasury bills have yielded less than the Fed pays.

Moreover, other investments have a low interest rate and perhaps a perceived risk of increased defaults, as in the case of some overnight loans. This also reduces the opportunity cost of holding reserves. Thus, the level of reserves at which the marginal cost of holding an additional dollar of reserves equals the marginal benefit of doing so is much higher now than it was before the financial crisis. One consequence of high excess reserves is that the federal funds market for last-minute funds has essentially dried up.

Finally, although the perceived risk of counterparty default has lessened since the height of the crisis, it still exceeds its pre-crisis level. The counterparty default risk associated with banks lending to other banks can be measured with the LIBOR-OIS spread, which has come down significantly since the financial crisis. It increased slightly toward the end of 2011 but has remained relatively flat since the beginning of 2013.

Conversely, holding liquid assets is subject to decreased short-run inflation risks, which many believe are at an all-time low. So a holder of these safer reserves (which now pay interest) is faced with alternatives that have higher default and duration risks. They also pay a historically small return. Not surprisingly, banks’ preferences have shifted markedly toward holding large balances of excess reserves.

Expansion of Excess Reserves by the Federal Reserve

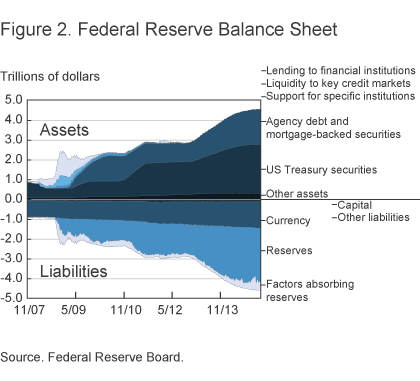

The increased demand for reserve assets has been matched by the Fed’s willingness to supply them. In responding to the financial crisis, the central bank implemented a series of credit-easing policies that included lending to financial institutions, providing liquidity to key credit markets, and purchasing long-term securities. Total reserves in the banking system expanded 326.9 percent in 2008 and another 389.6 percent in 2009 (figure 2).

One large liquidity program has been the Fed’s purchase of federal agency debt and mortgage-backed securities. In the wake of the housing crisis, the Federal Reserve sought to reduce mortgage rates by increasing the demand for agency-guaranteed, mortgage-backed securities. As a consequence of the Federal Reserve’s asset purchases, the amount of excess reserves in the banking system expanded greatly. By January 2015, the Federal Reserve held just over $1.8 trillion dollars of agency debt and mortgage-backed securities and an additional $2.5 trillion of Treasury securities.

A quick comparison of the Fed’s balance sheet and the amount of excess reserves shows an almost one-to-one correspondence between the two. This should not be surprising, since excess reserves are part of the banking sector’s assets and the central bank’s monetary liabilities. The Fed’s actions to increase its monetary liabilities will raise bank reserves by a like amount, unless public demand for cash rises sharply. Because risk-adjusted returns on assets are so low, banks are holding these assets as cash instead of cycling the liquidity through the system in the form of loans. Consequently, despite massive infusions of liquidity into the system, banks’ lending has increased only slowly, and after a long period of decline.

Implications

The simplicity of the one-to-one correspondence between the Federal Reserve’s balance sheet and excess reserves hides the difficulty involved in predicting how banks are likely to behave in the presence of the expanded reserves. Unfortunately, understanding this behavior is what matters for deciding on an appropriate policy for excess reserves.

The fact that banks are holding excess reserves in response to the risks and interest rates that they face suggests that the reserves are not likely to cause large, unexpected increases in their loan portfolios. However, it is not clear what banks are likely to do in the future when the perceived conditions change or which conditions are likely to bring about a massive change in their use of excess reserves. Recent history is not much help in determining the answer to this question because no balances this big have been seen in recent times.

Does this mean that the Federal Reserve should consider a major policy change that would remove some of the excess reserves as a safety measure? Such a measure might include raising the reserve requirement, charging interest on excess reserves, and removing liquidity from the system.

Here is where the more distant history of the Great Depression provides a cautionary lesson. In 1936, US banks’ reserves had accumulated to record levels. Although there had not been a dramatic increase in the levels of loans, the Federal Reserve decided to “play it safe” and reduce the flexibility of the banks’ options for using the cash by increasing the reserve requirement. Banks responded by dramatically reducing their loan portfolios. Milton Friedman and Anna Schwartz argued that this action caused the 1937 recession (A Monetary History of the United States, 1867-1960).

So the Federal Reserve has no easy policy choices, particularly in the absence of a large body of accepted theory on how banks can be expected to handle their oceans of cash under changing conditions. Perhaps the best thing to do is what they are doing, that is, to adopt an extremely watchful stance and wait.

Footnotes

- This reserve requirement is a bit of a fiction. Since 1994, banks have lowered the computed amount of required reserves by altering the amount of reservable liabilities on their balance sheet. In the process for doing this, banks use computer technology to temporarily “sweep” deposits from one type of account to another overnight, reducing reservable liabilities and hence required reserves. Return

- Between October 15 and December 10, 2008, the Fed paid rates between 65 and 100 basis points for excess reserves. Return

Suggested Citation

Craig, Ben R., and Matthew M. Koepke. 2015. “Excess Reserves: Oceans of Cash.” Federal Reserve Bank of Cleveland, Economic Commentary 2015-02. https://doi.org/10.26509/frbc-ec-201502

This work by Federal Reserve Bank of Cleveland is licensed under Creative Commons Attribution-NonCommercial 4.0 International