- Share

Reassessing the Effects of Extending Unemployment Insurance Benefits

To deal with the high level of unemployment during the Great Recession, lawmakers extended the availability of unemployment benefits—all the way to 99 weeks in the states where unemployment was highest. A recent study has found that the extensions served to increase unemployment significantly by putting upward pressure on wages, leading to less jobs creation by firms. We replicate the methodology of this study with an updated and longer sample and find a much smaller impact. We estimate that the impact of extending benefits on unemployment through wages and job creation can, at its highest, account for only one-fourth of the increase in the unemployment rate; an impact that is much lower than other estimates in the literature.

The views authors express in Economic Commentary are theirs and not necessarily those of the Federal Reserve Bank of Cleveland or the Board of Governors of the Federal Reserve System. The series editor is Tasia Hane. This paper and its data are subject to revision; please visit clevelandfed.org for updates.

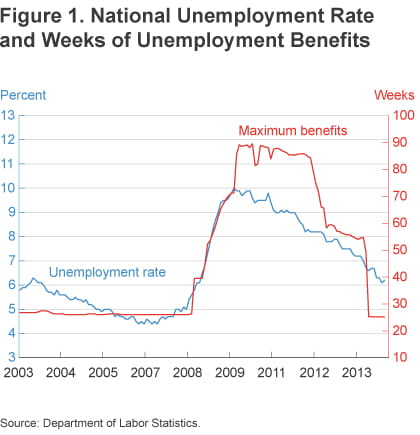

In October 2009, the civilian unemployment rate in the U.S. touched 10 percent, higher than at any time since WWII save a year in the mid-1980s (figure 1). This severe, almost unprecedented, increase in unemployment prompted equally unprecedented public policy responses from federal and state governments. One of those responses, the extension of unemployment insurance (UI) benefits, has been criticized for incentivizing workers to stay unemployed and keeping the unemployment rate higher than it would have been otherwise.

A number of studies documenting this incentive effect show that it was small in the last recession (Rothstein 2011, Farber and Valetta 2013). However, a more recent study by Hagedorn, Karahan, Manovskii, and Mitman (2013), HKMM henceforth, finds that benefits extension has had a substantial impact on unemployment. Their study differs from others in that it takes into account the impact of extensions on labor demand, as well as labor supply. They note that, as the generosity of benefits increases, the fact that unemployment becomes relatively more attractive puts pressure on wages to increase.

As a result, firms post fewer vacancies, fewer jobs are created, and unemployment goes up, everything else being the same. HKMM find that this effect can account for most of the increase in the unemployment rate during the recession and recovery. We argue that such a finding is not robust when considering either a longer or more adequate sample. We find that this labor demand channel can account for roughly only one-fourth of the increase in the unemployment rate.

Historically, UI benefits have consisted of three major components: regular unemployment compensation, extended benefits, and emergency unemployment compensation.

Regular unemployment compensation programs are funded by state unemployment taxes, and the length of benefits is determined by each state’s legislature. Prior to the Great Recession, the large majority of states set the maximum number of weeks of regular benefits at 26. (Massachusetts and Montana, with 30 and 28 weeks of benefits, respectively, are the exceptions.) Once individuals exhaust these regular benefits, and if their state meets certain unemployment and legal requirements, they are able to apply for extended benefits.

Extended benefits allow for an extension of benefits of up to 13 weeks, with a few states opting into a provision that permits extensions of up to 20 weeks. Extended benefits are jointly financed by federal and state governments and were enacted with the Extended Unemployment Compensation Act of 1970 to combat increased unemployment during recessions. In the years leading up to the law’s passage, the rate of participants enrolled in the UI program had increased dramatically over previous years. The longer extension of 20 weeks is provided if states decide to opt into a provision where the funding is determined by total unemployment rates rather than the rate of people who are claiming UI benefits (“insured unemployment rate); however, few states have opted into this provision.

With the onset of the Great Recession, the Supplemental Appropriations Act of 2008 allowed, among other things, for a third component to be added to UI benefits: Emergency Unemployment Compensation (EUC), available to qualified claimants who exhaust regular UI benefits. The bill started by providing all states with a federally funded 13-week extension of benefits and was subsequently revised multiple times through various legislative measures. The final legal framework of EUC provided a federally funded four-tier system of benefits, with durations for each tier depending on a state’s total or insured unemployment rate. Moreover, statutory durations for each tier kept changing over time throughout the recession and recovery: the first tier went from 13 to 20 weeks and then back to 14 weeks; the second tier provided an additional 13 and then later 14 weeks; the third tier started by providing an additional 13 and later 9 weeks; finally, the fourth tier started by providing an additional 6 weeks of compensation, which increased to 16, came back down to 6, and finally ended up at 10 before dropping to 0.

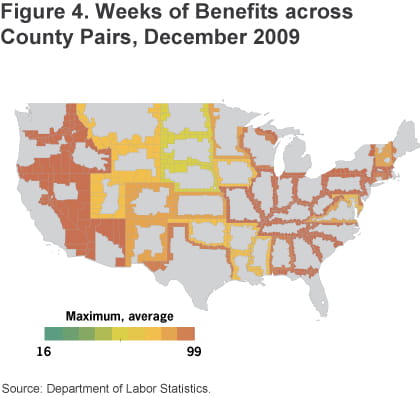

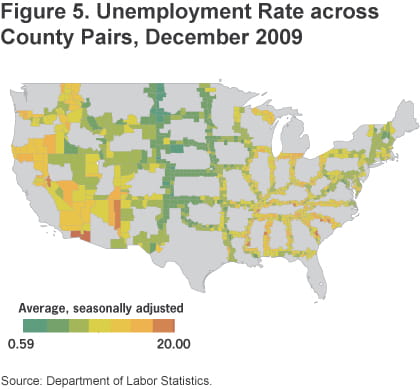

This rather byzantine system meant that the maximum duration of benefits any individual could be eligible for topped 99 weeks during the time extended benefits were in force (they ended in January 2014), with the national average at 89.6 weeks. Figures 2 and 3 show the cross-country variation in weekly benefits (state-by-state) and in unemployment rates (county-by-county) in December 2009.

Figure 2. Weeks of Benefits by State, January 2003 to January 2014

Figure 3. Unemployment Rate by County, January 2003 to January 2014

The Economics of UI Benefits

The channels through which UI benefits policy may affect labor market outcomes and economic growth are numerous. The most obvious is that it may stimulate demand by putting money in the hands of the unemployed, who are potentially less likely to save those dollars than the average taxpayer. Moreover, a more generous UI policy can have a liquidity effect that helps subsidize the job searches of unemployed workers who are more likely to be financially constrained, potentially leading to better, more productive job matches. Finally, more generous UI benefits may lead to higher unemployment by reducing job creation by firms. The argument is that better UI benefits increase the option value of being unemployed, putting upward pressure on wages and downward pressure on firm profits. As a response, firms will create fewer jobs, resulting in increased unemployment.

Unfortunately, similar to other forms of insurance, UI has a trade-off embedded in its core. By making leisure less costly relative to consumption, more generous UI benefits reduce the incentive to search for a job (what economists call moral hazard).

While these effects may sound simple enough, they are extremely hard to assess empirically. This is not only because they are confounded by other shocks the policy is responding to, which makes it hard to identify what is causing what, but also because both the underlying shocks as well as the policy responses give rise to changes in market prices that are hard to control for.

For example, while earlier analyses like Moffit (1985) and Meyer (1990) established a link between more generous UI benefits and increased unemployment spells, Chetty (2008) estimated that over half of this increase was due to the liquidity effect as opposed to the moral hazard effect. That is, part of the increase in unemployment spells was resulting from the fact that workers could actually afford to finance longer spells in order to obtain better job matches.

A Different Way to Identify the Impact of UI Benefits Extension

In order to properly measure the impact of extending the duration of UI benefits on the unemployment rate, one would need to compare the US economy to an economy that is exactly the same as the US except for the UI benefit extension. Needless to say, such an experiment is impossible. The fundamental problem is one of endogeneity: The duration of UI benefits and the unemployment rate affect each other. Changes in duration may affect unemployment rates through any of the channels discussed above, while at the same time independent increases in unemployment rates trigger statutory increases in the maximum duration of UI benefits.

In an attempt to circumvent this problem and properly identify the impact that changes in UI benefits duration have on unemployment rates, HKMM developed an empirical strategy in which they looked at neighboring counties across state lines, like Ashtabula County in Ohio and Erie County in Pennsylvania, for example. HKMM reasoned that if both counties are buffeted by the same economic shocks (because of proximity) but are subject to different UI policies (because they are in different states), one can isolate the impact from different policies from the impact of different economic shocks. The impact of changing UI benefits duration can be inferred by looking at the differences in unemployment rates between the two counties (if properly controlling for other differences).

Importantly, HKMM incorporate interactive fixed-effects, so their model allows for economic shocks to have different impacts in different counties at different points in time. This is a more flexible structure than one incorporating time fixed-effects (which are the same for all counties at any point in time) or county fixed-effects (which apply to a given county at all times). Consider the early days of the Great Recession and a shock that affects the financial services industry disproportionately. One would expect counties in and around Connecticut to be more impacted than those in North Dakota. Now go forward in time and consider a shock due to an oil and gas extraction boom, and the opposite is true. Interactive fixed effects will be able to capture this difference.

Different Results with a Longer Sample

We use the same methodology as HKMM and reassess the effect of the recent extension in UI benefits duration on unemployment. We do this because we now have a longer sample than HKMM had available. Figures 4 and 5 highlight what the weekly benefits and unemployment rates were in December 2009 for the county pairs in our sample.

We also take a closer look at the Fourth Federal Reserve District. This region was particularly hard hit by the recession, so we wanted to see if it plays an important role in driving the overall US results.

Our data for seasonally adjusted unemployment rates is from the Local Area Unemployment Statistics (LAUS) maintained by the Bureau of Labor Statistics (BLS). We have a quarterly data panel, from the first quarter of 2003 to the fourth quarter of 2013 for 1,156 border county pairs. We have also compiled data from various sources (chiefly the Department of Labor’s Employment and Training Administration but also various state sources) on the maximum amount of weeks of UI benefits available to qualifying workers. We regress unemployment rates on benefits duration and (unknown) interactive factors to obtain an estimate of how the unemployment rate changes when the duration of UI benefits changes.

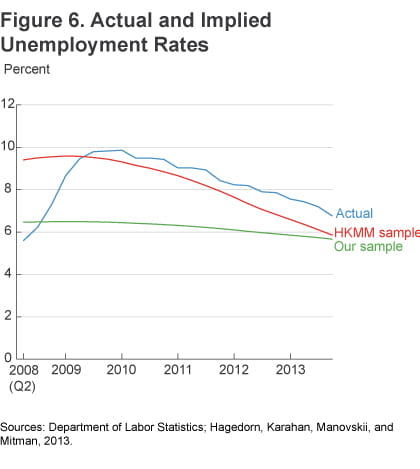

Next we calculate the unemployment rate that would be implied by our estimate and the one that would be implied by HKMM’s estimate, and we plot these against the actual unemployment rate (figure 6). The implied unemployment rates represent what the unemployment rate would have been, taking into account the extensions in unemployment insurance and holding all other factors constant. When calculating the implied unemployment rates, we deal with all the changes in the maximum number of benefit weeks in the following way. We start in the second quarter of 2008 (at the end of which EUC was introduced) and assume that people expect that the maximum number of weeks of benefits will stay the same forever (that is, until the end of our sample period, the end of 2013). Then we move to the next quarter and do the same. For example, take the second quarter of 2008: at that point, the average maximum of weekly benefits was 71.6. We assume people thought that level would be in place until the end of 2013 and obtain an implied unemployment rate for the second quarter of 2008. In the next quarter, the average maximum weekly benefits increased to 73.7, so again we assume people thought that level would be in place until the end of 2013, and so forth.

Our estimate implies that the unemployment rate would be 6.45 percent in the second quarter of 2008 (85 basis points above the actual rate) and would then increase to a maximum of 6.5 percent three quarters later before tapering out. While a jump of roughly 1 percentage point in the unemployment rate is substantial, it is much smaller than what the estimate implied by the HKMM would produce, and accounts for only a fraction of the increase in the actual unemployment rate throughout the recession and recovery.1

There are two main reasons for this discrepancy. The first has to do with the longer sample we are using. HKMM’s sample extends from the first quarter of 2005 to the first quarter of 2012, while ours reaches back to 2003 (HKMM faced restrictions from other data sets we are not using) and forward to the end of 2013. While there were not many changes in benefits between 2003 and 2005, including these years allows the model to better capture the interactive factors—whatever variation there was in the unemployment rate in those years would be largely attributable to those outside factors, allowing greater precision in estimating their effects on the unemployment rate. Importantly, the period between mid-2012 and the end of 2013 allows the model to capture the decline in benefits and even the end of EUC in North Carolina that occurred in mid-2013.

The second reason has to do with the exclusion of outliers. We opted for excluding the county pairs where at least one of the counties experienced a monthly change in the unemployment rate that is larger than 10 percentage points at any point in the sample period. The goal was to exclude data oddities like the occasional unemployment spikes in tiny Sargent County, North Dakota, which shows up in two county pairs; but more importantly, this means we are excluding seventeen other county pairs that were affected by major natural disasters at some point in time. One might think that including a phenomenon like Hurricane Katrina could help with the regression as its effects do not have to stop at the county borders and it could therefore help with identifying the impact of extending unemployment benefits. The problem is that the effects of the hurricane were felt disproportionately in Louisiana, to an extent that the duration of UI benefits was affected there, but not in neighboring states. Therefore, the regression that includes these county pairs in the sample misattributes the higher increase in the unemployment rate in Louisiana counties to the increase in unemployment benefits there.

As the example with Hurricane Katrina shows, an issue that may potentially plague this methodology is the inclusion of county pairs where at least one county is large enough to meaningfully affect its state’s unemployment rate. The endogeneity problem would arise again, despite the differencing between border counties, if a shock to one of the counties that is large enough to affect its state’s unemployment rate ends up triggering an extension of UI benefits in one of the states and not in the other. Most of the counties in the sample are very small, in terms of employment, relative to their state. Yet the large ones may be driving a disproportionate part of the action. We conducted a series of experiments in which we excluded those pairs where at least one of the counties is responsible for more than 15 percent of its state’s employment; the effect would be smaller, but not substantially so, with the unemployment rate peaking instead at 6.4 percent.

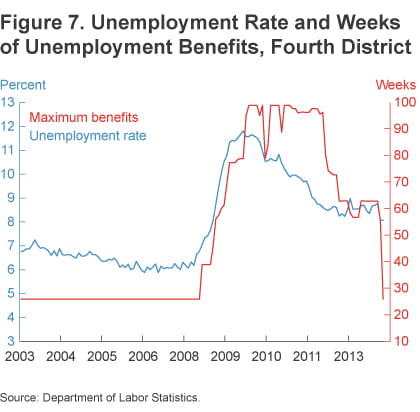

The Fourth District

The Fourth District2 experienced particularly high unemployment throughout the recession and subsequent recovery. The unemployment rate climbed all the way to 12 percent at its peak, almost a full two percentage points above the national average. Not surprisingly, UI benefits were also higher on average, with the full 99 weeks of benefits available for considerable periods of time during 2009 and 2010 (figure 7).

Our estimate for the impact of UI benefits on the unemployment rate in the Fourth District is not statistically different from zero. Even though it is higher than the estimate we calculated at the national level, there is considerable uncertainty around it. This is most probably the result of the smaller sample size, as we have only 97 border county pairs in the Fourth District; but this would also be consistent with relatively less wage pressure in the Fourth District compared to the whole country, although there is no hard evidence that that is indeed the case.

Conclusion

Our analysis indicates that the impact of extending the duration of UI benefits on unemployment during the last recession was positive, but modest when compared to other estimates in the literature. We estimate that had the duration of UI benefits not been extended, the unemployment rate would have increased roughly one percentage point less from June 2008 to its peak in October 2009, everything else being the same. While this effect is important, it can only account for a fraction of the actual increase in the unemployment rate.

It is important to understand the effect of UI benefits duration on the unemployment rate is only one aspect of the more general effects of UI benefits generosity. More generally, UI benefits operate through alternative channels we are ignoring here in affecting other variables like the degree to which workers are financially constrained, and ultimately welfare and inequality. A sensible benefits policy needs to take these dimensions into account in addition to the results found in this study.

Footnotes

- In interpreting all of these estimates one should note that there is an issue of external validity; we are extrapolating from the estimates we are getting from all the border county pairs to the whole country. Return to 1

- The Fourth District of the Federal Reserve System comprises Ohio, western Pennsylvania, eastern Kentucky, and the northern panhandle of West Virginia. Return to 2

References

- Chetty, Raj, 2008. “Moral Hazard versus Liquidity and Optimal Unemployment Insurance,” Journal of Political Economy 116(2), pp. 173-234.

- Farber, Henry S., and Robert G. Valletta, 2013. “Do Extended Unemployment Benefits Lengthen Unemployment Spells? Evidence from Recent Cycles in the U.S. Labor Market,” Federal Reserve Bank of San Francisco, Working Paper 2013-09.

- Hagedorn, Marcus, Fatih Karahan, Iourii Manovskii, and Kurt Mitman, 2013. “Unemployment Benefits and Unemployment in the Great Recession: The Role of Macro Effects,” National Bureau of Economic Research, Working Paper, no. 19499.

- Meyer, Bruce D., 1990. “Unemployment Insurance and Unemployment Spells,” Econometrica, 58(4), pp. 757-82.

- Moffit, Robert, 1985. “Unemployment Insurance and the Distribution of Unemployment Spells,” Journal of Econometrics, 28, pp. 85-101.

- Rothstein, Jesse, 2011. “Unemployment Insurance and Job Search in the Great Recession,” NBER Working Paper 17534.

- Whittaker, Julie M., and Katelin P. Isaacs, 2014. “Unemployment Insurance: Legislative Issues in the 113th Congress,” Congressional Research Service, CRS Report R242936.

The authors thank Bruce Madson at the Ohio Department of Job and Family Services, Thomas Stengle at the Department of Labor, Lockhart Taylor at the North Carolina Department of Commerce, Iourii Manovskii at the University of Pennsylvania, and Kurt Mitman at the Institute for International Economic Studies at Stockholm University.

Suggested Citation

Amaral, Pedro S., and Jessica Ice. 2014. “Reassessing the Effects of Extending Unemployment Insurance Benefits.” Federal Reserve Bank of Cleveland, Economic Commentary 2014-23. https://doi.org/10.26509/frbc-ec-201423

This work by Federal Reserve Bank of Cleveland is licensed under Creative Commons Attribution-NonCommercial 4.0 International