- Share

Are We Like Sweden? Recovery in the Labor Market

More than 20 years ago Sweden suffered a severe financial crisis that brought unemployment to an all-time high. To this day the unemployment rate has not returned to where it was before the crisis. Economists say that if the U.S. is anything like Sweden, our full recovery may still be a long way off. Sweden is like the U.S. in many ways, but the roots of its labor market troubles appear to be very different from ours.

The views authors express in Economic Commentary are theirs and not necessarily those of the Federal Reserve Bank of Cleveland or the Board of Governors of the Federal Reserve System. The series editor is Tasia Hane. This paper and its data are subject to revision; please visit clevelandfed.org for updates.

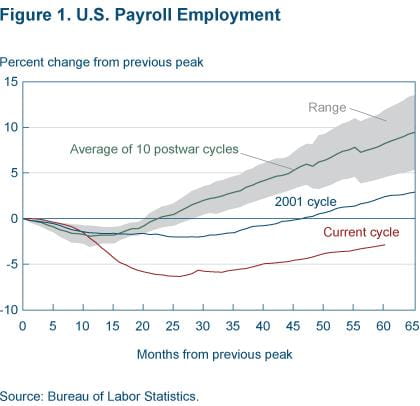

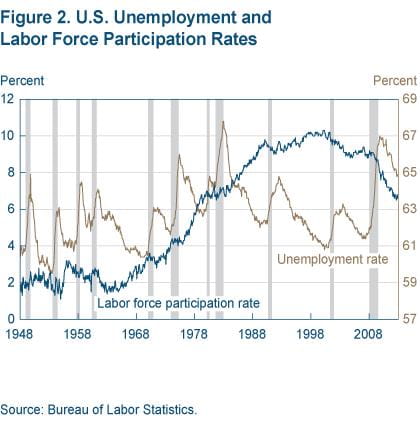

The recovery in the labor market after the last recession has been sluggish by any measure. In a typical recovery, payroll employment returns to its pre-recession level in under two years, yet today, at 60 months and counting since the last peak, we are still quite a way off from that point (figure 1). On top of the slow growth of jobs, the labor market participation rate has also declined significantly, which means that many people have given up on their job search and are no longer actively looking for a job (figure 2). It’s a troubling trend, as their job skills could quickly become obsolete in the rapidly advancing world of technology.

Source: Bureau of Labor Statistics

Source: Bureau of Labor Statistics

The short-term outlook for the labor market has many people asking how long it will take to get to a full recovery. Forecasters have given a broad range of answers, and those answers are based on very different assumptions about the reasons the recovery is so slow. Some forecasters assume all of the sluggishness can be attributed to the severity of the recession; others assume the labor market has undergone a structural change that will take everyone time to adjust to. Those in the latter camp put a full recovery farther out, and say there is even more than the usual uncertainty about when it will happen.

It’s important to know what someone’s view on this issue is when you’re evaluating their labor market forecasts or the policy responses they’re proposing. Some economists, as a case in point, have suggested that we can look to Sweden’s experience after a major financial crisis 20 years ago to get ideas about how long our full recovery will take and what interventions we might consider. With its wealthy citizenry, strong adherence to the rule of law, and successful handling of the financial crisis, Sweden may indeed be an appropriate comparison to the current situation in the United States—though a gloomy one since the Swedish labor market has still not returned to its pre-crisis state after 20 years. But Sweden’s labor market problems were a textbook case of structural change, and the relevance of Sweden’s experience to the U.S. depends on how closely the U.S. labor-market adjustments parallel the adjustments that occurred in Sweden.

Sweden’s Crisis

Two seemingly independent components merged to create the perfect storm that engulfed Sweden in 1990. On the one hand, Sweden had relied heavily on export-based industries (such as shipbuilding) for economic growth. Various policies were put in place to keep those industries competitive in the face of global economic changes. For example, credit was rationed to households and domestic businesses so that the export industries could get the credit they needed. The exchange rate was pegged to a basket of currencies (the U.S. dollar and German mark) and cross-border capital flows were restricted to maintain control over domestic interest rates.

On the other hand, Swedish policymakers of all political convictions were committed to keeping unemployment low and promoting “economic equality.” Shipbuilding seemed the ideal industry to achieve these goals, as it required many skilled workers and supported multiple side industries such as steel mills, railroads, and various parts suppliers, and so the industry was more heavily subsidized than others.

In the 1970s, it all came to a head. First, the shipbuilding industry started facing tough competition from Japan in the 1960s and Korea in the early 1970s. Then came the oil shock that reduced the global demand for Swedish products. It did not help that, as happens with any state-sponsored industry, the country had built significant overcapacity in its shipyards. Public comments from the policymakers of that period suggest that they viewed the doldrums of this and associated industries as temporary; the recovery was always thought to be around the next corner.

The government reacted to the “temporary” troubles of its failing industries by providing additional subsidies and discouraging layoffs, as well as creating jobs in the public sector. Consequently, public sector employment ballooned from 20 percent of total employment in 1965 to 30 percent in 1975 and 38 percent in 1985. Public spending grew in tandem, from 31 percent of GDP in 1960 to 61 percent in 1983. In comparison, public spending in the U.S. grew from 28 percent of GDP to 36 percent over the same period. The way the government paid for the spending was to borrow heavily in international markets and to levy higher taxes. The marginal income tax rate on full-time workers earning the average hourly wage increased from 35 percent in the second half of the 1960s to 65 percent in 1976.

By the late 1970s, economic growth was sluggish and inflation was topping 15 percent. When a country has fixed exchange rates, its exports will quickly become uncompetitive if its production costs are rising rapidly. This is what happened to Sweden. The government responded with a series of currency devaluations and wage and price freezes. In the absence of any change in the unsustainable spending policies, inflation never came under control and the positive effects of the devaluations on exports dissipated quickly.

During the 1980s, the government seems to have identified three problems with the economy, as revealed by its policy choices. First was high inflation. Second was the impact of credit market restrictions on domestic investment and consumption. And third was the government’s ballooning foreign-exchange-denominated liabilities, a sign of the lack of fiscal discipline. The first issue was dealt with by allowing cross-border capital flows (opening the capital account) while maintaining the currency peg, which essentially handed over the control of domestic interest rates to the foreign central banks represented in the basket (which had a better record of fighting inflation).

To address the second problem, the government lifted the credit and interest rate caps on domestic borrowers and allowed companies to borrow in international markets. Once the flood gates opened, a credit boom and a housing bubble ensued.

The third problem of heavy foreign borrowing was perhaps politically the most challenging. Instead of attempting to dismantle its costly policy of providing employment security, the government committed itself to borrowing only in kronas. This policy was expected to impose discipline by reducing the government’s access to cheap credit, but it only transferred the foreign exchange risk from the government to financial institutions, which borrowed in international markets and then lent to the government in kronas.

Unfortunately, inflation never came down to the levels of Sweden’s trading partners. Maintaining the currency peg required high domestic real interest rates. The currency peg must have seemed credible because many Swedish companies borrowed heavily in foreign currencies to escape high domestic real interest rates. But as a result, those companies took on large exposures to exchange rate risk.

After the German unification, Germany’s real interest rates jumped as a result of high unification costs. The fixed exchange rate obliged Sweden to import the higher German real interest rates, pushing its own already-high domestic rates even higher. Once the rates became too much to bear, the fixed exchange rate became indefensible, and the Swedish financial system collapsed.

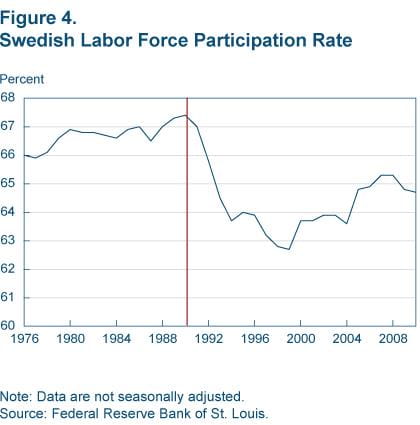

To this day, the labor market picture in Sweden shows the impact of their financial crisis (figures 3 and 4). While the Swedish unemployment rate has come down from its crisis peak and the labor force participation rate has somewhat recovered, neither has come close to its pre-crisis level.

Scource: Statistika Centralbyran, Haver Analytics.

Note: Data are not seasonally adjusted.

Source: Federal Reserve Bank of St. Louis.

Lessons for the U.S.

This brief flashback may contain a part of the explanation for why Swedish labor market statistics have not fully returned to their pre-crisis levels. One study of public sector employment policies published in 2008 by Hans-Ulrich Derlien and Guy Peters indicates that for many years, the labor market had been kept artificially tight by government policies that replaced disappearing jobs in failing industries with jobs in the government. The financial crisis was the breaking point of an economic system that had grown increasingly more unstable over a long period of time. It was a watershed event that marked the end of an unsustainable structure and the beginning of a new one. Public sector employment declined from 423,000 in 1985 to 240,000 in 1996 mainly through the privatization of large employers—like the Swedish postal service, the Swedish Telecommunications Administration, and Vattenfall, the electricity enterprise—and it has remained almost flat since then.

With such a large structural change, what came before the crisis may no longer be a reference point for what will come after. Having corrected the root of the problem, the Swedish labor market is now operating at a new equilibrium.

Has there been such a structural shift in the U.S. labor market? A number of economists have argued that the housing boom hid some long-term weakness in the labor market that is becoming apparent in the wake of the financial crisis. There is some validity in the argument that during the credit and housing boom of the last decade many individuals developed skills in the construction, real estate, and mortgage industries that may no longer be needed going forward. However, economic models used at the Federal Reserve Bank of Cleveland suggest that structural issues are not the primary driver of sluggish job growth in the United States.

Instead, as I see it, there seem to be two culprits behind slow employment growth now, and they are not primarily due to skills mismatch. The first is reduced consumption due to the shock to households’ balance sheets. People consume less when they get poorer, and people did get poorer during this crisis when home prices crashed, especially when one considers households’ high debt loads (figure 5). So, for example, when consumers realize they can no longer draw on their home equity credit lines, they buy fewer cars, which means that workers lose their jobs in auto manufacturing plants. Auto workers remain unemployed not because their skills are stale but because the demand for autos (and other manufactured goods) has declined. Thus the situation in the United States is more of an issue related to the demand for products and the severity of the recession, not to the structure of the labor market.

Source: Federal Reserve Board.

The second culprit follows from the simple math of the labor market: unemployment will decline when more people find jobs than are losing them. The dynamism of the labor market—the rate at which people quit their jobs and find new ones—is a key determinant of how quickly the labor market will reach its equilibrium, which is currently estimated to be an unemployment rate of around 5 to 6 percent. For reasons still being researched by economists, the dynamism of the U.S. labor market has been slowing down for many decades. Even if the research determines that there is a structural reason behind the slowing job flows (an aging population could be one example), this is still a long-term process, unrelated to the upheaval created by the financial crisis.

What we observe in the job market today is consistent with what would be predicted from a deep recession and stunted recovery. Since Sweden’s labor market problems had structural features that we do not see in the United States, the Swedish experience would appear to shed little light on when the U.S. will achieve a full recovery.

Recommended Reading

- The State at Work: Public Sector Employment in Ten Western Countries, Hans-Ulrich Derlien, and B. Guy Peters, 2008. Edward Elgar Publishing, U.K.

- “What Explains High Unemployment? The Aggregate Demand Channel,” Atif Mian and Amir Sufi, 2011. NBER working paper no. 17830.

- “This Time May Not Be That Different: Labor Markets, the Great Recession and the (Not So Great) Recovery,” Murat Tasci, 2011. Federal Reserve Bank of Cleveland, Economic Commentary, no. 2011–18.

- “Maximum Employment: What We Know (and Don’t Know) about the Labor Market,” Federal Reserve Bank of Cleveland Annual Report, 2011.

Suggested Citation

Ergungor, O. Emre. 2013. “Are We Like Sweden? Recovery in the Labor Market.” Federal Reserve Bank of Cleveland, Economic Commentary 2013-03. https://doi.org/10.26509/frbc-ec-201303

This work by Federal Reserve Bank of Cleveland is licensed under Creative Commons Attribution-NonCommercial 4.0 International