- Share

Time-Consistent Rules in Monetary and Fiscal Policy

The intended effects of a government policy can be distorted by the public’s expectations about how strictly it will be enforced. If households and businesses cannot be certain that a policy will remain unchanged over its scheduled tenure, they will adjust their response to it to reflect this uncertainty. One way of mitigating the uncertaintly is to add rules to new policies when they are enacted that would make altering the policies very difficult in the future.

The views authors express in Economic Commentary are theirs and not necessarily those of the Federal Reserve Bank of Cleveland or the Board of Governors of the Federal Reserve System. The series editor is Tasia Hane. This paper and its data are subject to revision; please visit clevelandfed.org for updates.

When it comes to government finance, it’s not just laws and policies about taxes, spending, or inflation that affect macroeconomic outcomes like growth and unemployment. Expectations matter, too. Beliefs about how the future will unfold and the way that the government will react change what can happen today. Expectations matter both for central banks, which manage monetary policy, and for government executives and legislators, who set fiscal policy.

The Federal Reserve learned its lesson on expectations in the early 1980s, when Chairman Volcker decided to bring inflation under control. That task required resetting market inflation expectations, and he had to undertake contractionary monetary policy in order to do it. The lesson was demonstrated recently for fiscal policy in European sovereign debt markets, after market confidence in the ability or willingness of some countries to repay their debt obligations eroded, resulting in sudden spikes in interest rate spreads.

It is natural to think of information flowing from the past to the present and from the present to the future. What happens today obviously impacts what will happen tomorrow. But expectations flow in the opposite direction. For example, current nominal interest rates are known to depend on two things: the real interest rate today, which is governed by people’s preferences and the economic resources available, and what inflation is expected to be in the future (figure 1). This dependence ties a government’s policy choices in the here and now to possible future outcomes through market expectations. Because expectations matter, it is critical that policymakers be mindful of how their actions shape market beliefs.

Sources: University of Michigan, Survey of consumers; U.S. Department of Labor, Bureau of Labor Statistics;

The subtle link backward from the future to the present and its impact on optimal policy have powerful implications for government. In a well-functioning democracy, no elected official’s position is guaranteed, and with each election cycle some new leaders are elected and some incumbents removed. In contrast, government policy is typically designed to be in effect for a long period, one that contains several elections. New policymakers may have the power to extensively alter or even completely undo the policies of their predecessors. Incumbents therefore cannot guarantee that the policies they create will be maintained by future governments.

If households and businesses cannot be certain that a policy will remain unchanged over its scheduled tenure, their response to the policy will adjust to reflect this uncertainty. As a consequence, the outcome policymakers intend to achieve may not be what occurs. Election turnover, a healthy feature of a democracy, creates a difficulty for policymaking because the current government cannot commit the future government to carry on its policies.

This Commentary discusses how the inability to commit to a policy alters market expectations, and how those expectations distort optimal policy. It also points out a general strategy for mitigating the negative effects arising from the inability to commit: specifically, combining policy rules with tough penalties for violating or amending those rules.

Commitment, Expectations, and Optimal Policy

In their Nobel-prize-winning paper, Finn Kydland and Ed Prescott showed how optimal policy crucially depends upon whether or not the policymaker can commit. When a policymaker can commit, households and businesses can rely on the policy remaining constant, which helps them make decisions about everything, like how much income to save or how many workers to hire. A government could, theoretically, factor in those decisions when it evaluates policy options.

In contrast, if a policymaker cannot convince households that it will abide by the policy it sets (that is, the government cannot commit) households and firms will form expectations about the way policy may change in the future. The decisions made based on those expectations are likely to alter the effectiveness of the original policy.

Unfortunately, it is generally not the case that a policymaker can commit. This is because optimal policy with commitment most often is time-inconsistent, meaning that at some point in the future the policy which was viewed as optimal when it was adopted in the past will not be considered optimal from the perspective of future policymakers. These future policymakers will be tempted to change the policy. If households recognize this temptation, they may assign some probability to policy being changed in the future. This means that their response to a policy announcement could be very different depending on how likely they believe it is that the policy will stay in effect.

For governments, the dilemma of time-inconsistency appears directly in the conduct of monetary and fiscal policy. Consider that the government’s budget is constrained by certain realities: For sources of revenue it has tax collections, new debt, and seigniorage (something like profit from issuing new money). Its expenditures include general spending for projects, transfers (promised payments to subsets of the population, as in social security), and the interest it owes on existing debt. To increase revenue, the government can raise taxes, create money (inflate), or, assuming that it does not default on its debt, issue new debt.

To see the time-inconsistency problem here, consider a democratically elected government. All else equal, officials have an incentive to provide more resources to their constituents through spending and transfers, but doing so requires financing. Of the three possible sources of revenue, taxation is probably the least desirable for the elected official. Voters tend to react negatively when their take-home pay shrinks (in the case of rising income taxes) or the after-tax price of goods at the grocery store rises (in the case of rising sales taxes).

History has shown that inflation is more attractive to politicians. If it takes time for people to disentangle growth from inflation, then voters will not immediately recognize the government’s action. Over time, however, they will become savvy to inflationary policy, and they will expect future inflation to be higher. This increase in inflation expectations raises the nominal interest rate and makes the government’s cost of debt service larger. Larger debt service means that the government will have an even greater need for financing, which increases the temptation to use inflation taxation again. Ultimately, that path leads to a suboptimal world characterized by very high inflation rates and high expected inflation.

Part of the Solution: An Independent Central Bank

Because of the temptation to inflate and the self-reinforcing nature of an inflation-based financing policy, governments have looked for ways to commit to not using it. This is the logic behind independent central banks. By handing the power to set monetary policy over to an independent central bank, the government can put a barrier between its temptation to inflate and its ability to do so.

Several studies have examined the effect of central bank independence on inflation. One widely-used measure of independence was designed by Cuckierman, Webb, and Neyapti (1992) and is based on four broad categories. These are the degree to which the head of the central bank is sheltered from the executive and legislative branches of government, the degree to which central banks have exclusive authority over monetary policy and influence over the budget process, the concentration of the central banks’ mandate on price stability, and the limitations placed on the central bank in regards to lending to the government. Using this measure, studies have found a positive, significant relationship between degrees of bank independence and inflation performance (see, for example, IMF 2008).

Because an independent central bank is charged with maintaining long-term economic targets, its policy focus extends beyond any election cycle. Because a significant fraction of the consequences from excessive inflationary policy are realized in the medium and long runs, a central bank should internalize more of the costs from inflating. This arrangement produces confidence within the market that an independent central bank will fight inflation, which keeps inflation expectations low and anchored and ensures that the government can borrow at affordable rates of interest. It is not surprising that most advanced economies have independent central banks.

Although an independent central bank does seem to effectively tie the hands of the government with respect to monetary policy, it does not cover fiscal policy, as it does not force current officials to fully internalize the costs of their spending decisions. Tax increases can still be avoided in the short run by borrowing more. To be sure, the interest that will have to be paid on new debt must be balanced at some date with additional tax revenue, but it is quite possible that other officials will be in office when that time comes. This gives the current sitting government a free lunch.

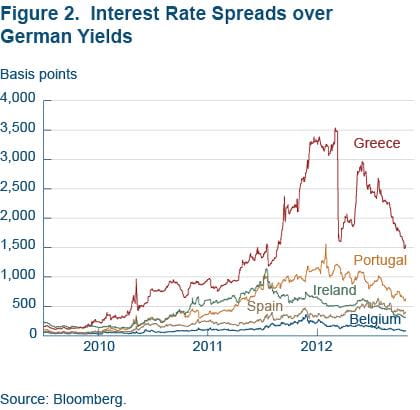

That said, the terms that the government receives on its new debt will depend in part upon how the market perceives the risk of default. When this risk is deemed to be low (as it normally is), government debt provides a near risk-free return, so the market requires a low rate of interest. However, if additional expenditure is continually financed with more new debt, at some critical point, the ability to make payments on maturing debt may be questioned. When this occurs, it produces sharp change in the terms of credit for new debt issues, as we witnessed in Greece recently (figure 2).

Sources: Bloomberg.

History has shown that in countries lacking a strong, independent central bank, the government may succumb to the temptation to devalue outstanding debt through rapid inflation; however, when the central bank is independent, the government must either raise taxes or default when it cannot service its debt with current revenues. The danger is that for many advanced countries the “day of reckoning,“ when markets begin to penalize governments for excessive debt burdens, may come far in the future when the policies which have produced the high debt are strongly entrenched politically. Equally unsettling, these days of reckoning are likely to come during a downturn, when real economic activity is depressed, making tax rate increases even more painful. Worse still, those tax rate increases are less effective at raising new revenue because the taxable base is low in recessions.

Fiscal Rules

Given what we know about the effectiveness of independent central banks at keeping inflation expectations reigned in, it is natural to wonder whether the same result could be achieved for other forms of financing. Could restricting the degree to which new spending can be financed with debt place more of the cost of incurring new debt on the government that enacts the policies?

The solution could come in several forms. The simplest type of solution along these lines would be a financing rule, like an expenditure rule or a balanced budget amendment. Both of these have been implemented in the past with some success. In the 1990s the U.S. Congress capped spending and tied expenditure changes to revenue changes. By adhering to these rules, Congress was able to transform above-average revenues from the combination of the 1992 tax reform and technological growth into budget surpluses.

Nearly all U.S. states have enshrined balanced budget rules into their constitutions. These rules require states not to run an operating deficit over a short window (usually one or two years). While balanced budget amendments can be effective for preventing run ups in state debts, they only tie the hands of incumbent governments to an extent. Often there are loopholes which exempt some expenditure categories from counting against the operating budget (and thus must be balanced by revenues). Also a balanced budget amendment is only as reliable as it is difficult to amend the state constitution. In some cases, it is very difficult, requiring both legislative action and popular votes. In others, the rule can be undone by a simple majority of state voters.

In Practice

The key to making rules work is to make violating the commitment very costly. Without meaningful penalties to give rules force, governments can ignore rules. In addition, penalties should be enforced from outside the government, for example by the market. Independent central banks satisfy this criterion because they act as a signal to the market of the government’s stance on inflationary monetary policy.

If a government interferes too strongly with its central bank, markets become nervous about future inflation and move quickly to demand more compensation (that is, inflation risk premium). Over time, an independent central bank amasses credibility for keeping inflation low. This anchors the market’s inflation expectations so that the government can borrow at lower nominal interest rates. Under this environment, political interference comes at the additional cost of lost reputation for the central bank. Even if central bank independence is restored, it may take many years to rebuild reputation and bring inflation expectations, and government borrowing costs, back down.

Whatever rule a government adopts, it is important that the rule have just the right amount of flexibility. If the rule is too rigid, then there will be more temptation to break it in times of stress. If it is too flexible, then the rule can be circumvented, and it will fail to inspire market confidence. A good rule must allow for fiscal action in extraordinary circumstances (like the recent recession or a war) and provide a channel for possibly swift action. At the same time, it must force the current government to internalize the costs of today’s actions on future generations and maintain a long-run perspective. Ultimately, it is up to voters to strike the balance most desirable to them.

Works Referenced

- “Central Bank Independence and Transparency: Evolution and Effectiveness,” Chris Crowe and Ellen E. Meade, 2008. International Monetary Fund, working paper no. 08/119.

- “Rules Rather than Discretion: The Inconsistency of Optimal Plans,” Finn Kydland and Edward C. Prescott, 1977. Journal of Political Economy, vol. 85, no. 3.

- “Presidents, Governors, and the FOMC: Regional Bank Leaders Provide Long-term Stability,” Tim Todd, 2009. Federal Reserve Bank of Kansas City, TEN.

Suggested Citation

Carroll, Daniel R. 2012. “Time-Consistent Rules in Monetary and Fiscal Policy.” Federal Reserve Bank of Cleveland, Economic Commentary 2012-19. https://doi.org/10.26509/frbc-ec-201219

This work by Federal Reserve Bank of Cleveland is licensed under Creative Commons Attribution-NonCommercial 4.0 International