- Share

Exchange-Traded Funds

ETFs are one of the most successful financial innovations of the last few decades. As a new, rapidly growing, and increasingly complex financial instrument, ETFs might raise concerns about the risk they pose to financial stability. While they do not seem to pose a threat at this time, ETFs did expose a weakness in U.S. stock markets during the Flash Crash of 2010: the fragmented nature of trading, which can leave some markets very shallow.

The views authors express in Economic Commentary are theirs and not necessarily those of the Federal Reserve Bank of Cleveland or the Board of Governors of the Federal Reserve System. The series editor is Tasia Hane. This paper and its data are subject to revision; please visit clevelandfed.org for updates.

With the spectacular boom and bust of mortgage-backed financial products still fresh in our collective memory, any rapidly growing asset class is bound to raise eyebrows in the marketplace. The exchange-traded fund (ETF) is one such product.

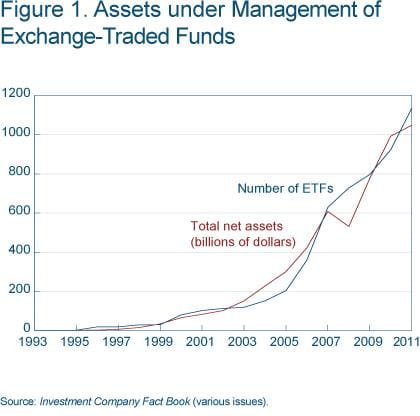

ETFs are stock-market-traded entities that invest mostly in corporate and sovereign financial liabilities, often with the intention of replicating the returns of a market index, like the S&P 500. That goal may not sound glamorous, but ETFs are one of the most successful financial innovations of the last few decades. Their growth has been phenomenal, especially since 2005 (figure 1). While small relative to their older cousin, mutual funds (which control about $7.5 trillion in assets), ETFs have gone from $0 to $1 trillion in just 20 years.

We explore what makes ETFs successful, especially in comparison with mutual funds, and whether this rapidly growing financial instrument poses a risk to the stability of the financial system.

From TIPs to SPDRs and Beyond

ETFs may be new and complex financial instruments, but they are quite similar to the simple warehouse receipts of goldsmiths at the dawn of banking. Goldsmiths had safe storage facilities, and people realized that it cost less to leave their coins with the goldsmiths than to keep them safe in their homes. In return, goldsmiths gave coin owners a warehouse receipt, which allowed them to withdraw their coins on demand. As confidence in the goldsmiths grew, the receipts became a surrogate for the gold coins. Over time, some goldsmiths began making loans by lending out receipts (not gold). Thus, there were two receipts against the same amount of gold, one in the hand of the original depositor and the second in the hand of the borrower. This practice allowed goldsmiths to collect interest on the gold in their storage rooms.

Fast forward a few millennia to 1990. Substitute the goldsmith with a trustee, the cost of theft with transaction costs, and the gold coins with shares of stock in Toronto’s TSE-35 index, and you have the makings of the first ETF. In place of the warehouse receipts there are Toronto Stock Exchange Index Participations (TIPs). Just like the goldsmiths’ receipts, TIPs could be redeemed at any time for the underlying asset, in this case, stocks in the index, or they could be created once the asset had been deposited with the trustee. And in the same way that goldsmith receipts could serve in the place of coins for everyday transactions, TIPs were also very liquid and could be bought and sold in the market at any time, just like the index stocks in the portfolio they were a claim on. If the TIP had increased in value, investors made a profit, and if it fell, they lost money.

Overall, TIPs were a low-cost way for investors to hold the portfolio because the trustee could lend out the stocks in storage for a fee and thus earn income from the holdings and make up for some of the costs. In other words, just like the goldsmith who made money from lending out the gold in storage, the trustee’s income came not just from charging for security storage but also from the security-lending side business.

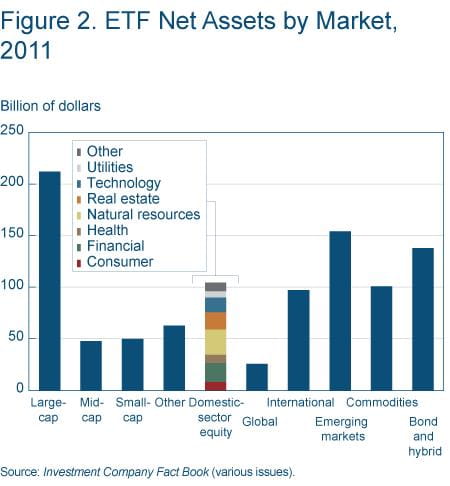

The ETF concept was implemented in the United States in 1993 with the development of SPDRs (pronounced “spiders”). SPDRs were created by the American Stock Exchange to hold the S&P 500 portfolio. Over time, ETFs began to proliferate, and as they did, the diversity of the sectors and markets that they covered expanded remarkably. It is currently possible to invest through ETFs in any major sector of the economy and in developed and emerging stock and bond markets across the globe (figure 2).

Why ETFs When There Are Mutual Funds?

Mutual funds and ETFs are similar in concept, and they offer investors many of the same advantages. But one difference between them has a lot to do with the growing popularity of ETFs.

Like ETFs, mutual funds are a form of financial intermediation that arose to lower the transaction costs of holding a portfolio of financial assets. Mutual funds are investment companies that invest exclusively in a particular set of financial assets or a mixture of assets, depending on their stated investment objectives (such as meeting or exceeding the returns on the stock index of an industry, a broad market index, the price index of a commodity, etc.). A share in a mutual fund represents a claim on the cash flows from the assets in the portfolio.

Mutual funds come in two types: closed-end and open-end.

Closed-end funds have a fixed number of shares. All trading in the shares of these funds occurs in the stock exchanges, meaning that someone who wishes to invest in the fund has to find a willing seller of the fund’s shares. Conversely, sellers have to find willing buyers. If demand for the fund’s shares is high, sellers may require a premium above and beyond the value of the assets of the fund (called net asset value or NAV). If demand is waning, sellers may have to accept a discount relative to NAV. Because transactions in the shares of closed-end funds may occur at a price that deviates from the fund’s NAV, investor returns on closed-end mutual-fund shares do not always match the return on the underlying assets.

Open-end funds do not have a fixed number of shares, and there is no secondary market trading. A prospective buyer who wishes to invest in the fund pays cash to the fund manager, and the manager uses the cash to buy more of the assets in the fund portfolio in the proportions of the existing holdings. Alternatively, if an existing investor wishes to exit, the fund manager sells some of the assets and pays off the investor.

The advantage of an open-end fund is that there is never a price premium or discount associated with the fund shares, since they can be created and redeemed any time. But there are a couple of disadvantages.

First, both the creation and redemption of open-end mutual-fund shares involve transaction costs, since assets must be purchased for and sold from the portfolio. Moreover, the asset sales needed for redemption may create capital gains and a tax liability for the remaining investors. Tax liability is not an issue for closed-end funds, because they do not involve redemption.

To minimize the additional transaction costs, the open-end-fund manager typically does two things, both of which can have unwanted side effects. He keeps some cash and other liquid funds on the side to meet requests for redemption (sparing him from selling assets). The downside to that strategy is that the fund has to invest less in the assets it targets and more in liquid assets and cash. The manager can also invest in the relatively few large components of a market index while leaving out the numerous smaller components; this saves the fund money in transaction costs at the expense of tracking accuracy.

ETFs arose to address all the weaknesses and capture all the benefits of both types of mutual funds. Just like closed-end funds, they trade in the markets continuously, and just like open-end funds, they can be created and redeemed at any time by investors. Only “authorized participants,” large institutional investors who have an agreement with the fund sponsor, can create shares, typically in 50,000 share lots. Redemptions are also done in batches of a fixed number of shares.

But the one major difference that sets ETFs a world apart from mutual funds is that both the creation and redemption of shares are in-kind, not cash. That is, the authorized participant has to bring a scaled replica of the ETF’s portfolio to receive the corresponding number of shares. At redemption, the participant is again paid in the assets of the portfolio.

In-kind transactions provide three advantages to ETF investors over mutual funds. First, transaction costs are minimal since the fund manager does not have to engage in market trades to acquire or redeem shares. Second, because no asset sales take place, there is no taxable event. And third, the fund manager can choose the shares with the lowest cost basis in the portfolio for redemption. For example, let’s assume that the stock of a particular company was acquired at $1, $2, and $3 in three separate trades. The current price is $4. The shares that were bought at $1 would create the highest capital gains tax liability if they were sold to rebalance the portfolio. However, if there is a redemption request, the fund manager can meet the request with the $1 shares, raising the cost basis of the shares remaining in the portfolio. If there is a need to rebalance the portfolio thereafter, the capital gains tax liability of the remaining shareholders would be less.

Thus, ETFs dominate open-end mutual funds because the fund manager does not have to keep cash on hand to meet redemption requests and because the shareholders do not suffer from taxes and transaction costs arising from other investors’ trading.

The advantages of ETFs over closed-end funds are related to the latter’s inability to get a match between the returns on the NAV and the fund returns. An investor who would like to gain exposure to a portfolio of technology companies, for example, may find out that the performance of the closed-end fund he invested in sorely trails the returns on the stocks of technology companies the fund is invested in because the fund is trading at a discount.

The reason for this mismatch is a lack of arbitrage opportunities. Speculators are unable to close the gap between the underlying value of the mutual fund and the price it is trading at; price no longer reflects value. If an ETF were to sell at a discount relative to NAV, speculators could come in, buy the ETF, redeem the shares for the underlying assets, and sell the assets in the market. The discount would be the speculator’s risk-free profit. Over time, this type of trade would drive the price of the ETF up and the price of the underlying assets down. The trouble with closed-end funds is that in-kind redemptions, which make the arbitrage trade feasible, are either not allowed or are severely restricted. Therefore, for short-term investors who really care about tracking the underlying fund portfolio accurately, ETFs may be the way to go.

Is There a Catch?

The rapid proliferation of ETFs is proof positive that investors value their advantages. Yet there is growing concern that the fast growth is a harbinger of instability.

A recent disturbance in the stock market showed how ETFs can potentially cause contagion across markets. On May 6, 2010, the Dow Jones industrial average dropped 998.5 points and recovered 600 points within 20 minutes—an event now remembered as the Flash Crash of 2010. The event started in the e-mini futures markets in Chicago when a trading algorithm ran amok. The crash may have been short and caused by a mere technical glitch, but the losses were heavy and very real.

The glitch first caused heavy losses in the futures market, which set off a wave of arbitrage activity in that market and then spilled over into the ETF market. Futures prices essentially reflect where asset prices are expected to go in the future. When investors saw the fall in futures prices, they judged it unreasonably low and began to arbitrage. They bought futures contracts and limited their exposure by shorting the underlying stocks in the spot market.

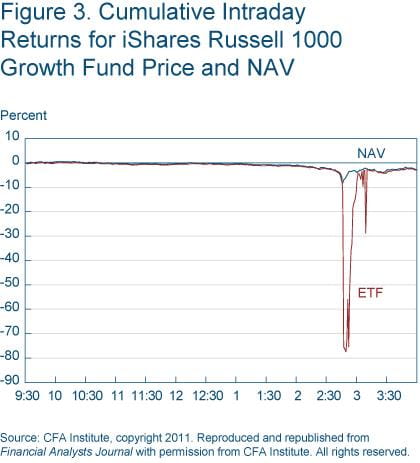

But with index futures, there are many stocks to be shorted, so investors followed the cost-effective strategy of shorting the ETF that tracked the underlying index. When they did that, the ETF prices became too low relative to the value of the portfolio, creating more opportunities for arbitrage. Investors bought shares in the ETF, redeemed them, and sold the underlying assets. The discount between the ETF price and NAV was closed, but stock prices began to drop as a result of the selling. Figure 3 shows the minute-by-minute evolution of the returns on one ETF, the iShares Russell 1000 Growth Fund, and its NAV on May 6.

During the flash crash, the price of the ETF cratered by almost 80 percent. By the time the link between the ETF price and its NAV finally broke, the NAV was down close to 10 percent. Research using tick-by-tick trading data suggests that the troubles of the futures market spilled over to the broad stock market through the ETF link. In the absence of ETFs, the transaction costs might have limited the arbitrage opportunities and slowed the spread of the wildfire from the futures market to the spot market.

Does this link make ETFs a threat to financial stability or just the canary for weak spots in market liquidity? Recent research suggests that policymakers should not shoot the messenger. The weakness that led to the Flash Crash may be the fragmented nature of trading in the U.S. stock markets, not the design of ETFs. The NASDAQ carries 23.8 percent of the equity dollar volume, the NYSE Arca 16.5 percent, the NYSE 12.6 percent, BATS 11.9 percent, Direct Edge-X 8.1 percent, and other exchanges and trading mechanisms carry the remainder.

The consequence of this fragmentation is that some markets can be extremely shallow; that is, they are unable to absorb sizeable orders without significant price effects. If orders are routed to these shallow markets during trade disruptions, the disturbance is likely to be magnified. What is needed then might be clear guidelines for trade routing and rules to curb extreme volatility.

Such rule changes are not put in place overnight, as each tweak to the existing rules brings along its own potential problems and has to be debated and negotiated among the regulators and market participants. But if we have a more sound market structure in place before the next shock hits, we may thank the exchange-traded funds for bringing this weakness to light.

Leverage: An Old Foe

While all may seem clear on the ETF front, this is not the time to drop all defenses. As recent experience shows, successful financial products tend to get increasingly more complex over time. While plain ETFs, like the ones we described here, are the most widely held securities, it is also possible to buy funds that invest in a third-party’s promise to deliver an asset or a stream of cash flows rather than the actual asset itself.

These synthetic products introduce counterparty risk—the risk that the third party won’t or won’t be able to honor its obligations—which is not an issue for plain vanilla ETFs. Because synthetic securities are not backed by the actual asset, they can be created in unlimited amounts, potentially creating exposures much larger than the underlying asset market. For additional flavor, investors can spice up their expected returns by investing in ETFs that augment the gains from the underlying assets using leverage—investing with borrowed funds. Unfortunately, as the failures of Bear Stearns and Lehman Brothers have shown, leveraging also magnifies the losses.

There is no indication that the use of synthetic and leveraged ETFs will reach levels that could threaten financial stability any time soon. We continue to believe that very important lessons about investing have been learned in the last five years, and those lessons will keep a cap on investors’ risk appetites. Still, regulators will be staying alert, just in case.

Recommended Reading

- “ETFs, Arbitrage, and Contagion,” by Itzhak Ben-David, Francesco Franzoni, and Rabih Moussawi. 2011. Ohio State University, Dice Center working paper no. 2011-20.

- The Exchange-Traded Funds Manual, by Gary L. Gastineau, 2010. John Wiley & Sons, Inc.: Hoboken, New Jersey.

- “Exchange-Traded Funds, Market Structure, and the Flash Crash,” by Ananth Madhavan, forthcoming in Financial Analyst Journal.

- “Findings Regarding the Market Events of May 6, 2010: Report of the Staffs of CFTC and SEC to the Joint Advisory Committee on Emerging Regulatory Issues,” by the U.S. Commodity Futures Trading Commission and the U.S. Securities and Exchange Commission, September 30, 2010.

Suggested Citation

Ergungor, O. Emre. 2012. “Exchange-Traded Funds.” Federal Reserve Bank of Cleveland, Economic Commentary 2012-05. https://doi.org/10.26509/frbc-ec-201205

This work by Federal Reserve Bank of Cleveland is licensed under Creative Commons Attribution-NonCommercial 4.0 International