- Share

Recession Probabilities

Statistical models that estimate 12-month-ahead recession probabilities using the term spread have been around for many years. However, the reliability of the term spread as a predictor may have been affected by short-term interest rates being at zero. At the zero lower bound, long-term yields cannot go too far into negative territory due to the portfolio constraints of institutional investors. Therefore, the yield curve may not invert when it should or as much as it should despite the anticipated path of the economy. I enhance the simple model with two variables that should have predictive power for recessions.

The views authors express in Economic Commentary are theirs and not necessarily those of the Federal Reserve Bank of Cleveland or the Board of Governors of the Federal Reserve System. The series editor is Tasia Hane. This paper and its data are subject to revision; please visit clevelandfed.org for updates.

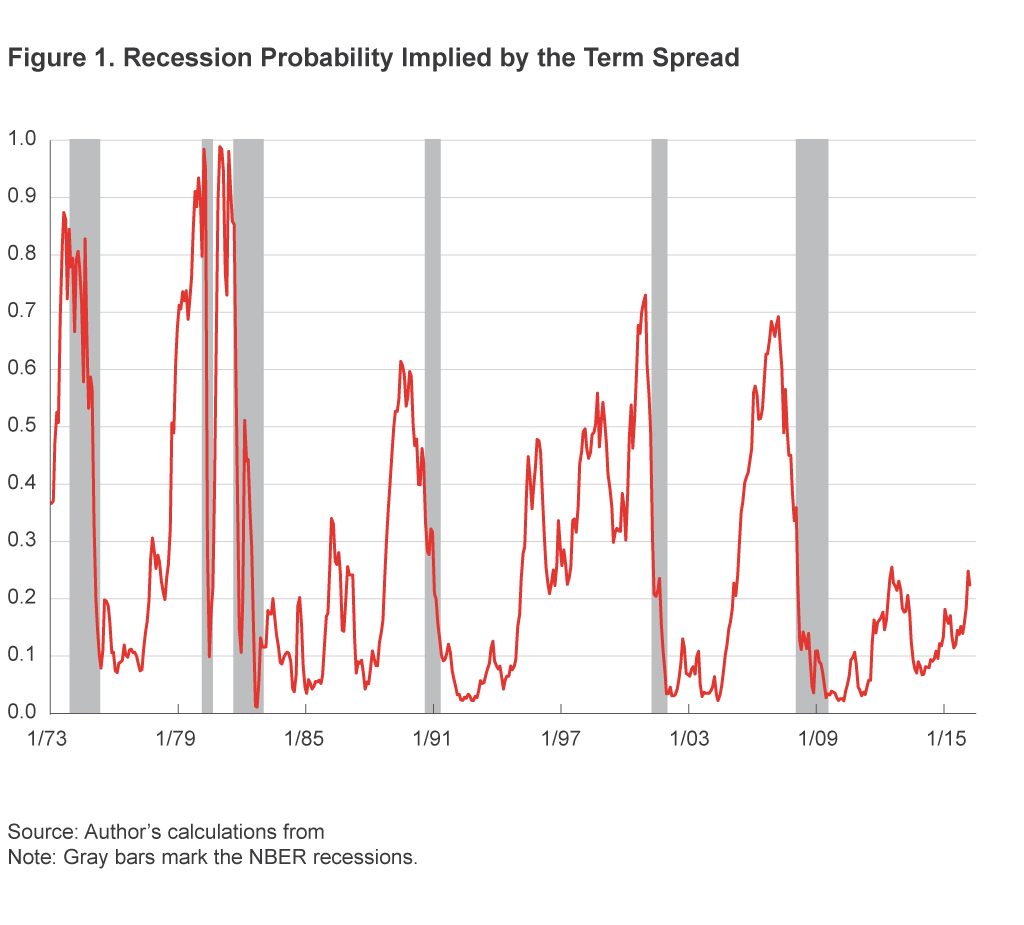

With the eagerness of alchemists looking for the universal elixir, business economists have forever been looking for economic or financial variables that can predict future economic activity. Unlike the medieval protoscientists, the intuition of the business economists seems vindicated. Wenow have nearly 30 years of meticulous research that shows that such variables do exist in the fixed-income market. In particular, the difference between long- and short-maturity Treasury yields (the term spread) produces intriguingly accurate predictions of economic activity and recessions in the United States and abroad (figure 1).1 Furthermore, credit spreads—the difference between the yields of high- and low-quality bonds—are known to have predictive power.2

In recent years, the fact that high-quality bond yields have been very close to zero may be hurting the predictive power of fixed-income spreads. When short-term Treasury yields are at zero, the long-maturity yields would have to go deep into negative-yield territory to create the same level of negative term spreads we have observed in the past before recessions. However, such negative long-term yields are more difficult to generate in the financial markets than “low” but positive long-term yields. Most importantly, negative yields cut into the demand for safe bonds from traditional long-term institutional investors, such as insurance companies and pension funds. These investors have nominal future liabilities and must generate positive returns on their investments to be able to meet those obligations. By the same token, demand for bond mutual funds is reduced, as their customers can always keep their money in a vault and earn zero interest. In other words, the yield curve may not invert at the zero lower bound despite the anticipated path of economic activity because the declining investor demand will prevent yields from falling too far.

In this Economic Commentary, I explain why fixed-income spreads have worked so well as a predictor of economic activity in the past and discuss the economic merit of an enhanced measure that reduces our reliance on the fixed-income markets. This new measure includes the growth in corporate profits.

The Term Spread

According to the market expectations hypothesis, the long-maturity end of the observed yield curve reflects investors’ expectations of future short-term rates. Intuitively, an investor who is interested in a two-year investment compares the current two-year bond yields to how much she expects to earn if she invests in a one-year bond and then rolls that investment over into another one-year bond next year when the first bond matures. The market yields will be in equilibrium when the marginal investor is indifferent between the two options. Thus, the current two-year yield reflects the current one-year yield and the expected one-year yield one year from now.

Admittedly, long-maturity yields reflect more than just future short-maturity yields, but this limited description is sufficient for our purposes. But given what they do reflect, an upward-sloping yield curve then represents investors’ expectation that short-term money will cost more in the future. Yield curves with steep slopes are observed during recessions because, while investment opportunities may be limited in the near term, recessions always end. When they do, investment opportunities abound and the cost of credit reflects these growth opportunities. Conversely, if the yield curve is flattening or sloping downward (negative term spread), investors are essentially predicting a decline in investment opportunities and an economic slowdown.

The Credit Spread

While the term spread considers the yield differential between long- and short-maturity securities of the same borrower, the credit spread keeps the maturity constant but considers borrowers of different creditworthiness: namely, the highest-quality (Aaa) and lower-quality (Baa) corporate borrowers.3 At first glance, its construction suggests that the credit spread captures the market expectations of default risk in the corporate bond market. When market expectations of default (thus, the spread) rise, this is predictive of an upcoming slowdown or recession.

However, recent research by Gilchrist and Zakrajšek suggests that this traditional story may be intuitive but it might also be misleading. The credit spread, they argue, has two components. The first is sensitive to expected defaults, as in the traditional story. Practically speaking, one can take historical credit spreads and determine how sensitive they have been to the level of a theoretical estimate of expected default at each point in time.4 Then, one can take the default expectation as of today and use the historical sensitivity to estimate the portion of the observed spread that is related to the expected default risk; this is the first component (ED).

The second component is the remainder after one subtracts the first component from the total spread. This is the piece whose variations cannot be explained by the changes in default expectations. It is interpreted as investor sentiment or the willingness of fixed-income investors to extend credit. It captures how much extra yield a borrower with constant default risk needs to pay to convince an investor to hold her bond at that point in time. It is this second component that has predictive power for future economic activity, not the first. Gilchrist and Zakrajšek call this measure of sentiment the excess bond premium (EBP). If investors are requiring higher compensation for holding bonds whose default risk has not changed, the sentiment may be turning negative and a slowdown in economic activity may be more likely.

A statistical model that includes the term spread and the credit spread has greater accuracy when predicting recessions 12 months ahead relative to a model that includes only the term spread. However, the explanatory power of the credit spread comes from its EBP component, not the ED component.

This being said, the credit spread is afflicted by the same concerns that affect the term spread. It is a measure taken from the fixed-income markets. As such, the high quality (Aaa corporate or US Treasury) yields are subject to the same zero-lower-bound problem described in the introduction (at which point, cash becomes more attractive than holding the bond if we ignore the cost of storing the actual banknotes). Furthermore, in areas like Europe, where the central bank is buying the investment-grade corporate bonds, the yields and spreads may no longer reflect market sentiment toward credit risk but expectations about central bank behavior.

Corporate Profits

Given concerns over the stability of the predictive power of the term and credit spreads, I turn my attention to other financial measures that lack the forward-looking nature of the financial market data but should still have predictive power for future economic activity.

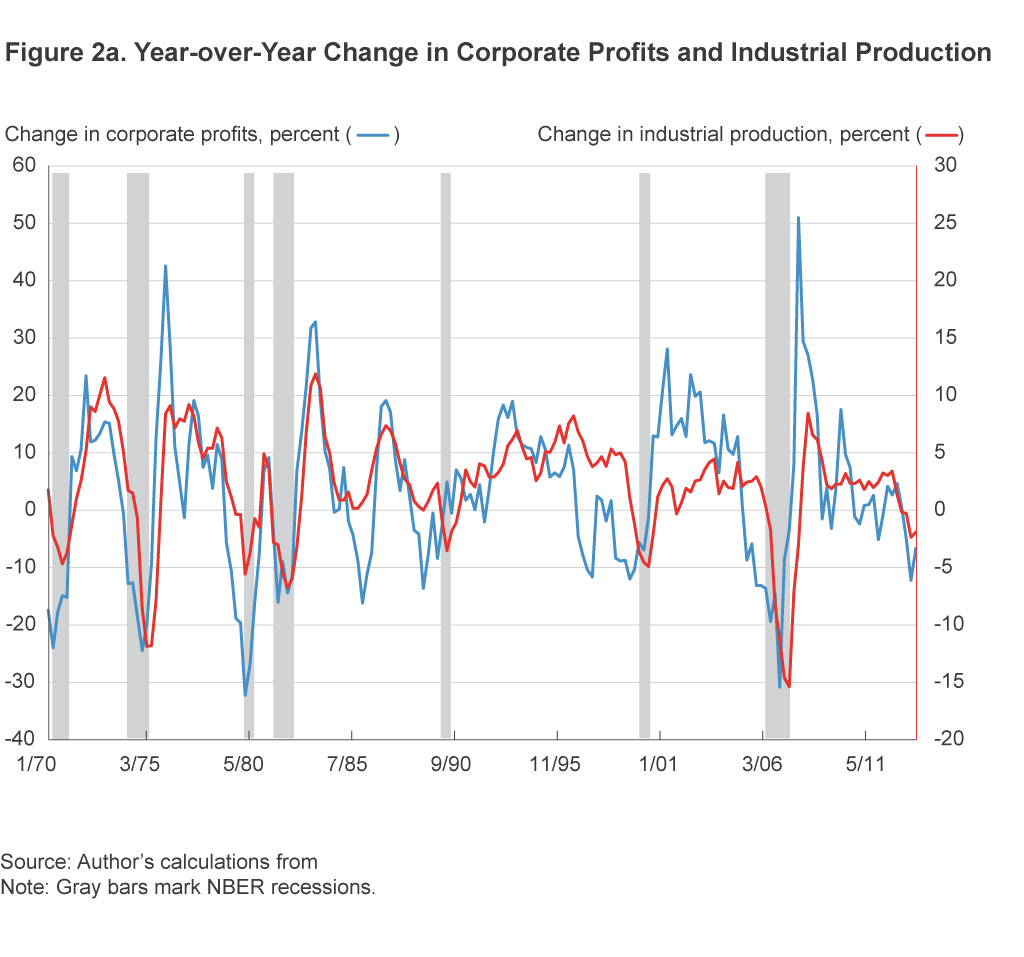

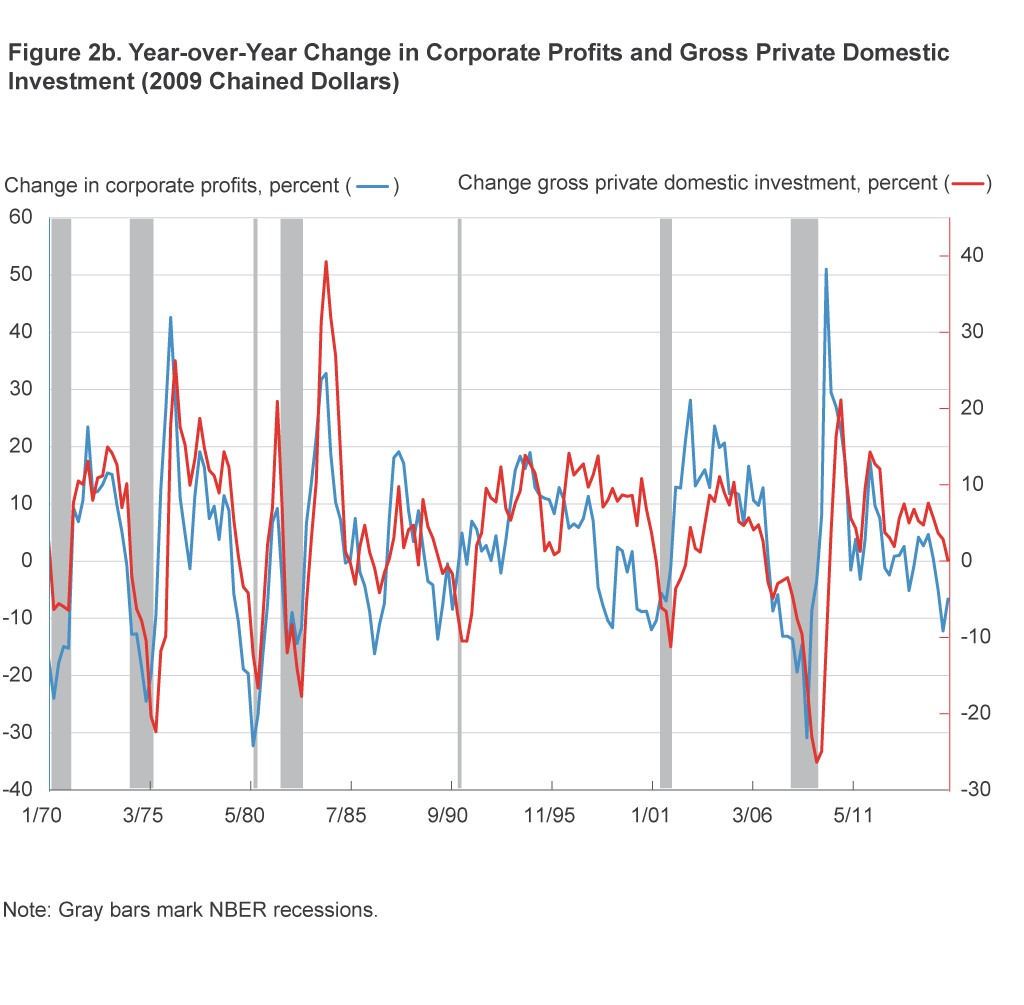

The measure I propose is the inflation-adjusted quarterly change in pre-tax corporate profits.5 Intuitively, a change in corporate profits should be highly correlated with industrial production and investment. One would expect firms to produce and invest more if their profits are rising. The empirical question in this analysis is which comes first: the change in profits or production and investment?

Using quarterly data since 1970, figures 2a and 2b show the three data series, but to improve the exposition of the relationship, I plot year-over-year changes rather than quarterly changes. A simple correlation analysis shows that the correlation between the change in corporate profits and the contemporaneous change in industrial production is 54 percent, but the correlation goes up to 66 percent if I use the one-quarter-ahead change in industrial production. Similarly, the correlation between the change in corporate profits and the contemporaneous change in gross domestic private investment is 57 percent, but the correlation goes up to 68 percent if I use the one-quarter-ahead change in investment. More formally, a Granger causality test indicates that the quarterly change in profits leads the quarterly change in production by one quarter, but the change in profits is independent of the change in production. A similar relationship applies to the quarterly change in profits and investment.6 Thus, firms seem to adjust their production and investment after seeing a drop in their profits.

There may be many reasons why corporate profits lead economic activity. For example, a drop in demand may hurt profits, but production and investment would continue for some time to run down raw-material inventories or to complete investment projects that are in the final stages of implementation. In the financial industry, trading profits or loan originations would drop before institutions take drastic measures, such as halting new office construction, closing offices, or cutting employment. An institution would need to make sure that the drop in activity is not temporary because capacity adjustments, such as laying off workers and mothballing factories, are costly.

A second narrative might be that as the economy reaches full employment and labor costs begin to rise, corporate profits would weaken. With profits and cash flows under pressure, firms would have more difficulty justifying their investment and hiring plans to their shareholders. The resulting decline in investment and spending would lead to a slowdown and have further knock-on effects on profits. Unfortunately, the current analysis is not designed to distinguish between various alternative explanations.

Estimation Technique

In this section, I describe the statistical technique used in estimating the likelihood of a recession in the next 12 months. The reader who is impartial to the estimation details can skip to the next section.

I use a probit model, which includes the term spread (TS), the component of the credit spread tied to expected defaults (ED), the excess bond premium component (EBP), the quarterly change in the S&P 500 total return index (SNP), and the quarterly change in inflation-adjusted pre-tax corporate profits with inventory and capital consumption adjustments (PR). The dataset spans the months between January 1973 and March 2016, matching the availability of the credit spread data.7 Summary statistics of these variables are in table 1.

|

|

Mean (percent) |

Standard deviation | Minimum (percent) | Maximum (percent) |

|---|---|---|---|---|

| PR | 0.72 | 5.16 | −21.86 | 22.51 |

| EBP | 0.04 | 0.51 | −1.19 | 2.91 |

| TS | 1.58 | 1.38 | −3.51 | 4.15 |

| SNP | 8.36 | 16.54 | −42.51 | 52.64 |

| ED | 1.73 | 0.73 | 0.59 | 5.49 |

N= 519.

The dependent variable, NBERt,t+12, equals one if there is an NBER recession starting at any time in the 12 months that follow the observed independent variables, and zero otherwise. I assume that whether we are in a recession or not is unknown in the current month and the five months prior because of the delay in NBER recession announcements. Since NBERt,t+12 needs 12 months of forward-looking observations of recessions, the estimation ends in September 2014 but the forecasts continue until March 2016.

While the coefficients from a standard probit estimation will be unbiased, the serial correlation in the dependent variable will cause the standard errors to be too small. The standard errors I report later in this analysis are the errors obtained after applying the Newey-West correction.

Table 2 shows the average marginal effects from the analysis. A one-standard-deviation decline in real corporate profits (5.2 percentage points) increases the probability of a recession in the following 12 months by 5.5 percentage points (model 3). A one-standard-deviation decline in the term spread (1.29 percentage points) increases the probability of a recession by 15.4 percentage points. All these estimates are statistically and economically meaningful. There is also very strong evidence that model 3 provides a better fit to the data than model 4 based on the Bayesian information criterion (BID).

| Model 1 | Model 2 | Model 3 | Model 4 | |

|---|---|---|---|---|

| PR | −0.0301*** | −0.0110*** | −0.0103*** | |

| (0.0080) | (0.0039) | (0.0037) | ||

| EBP | 0.2903*** | 0.1959*** | 0.2148*** | |

| (0.0461) | (0.0398) | (0.0445) | ||

| TS | −0.1199*** | −0.1154*** | −0.1318*** | |

| (0.0171) | (0.0175) | (0.0193) | ||

| SNP | −0.0056*** | −0.0058*** | ||

| (0.0013) | (0.0013) | |||

| ED | −0.0463 | −0.0539 | ||

| (0.0418) | (0.0447) | |||

| BIC | −2584 | −2818 | −2848 | −2836 |

| Pseudo-R2 | 0.22 | 0.73 | 0.80 | 0.78 |

Notes: The Newey-West standard errors are in parentheses. The pseudo R2 is computed according to McKelvey and Zavoina. *** indicates p is less than 0.01; * indicates p is less than 0.10. BIC is the Bayesian information criterion.

Results

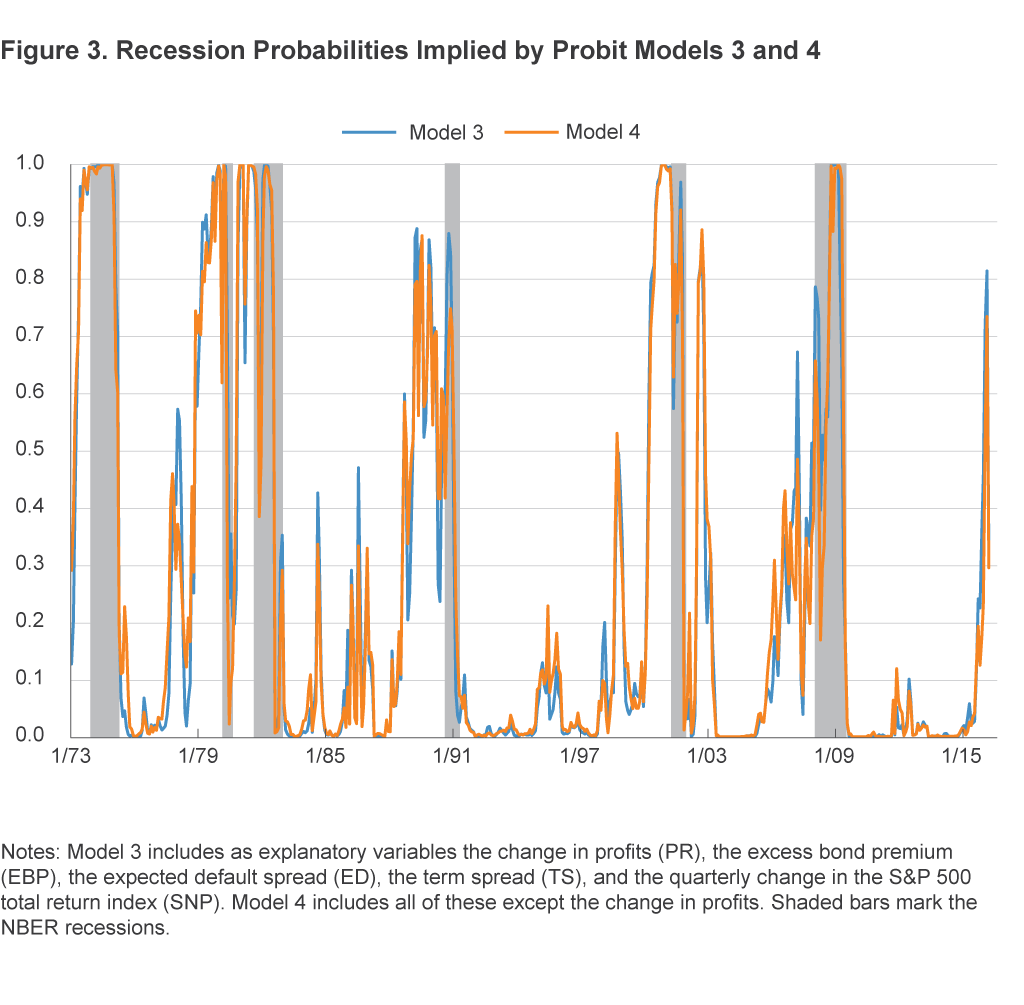

The estimated recession probabilities using a model that includes the change in profits (PR) as an explanatory variable (model 3) and a model that excludes it (model 4) are shown in figure 3. The comparison allows me to discern what corporate profits add to the explanatory power of some commonly used predictive measures, such as the term spread (TS), the expected default spread (ED), the excess bond premium (EBP), and the quarterly change in the S&P 500 total return index (SNP).

In early 2016, model 3 assigned an 81 percent probability to a recession in the next 12 months, and model 4 assigned a 73 percent probability to the same event. Thus, the consideration of the decline in corporate profits in this period worsened the recession probability by 8 percentage points. As credit spreads declined later in the period, the recession probabilities from both models declined to around 30 percent.

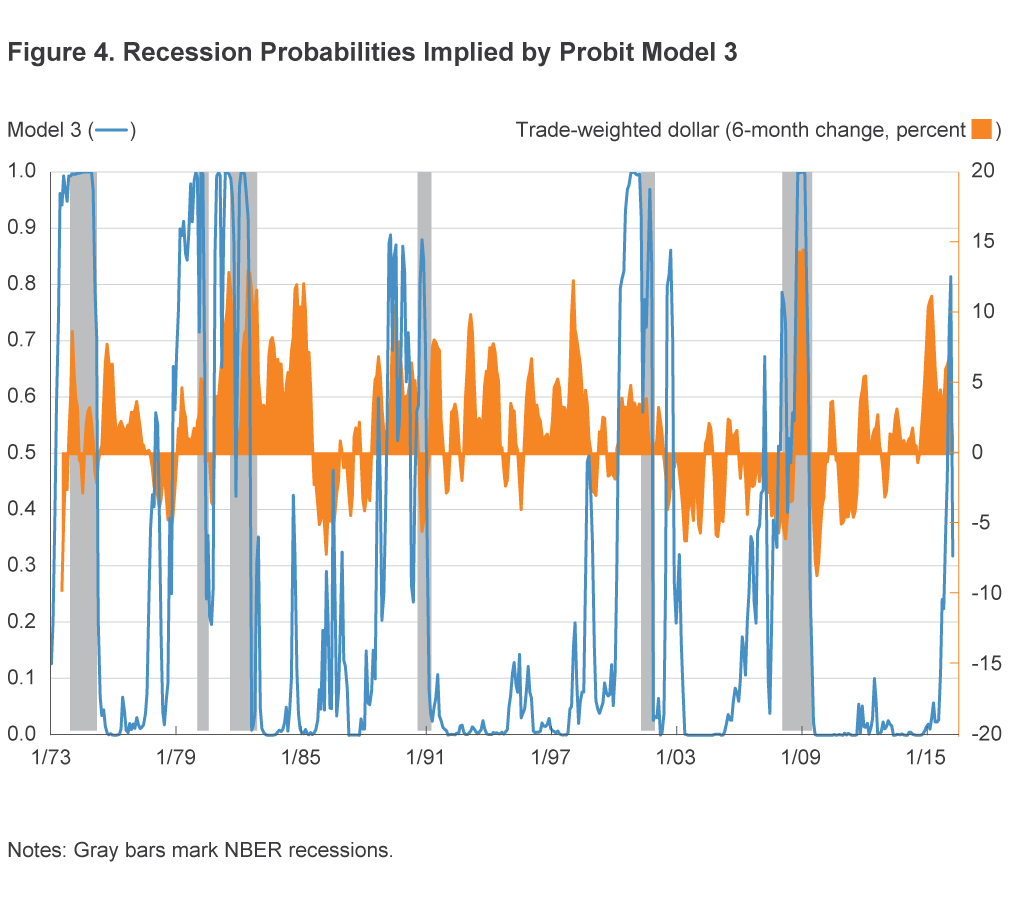

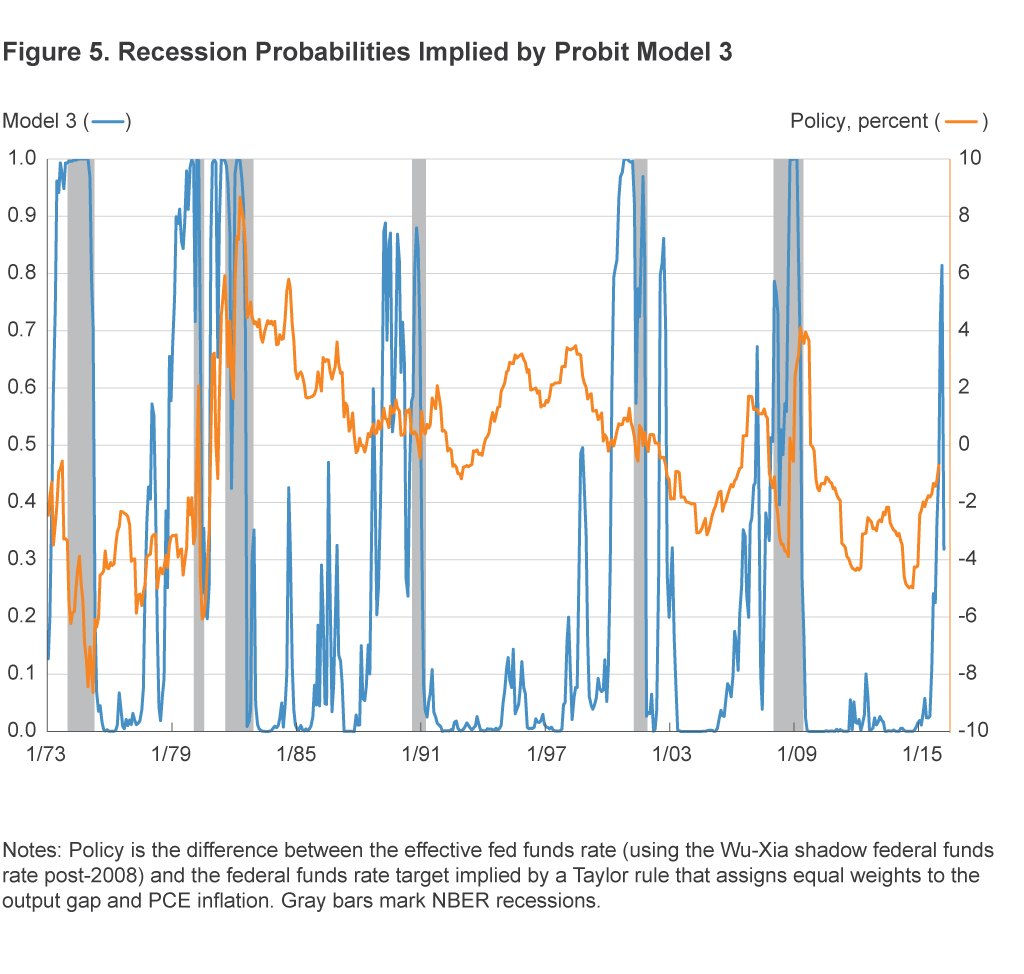

While these probabilities are high, note that both models also give noteworthy false positives in 1984, 1986, 1998, and 2002 by predicting recessions that never came to pass. The peak of model 3 in the first two episodes, when it exacerbates the false positive by 9 to 14 percentage points, follows extended periods of strength in the US dollar (figure 4) and corresponds precisely to the end of monetary policy tightening cycles, which are followed by a nearly 4 percentage point easing of the federal funds rate (figure 5).8,9 The 1998 episode corresponds to the flattening of the yield curve (declining term spread) after the Russian default. The 2002 episode is driven almost entirely by widening credit spreads in the aftermath of the accounting scandals. It is not associated with a period of strength in the US dollar as shown in figure 4 or the term spread (figure 1). Positive profit growth in this period actually pulls the recession probability down, but it cannot overcome the impact of the sharp widening of the credit spreads.

Real-time Effects

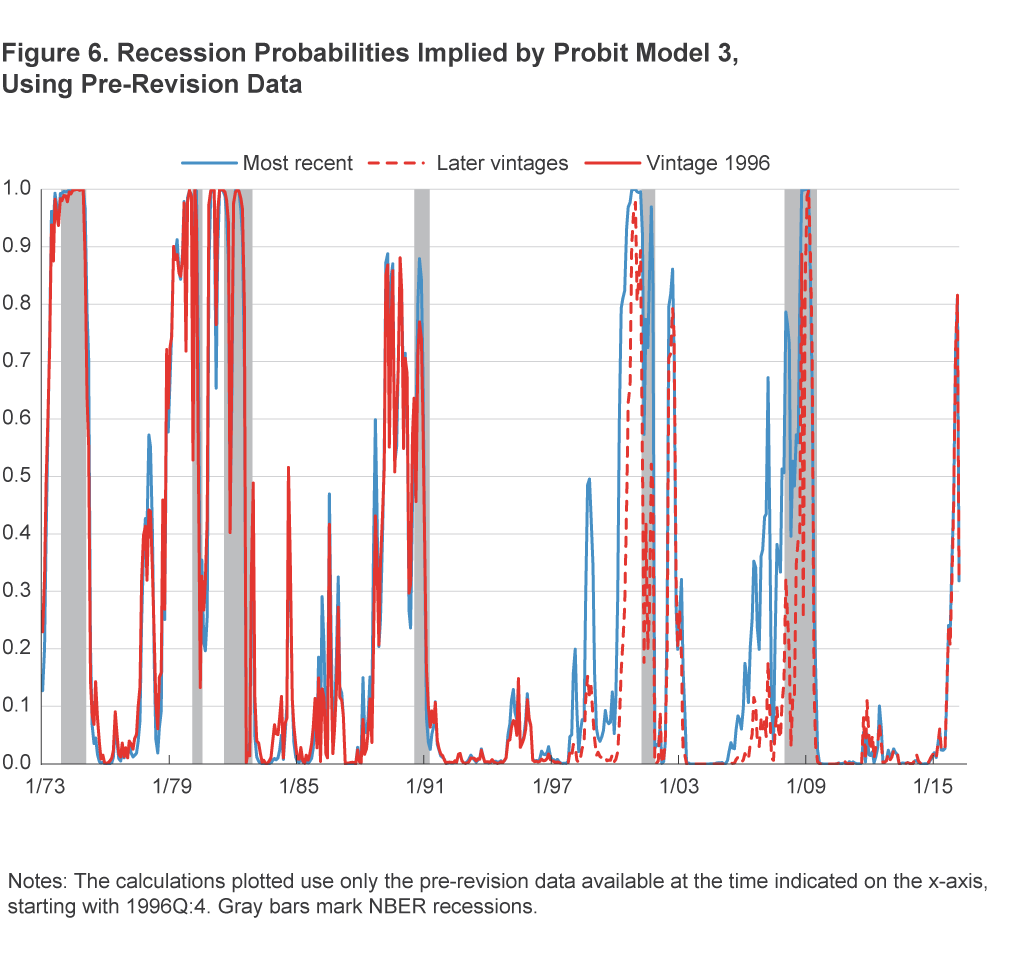

The downside of using corporate profits in the analysis is the inaccuracy of the real-time measures. The Bureau of Economic Analysis updates the National Income and Product Accounts (NIPA) annually as well as every four years or so during its comprehensive revision of the data sources, methodologies, and definitions. To examine how much the revisions impact the recession probabilities, I conduct the following exercise.

I start with the corporate profits data from early 1997, as it was known at the time of the first estimate of 1996:Q4. I choose this date in order to include at least four recessions in my estimation. Also, there was a comprehensive revision to the NIPA at the end of 1995. The solid red line in figure 6, from the beginning of the sample to December 1996, is the backward-looking probability estimates from this sample using model 3. Then, in every quarter after 1996:Q4, I estimate model 3 with the first estimate of the corporate profit data from that quarter and all the revisions incorporated at that time. I plot on the chart only the estimated probabilities from that quarter, without changing the data I already plotted (dashed red line). In other words, the dashed red line shows the 12-month-ahead recession probability as of that point in time but only for that current quarter. Note that the dashed red line and the blue line overlap perfectly at the end of the sample because the most recent data have not been revised yet.

The vintage analysis reveals that the greatest risk associated with data revisions is receiving the recession warnings too late. Pre-recession first estimates of profits are revised down significantly in later years, which results in the red line in figure 6 lying much higher than the dashed red line. While the post-recession first estimates are revised up later, there is no impact on recession probabilities, as the other components of model 3 are already pulling the probability down to zero.

Conclusion

Although the 12-month-ahead recession probabilities estimated using only the term spread have not exceeded 30 percent since the financial crisis, the estimates using credit spreads and corporate profits tell a different story. The recession probability in the first quarter of this year may have risen to 73 percent excluding the quarterly change in profits or as high as 81 percent including them. These probabilities later declined to around 30 percent.

While these estimates are large, they must be interpreted cautiously. The methodology is nothing more than a mechanism that puts investors’ anxiety and corporate profitability on a 0–1 scale. High measurements on this scale have often been followed by a recession in the past, but this is not a guaranteed outcome. In early the 2000s, for example, the Sarbanes-Oxley Act quickly restored investor confidence in corporate accounting, and credit spreads came down. As for today, our statistical technique cannot explain why investors were anxious during the first quarter of this year, whether their anxiety was justified, or whether they still have reason to be nervous. That’s too much to ask for a probability model.

Footnotes

- Ang, Piazzesi, and Wei (2006), Estrella and Hardouvelis (1991), Estrella and Mishkin (1997), Estrella and Mishkin (1998), Haubrich and Dombrosky (1996), Laurent (1988), Stock and Watson (1989), Stock and Watson (2001). See Österholm (2012) for an evaluation of an alternative method to predict recessions. Return to 1

- Gertler and Lown (1999), Gilchrist, Yankov, and Zakrajšek (2009), Gilchrist and Zakrajšek (2012), Favara, Gilchrist, Lewis, and Zakrajšek (2016). Return to 2

- One might also use the spread between corporates and US Treasuries. Return to 3

- The actual method of Gilchrist and Zakrajšek is more complex, but this brief description captures the intuition. Return to 4

- Specifically, I use the quarterly change in seasonally adjusted pre-tax corporate profits after inventory valuation and capital consumption adjustments, deflated by the CPI. Return to 5

- If I use a 95 percent confidence interval rather than 90 percent, profits Granger-cause investment three quarters ahead. Return to 6

- https://www.federalreserve.gov/econresdata/notes/feds-notes/2016/recession-risk-and-the-excess-bond-premium-accessible-20160408.html. Return to 7

- News records from the period explain the declining corporate profits with the strength of the dollar. Return to 8

- Easing is defined as the decline in the effective fed funds rate (or the Wu-Xia shadow federal funds rate after 2008) relative to the fed funds target implied by a Taylor rule that assigns equal weights to the output gap and PCE inflation. While it is not the case here, a constant effective fed funds rate in a rising implied-target environment would constitute easing or increasing accommodation by this definition. Return to 9

Further Reading

- Ang, A., M. Piazzesi, and M. Wei, 2006. “What Does the Yield Curve Tell Us About GDP Growth?” Journal of Econometrics, 131(1): 359-403.

- Estrella, A., and G. Hardouvelis, 1991. “The Term Structure as a Predictor of Real Economic Activity,” Journal of Finance, 46(2): 555–76.

- Estrella, A., and F.S. Mishkin, 1997. “The Predictive Power of the Term Structure of Interest Rates in Europe and the United States: Implications for the European Central Bank,” European Economic Review, 41(7): 1375-1401.

- Estrella, A., and F.S. Mishkin, 1998. “Predicting US Recessions: Financial Variables as Leading Indicators,” Review of Economics and Statistics, 80(1): 45-61.

- Favara, G., S. Gilchrist, K.F. Lewis, and E. Zakrajšek, 2016. “Recession Risk and the Excess Bond Premium,” Board of Governors of the Federal Reserve System, FEDS Notes. http://dx.doi.org/10.17016/2380-7172.1739.

- Gertler, M., and C.S. Lown, 1999. “The Information in the High-Yield Bond Spread for the Business Cycle: Evidence and Some Implications,” Oxford Review of Economic Policy, 15(3): 132-150.

- Gilchrist, S., V. Yankov, and E. Zakrajšek, 2009. “Credit Market Shocks and Economic Fluctuations: Evidence from Corporate Bond and Stock Markets,” Journal of Monetary Economics, 56(4): 471-493.

- Gilchrist, S., and E. Zakrajšek, 2012. “Credit Spreads and Business Cycle Fluctuations,” American Economic Review, 102(4): 1692-1720.

- Haubrich, J., and A.M. Dombrosky, 1996. “Predicting Real Growth Using the Yield Curve,” Federal Reserve Bank of Cleveland, Economic Review, Q1: 26-35.

- Laurent, R., 1988. “An Interest Rate-Based Indicator of Monetary Policy,” Federal Reserve Bank of Chicago, Economic Perspectives, 12(1): 3-14.

- Österholm, P., 2012. “The Limited Usefulness of Macroeconomic Bayesian VARs When Estimating the Probability of a US Recession,” Journal of Macroeconomics, 34: 76-86.

- Stock, J.H., and M.W. Watson, 1989. “New Indexes of Coincident and Leading Indicators,” in: Blanchard, O., Fischer, S. (Eds.), 1989 NBER Macroeconomics Annual. MIT Press, Cambridge, MA.

- Stock, J.H., and M.W. Watson, 2001. “Forecasting Output and Inflation: The Role of Asset Prices,” NBER Working Paper #8180.

Suggested Citation

Ergungor, O. Emre. 2016. “Recession Probabilities.” Federal Reserve Bank of Cleveland, Economic Commentary 2016-09. https://doi.org/10.26509/frbc-ec-201609

This work by Federal Reserve Bank of Cleveland is licensed under Creative Commons Attribution-NonCommercial 4.0 International