- Share

Regional Data, Analysis, and Engagement

Monitoring economic conditions in the Fourth District of the Federal Reserve System to inform monetary policy and improve the public’s understanding of the regional economy.

The region we serve

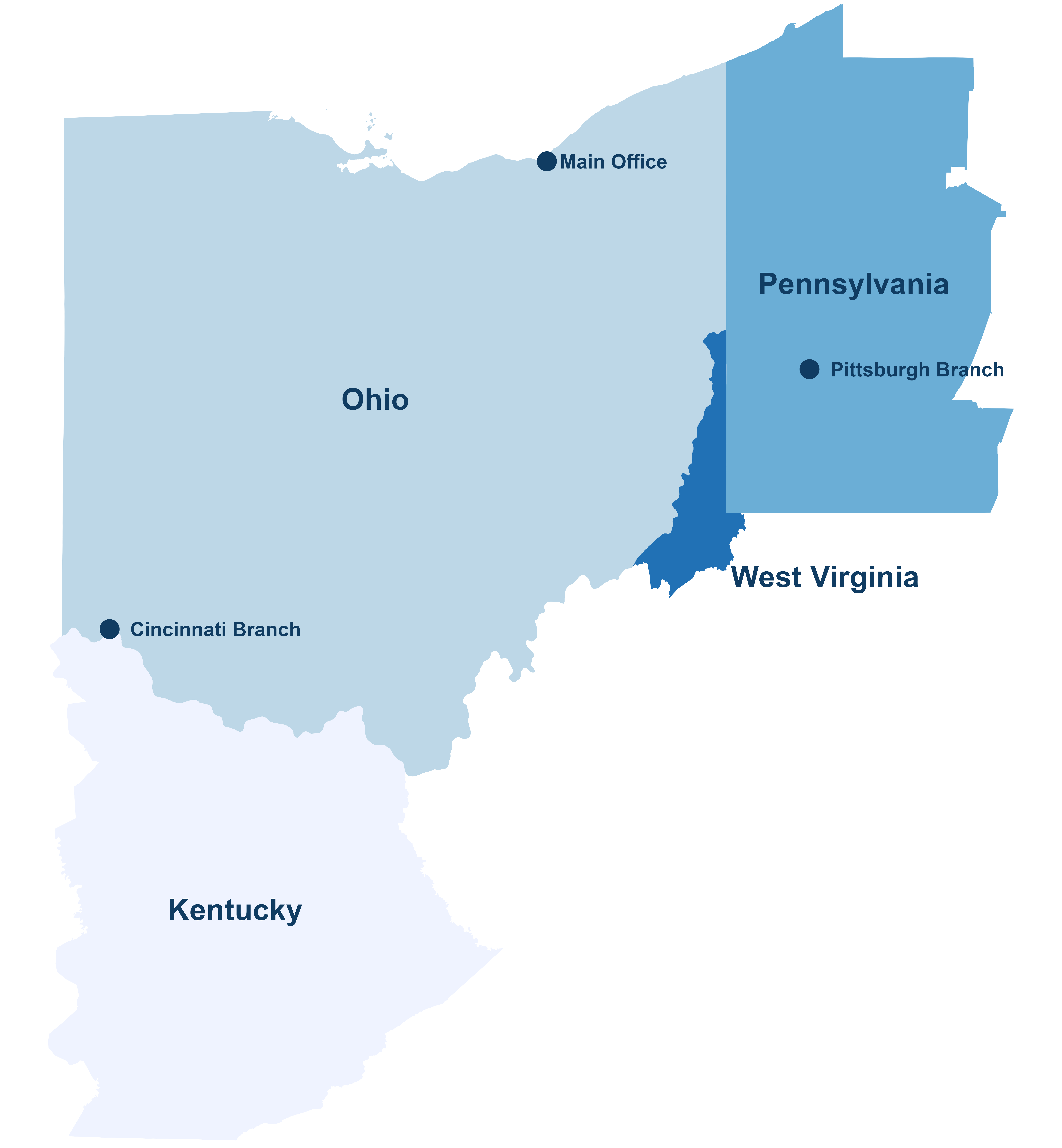

What is the Fourth District?

The Federal Reserve System is divided into 12 Districts. The Cleveland Fed serves the Fourth District, which encompasses the entire state of Ohio, 56 counties in eastern Kentucky, 19 counties in western Pennsylvania, and six counties in the northern panhandle of West Virginia. That’s 169 counties, nine major metropolitan statistical areas, and a population of approximately 17 million.

Within the Fourth District’s borders lie a range of industries—from manufacturing, agriculture, and mining to medicine and advanced technology—across a variety of communities, including older industrial cities and rural Appalachian areas.

What we do

Regional analysis

Our regional analysis group monitors the economy in the Federal Reserve’s Fourth District by tracking a variety of data and indicators and by gathering information from business and community leaders.

We regularly survey and interview business contacts to learn more about changes in customer demand, hiring, pricing, and more. We also convene Business Advisory Councils and roundtable discussions throughout the District.

We combine these insights with data to support our president's policymaking responsibilities and improve the public's understanding of how the region’s economy is evolving.

In our research, we analyze quantitative and qualitative data on topics including economic activity and consumer spending, labor and housing markets, household finance, and longer-term demographic and industrial trends. We also provide insightful perspectives on public-policy questions that are important to our region's longer-term economic prosperity.

Regional analysis publications

Regional analysis publications

Through mid-length reports and short-form briefs, our regional economists highlight the data we examine and provide public policymakers and other stakeholders with insightful analyses of policy issues that are important to the economic vitality of the region we serve.

Beige Book

The Beige Book is a Federal Reserve System publication about current economic conditions across the 12 Federal Reserve Districts. Eight times a year, the reports from each District characterize regional economic conditions based on a variety of mostly qualitative information, gathered directly from District sources, including interviews and online questionnaires completed by businesses, community organizations, economists, market experts, and other sources.

Regional data

Survey of Regional Conditions and Expectations Indicator

The Cleveland Fed Survey of Regional Conditions and Expectations (SORCE) indexes provide a timely summary of economic activity in the Federal Reserve’s Fourth District. The indexes are based on responses to the Cleveland Fed SORCE, a survey of business and community leaders about regional economic conditions.

Business Outlook and Trends Survey

The Business Outlook and Trends Survey (BOTS) is a biannual survey done in partnership with regional chambers of commerce. The results provide insights on regional demand for goods and services, labor markets, prices, and costs, which are used to inform the Cleveland Fed’s decision-making processes.

Engage with us and stay informed

Participate in the Survey of Regional Conditions and Expectations

Want to join our information-sharing network? Business owners, key decisionmakers, and industry leaders are invited to share their insights on current business conditions. By taking the survey, you would contribute to data that directly inform the Fed and policymakers. If you are interested in participating, contact our team to see if your organization would be a good fit.

Subscribe to Bank publications

Receive email alerts for new research published by the Cleveland Fed, including Economic Commentaries, the Beige Book, District Data Briefs, and reports on our region.

Meet our regional analysis team

Lisa Barrow

Brian Anderson

Brooke Dirtzu

Julianne Dunn

Jayme V. Gerring

Brett Huettner

Mitchell Isler

Russell Mills

Kevin Rinz

Stephan D. Whitaker

View the latest Beige Book

Latest research and events

The Human Factor: Why the Fed’s Work Isn’t All Numbers and Data

Whoever you are, the economy is affecting you and influencing your decisions, and your decisions in turn affect the economy. When central bank staff learn more about what’s happening in real time in local economies, they can (and do) share these experiences with those setting monetary policy for the country.

Business Advisory Councils

Business Advisory Council members are recruited annually and represent a cross-section of regional businesses, labor organizations, and economic development organizations to ensure that data collected on the regional economy reflect the views of an array of stakeholders.

Indicators and data

The Cleveland Fed maintains a broad range of indicators and datasets that are available for download, including median CPI, median PCE inflation, inflation expectations, yield curve and GDP growth, and simple monetary policy rules.

Request a speaker

The Cleveland Fed’s Speakers Bureau provides access to experts who can offer insight on a broad range of topics. Fed speakers can give presentations or serve as panelists, providing an exchange of ideas that fosters discussion and encourages audience involvement. We work with professional, business, and civic groups. This free service is available to groups of 25 or more.