- Share

Why Has Durable Goods Spending Been So Strong during the COVID-19 Pandemic?

Consumers increased their purchases of durable goods notably during the COVID-19 pandemic. The pandemic may have lifted the demand for durable goods directly, by shifting consumer preferences away from services toward a variety of durable goods. It may also have stimulated spending on durable goods indirectly, by prompting a strong fiscal policy response that raised disposable income. We estimate the historical relationship between durable goods spending and income and find that income gains in 2020 accounted for about half of the increase in durable goods spending, indicating that the direct and indirect effects of the pandemic on durable goods spending were about equally important.

The views authors express in Economic Commentary are theirs and not necessarily those of the Federal Reserve Bank of Cleveland or the Board of Governors of the Federal Reserve System. The series editor is Tasia Hane. This paper and its data are subject to revision; please visit clevelandfed.org for updates.

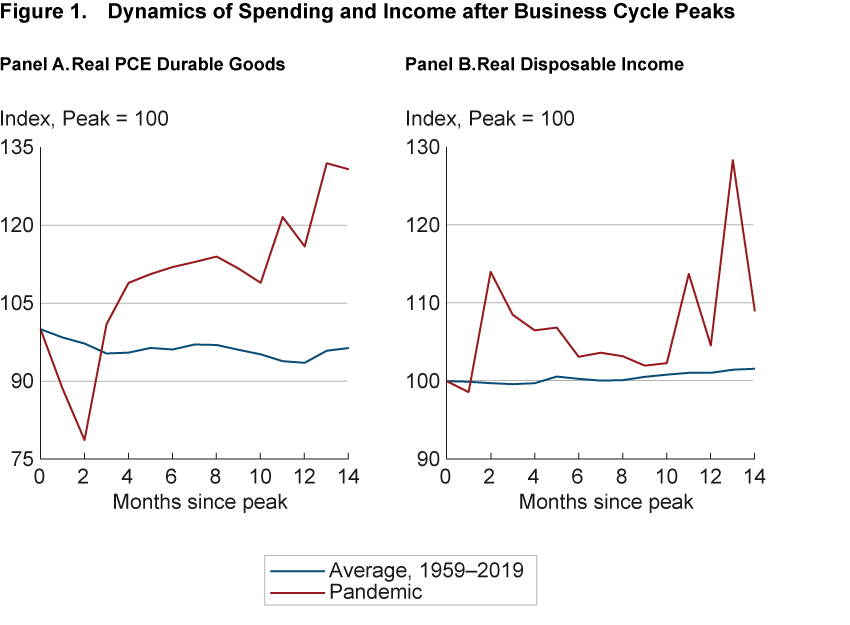

The US economy has witnessed many unusual developments during the COVID-19 pandemic, among them a surge in durable goods purchases by consumers. Durable goods spending typically slows gradually for a year after a business cycle peak, but it contracted briefly but severely at the onset of the pandemic and rose sharply thereafter (figure 1, panel A).

What accounts for the unusual behavior of durable goods spending during the pandemic? We explore two possible explanations using an econometric model. One explanation is that lockdowns and social distancing shifted consumer demand away from services toward durable goods. The other is that an increase in disposable income resulting from fiscal policy measures stimulated consumption expenditures, including those on durable goods. Our findings suggest that each explanation accounts for about half of the increase in durable goods purchases in 2020, although the relative importance of each effect varies for different types of durable goods. Purchases of recreational goods, such as consumer electronics and sporting equipment, likely increased primarily because households used these goods as substitutes for services. In contrast, motor vehicle purchases benefited from higher incomes, with substitution away from public transit playing no apparent role at the aggregate level.

Understanding the factors behind the rise in durable goods spending can inform policymakers’ assessments of the pandemic policy responses. On the one hand, substitution of durable goods for services would indicate that the overall economic cost of health policy measures that restrict services is smaller than indicated by the observed decline in services consumption alone. On the other hand, a boost to consumer spending from higher disposable incomes would corroborate the efficacy of fiscal stimulus.

Note: The left panel of the figure compares the evolution of real personal consumption expenditures (PCE) on durable goods since the peak of the last business cycle in February 2020 with its “typical” evolution after the peak of prior business cycles, as represented by the average across the eight business cycles in the period from 1959 to 2019. The right panel compares the evolution of real disposable income over the same two periods.

Source: Bureau of Economic Analysis, Haver Analytics.

Altered Tastes or Increased Ability to Spend?

The increase in durable goods spending observed during the pandemic could be the result of a number of factors. Two likely possibilities are that the historic change in consumers’ circumstances altered what they wanted to buy and that an increase in their disposable income due to fiscal policy measures changed how much they could buy.

Lockdowns and social distancing, reflecting precautions taken by government authorities, businesses, and consumers in the face of COVID-19, may have led to an increase in durable goods spending by shifting consumer demand away from services toward durable goods. Many people spent more time than usual in and around their home, to care for others, work or study from home, engage in home production, or enjoy leisure activities, thereby reducing their consumption of services such as eating out or traveling. Durable goods allow consumers to derive greater utility from their time spent at home and accomplish tasks they might have purchased as services before the pandemic. For example, consumers who stopped visiting restaurants may have upgraded their kitchen appliances to cook at home, and people who canceled their gym membership may have purchased a bike to work out at home. Such substitution of durable goods for services is a direct consequence of how COVID-19 has altered consumption behavior.

An increase in consumers’ disposable income during the pandemic may have stimulated consumption expenditures, including on durable goods. Disposable income did rise sharply during the pandemic, whereas it edged up only gradually after the peak of previous business cycles(figure 1, panel B).1 The idea that higher disposable income spurs consumer spending goes a long way back, to Keynes (1936), and is embodied in textbook consumption functions.2 As the catalyst of the rise in disposable income, the pandemic may have indirectly provoked the durable goods spending boom.

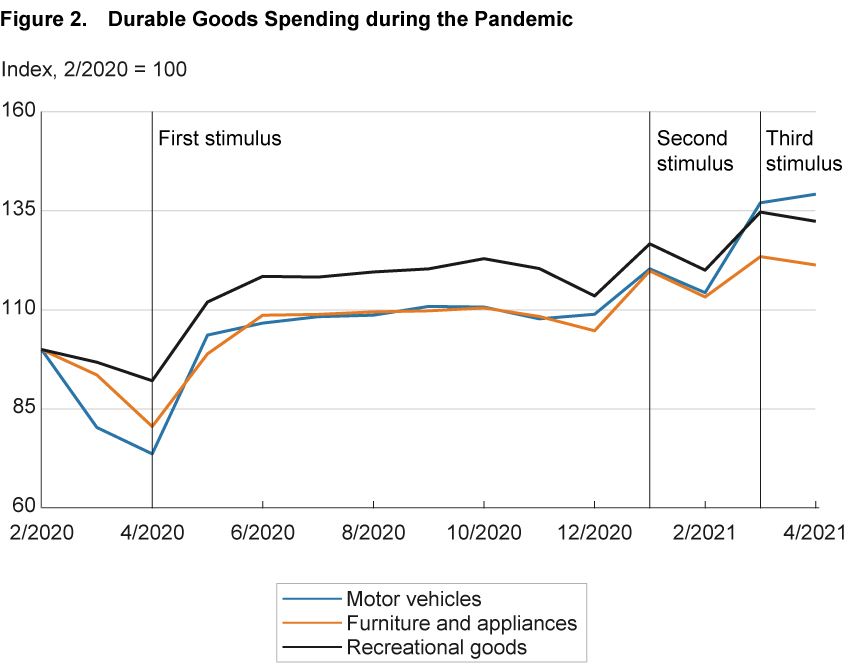

The increase in disposable income largely reflects the forceful fiscal policy measures that were put in place to deal with the economic fallout of the pandemic. According to the US national accounts, total disposable income rose by$1.18 trillion in 2020 compared to 2019, and more than 80 percent ($957 billion) of this increase stems from fiscal policy responses to the pandemic.3 Figure 2 displays real personal consumption expenditures (PCE) in three major categories of durable goods—motor vehicles, furniture and appliances, and recreational goods—along with vertical lines indicating the periods during which the bulk of three stimulus payments were disbursed. The first round of these payments was paid out in April and May 2020 and coincided with a rebound in spending on all three categories of durable goods in May. The second and third rounds of stimulus payments were disbursed in January 2021 and March and April 2021, respectively, and coincided with further broad increases in durable goods purchases in January and March. The timing suggests that the pandemic has stimulated durable goods spending indirectly by triggering a boost in disposable income.4

Notes: The labels motor vehicles, furniture and appliances, and recreational goods correspond to the PCE categories of motor vehicles and parts, furnishings and durable household goods, and recreational goods and vehicles, respectively, in the US national accounts. The vertical lines indicate the periods during which the bulk of the three stimulus payments were disbursed.

Source: Bureau of Economic Analysis, Haver Analytics.

To disentangle the direct and indirect effects of the pandemic on durable goods spending, we turn to an econometric model.

Empirical Analysis of Durable Goods Spending

The econometric model is a panel regression that relates the growth in durable goods spending in each of the 50 US states to the state’s growth in personal income and controls for state and time fixed effects. The regression coefficient for income growth estimates the marginal propensity to consume (MPC) out of income. The panel regression specifies a common MPC across US states, and the state fixed effects absorb trend differences in durable goods spending between states. The time fixed effects are included to capture changes from year to year in the relationship between durable goods spending and income.5 The online appendix provides details of the model. It is a variant of the model of Luengo-Prado and Sørensen (2008), who estimate the MPC for nondurable retail sales and include additional variables that interact with income growth.

We estimate the MPC for real PCE on durable goods and its three major components, PCE for motor vehicles, furniture and appliances, and recreational goods. Income is measured by personal income, which consists of market income and transfer receipts from the government, including the stimulus payments and other pandemic-related transfer payments to households.6 All variables are measured in constant prices and converted to per capita terms. The data for the 50 US states are available at annual frequency from 1997 to 2019, thus allowing us to estimate the sensitivity of durable goods spending to income during a period before the pandemic struck the economy.

Table 1 presents the estimation results. The estimated MPC for durable goods PCE is 0.6, indicating that an additional dollar of income raises durable goods purchases by 60 cents. The MPC is somewhat larger for motor vehicles and for furniture and appliances, suggesting that it may be somewhat lower for other durable goods that are not included in the three subcategories. The estimated MPCs are statistically and economically significant, roughly twice as large as those estimated by Luengo-Prado and Sørensen (2008) for nondurable retail sales, so they could lead a sharp rise in income to induce a sizable boost to durable goods purchases.

| Durable goods | Motor vehicles | Furniture and appliances | Recreational goods | |

| MPC | 0.599*** | 0.678*** | 0.685*** | 0.601*** |

| (0.037) | (0.049) | (0.051) | (0.062) | |

| Sample size | 1,100 | 1,100 | 1,100 | 1,100 |

Notes: The table reports ordinary least squares (OLS) regression results for the model (A.2) in the online appendix. Stock and Watson (2008) heteroskedasticity-robust standard errors are in parentheses. The *** denotes statistical significance at the 1 percent level.

Sources: Bureau of Economic Analysis, Haver Analytics, and authors’ calculations.

Direct and Indirect Effects of the Pandemic

We use the estimated model to predict the direct and indirect effects of the pandemic on durable goods spending. Regarding the indirect effect, combining the estimated MPC and the state-level income growth, which is already observed for 2020, yields a prediction of the effect of pandemic-induced higher income on durable goods spending. As for the direct effect of the pandemic, it is captured by the predicted time fixed effect for 2020 and can be obtained residually, because the growth in aggregate durable goods spending is already observed for 2020 even though state-level data for 2020 have not yet been released.

To make the argument more concrete, consider the predicted durable goods spending growth in state s for the year 2020. The panel regression model (detailed in the online appendix) can be rearranged to show that the predicted spending growth is

(1) ĉs,2020 = [c̅s − c̅ − β(y̅s − y̅)] + βys,2020 + (c̅2020 − βy̅2020),

where c denotes the growth rate of durable goods spending, y denotes the growth rate of personal income, a horizontal line over a variable denotes its average across states (subscript 2020), time (subscript s), or both (no subscript), and a caret denotes a prediction.

Equation (1) shows that the forecast of state-level durable goods spending growth is composed of three distinct terms. The first term, in brackets, captures long-run factors and is therefore not related to the pandemic. This constant term measures, for each state, the state-specific durable goods PCE growth that does not reflect state-specific income growth.

The second term on the right-hand side of equation (1) measures the portion of spending growth attributable to income growth in 2020. As pointed out above, the US national accounts indicate that the recent growth in disposable income resulted primarily from the fiscal response to the pandemic—that is, the indirect effect of the pandemic on durable goods spending.

The third term reflects the time fixed effect for 2020 and captures the extent to which growth in aggregate spending on durable goods in 2020 was unusually high or low given the growth in aggregate income for that year. Although fixed effects do not provide an explanation for the unusual spending growth other than “because it is 2020,” equation (1) shows that the third term captures economy-wide factors, other than income, that influenced durable goods purchases. Since the US economy was severely affected by the pandemic during most of 2020, this term likely captures a shift in the demand for durable goods related directly to the pandemic.

The shift in the demand for durable goods captured by the fixed effect for 2020 could reflect multiple factors. First, as pointed out above, the shift may reflect the substitution of durable goods for services as the pandemic altered consumers’ tastes and restricted their access to services. Second, the pandemic may also have influenced durable goods spending through an increase in macroeconomic uncertainty, which could dampen spending by leading households to postpone big-ticket purchases. Since macroeconomic uncertainty reduces durable goods spending, it would imply a stronger shift in consumers’ tastes for durables instead of services, given the net magnitude of the fixed effect for 2020. Third, favorable financial conditions, likely related to macroeconomic policy responses to the pandemic, may have stimulated durable goods spending. Specifically, the accommodative stance of monetary policy may have lowered borrowing rates for financing durable goods purchases and boosted asset valuations that contribute to a wealth effect on spending. However, empirical research indicates that interest rate and wealth effects are relatively small, suggesting they may form a less important factor behind the fixed effect for 2020.7 All told, the economy-wide factors specific to 2020 capture a shift in the demand for durable goods during the pandemic that likely reflects, importantly but not only, consumers’ substitution of durable goods for services.

Table 2 presents the growth rates of aggregate real per capita durable goods PCE and its three major components in 2020, along with the predicted contributions from long-run factors, income growth, and the fixed effect for 2020. Aggregate growth of real per capita durable goods purchases in 2020 is calculated by adjusting aggregate spending growth for US population growth in 2020. As shown on the first line of the table, real per capita durable goods PCE increased by 5.8 percent, was essentially unchanged for motor vehicles, and increased by 5.1 percent for furniture and appliances and 17.5 percent for recreational goods.

The predicted contributions, displayed in the bottom three lines of table 2, are obtained by aggregating each of the three terms on the right-hand side of equation (1) across states using appropriate state weights, as explained in the online appendix. First, the predicted contribution of long-run factors for the US economy is essentially zero. An unweighted average of the constant terms for each state would equal exactly zero, as distinct trends in individual states’ spending and income growth average out at the national level.

| Durable goods | Motor vehicles | Furniture and appliances | Recreational goods | ||

| Actual | 5.80 | 0.01 | 5.14 | 17.47 | |

| Predicted | |||||

| Long-run factors | 0.02 | 0.04 | 0.00 | 0.02 | |

| Income growth | 2.76 | 3.10 | 3.13 | 2.80 | |

| Fixed effect 2020 | 3.03 | −3.13 | 2.01 | 14.65 | |

Note: The bottom three numbers in each column may not add up to the first number in the column due to rounding.

Sources: Bureau of Economic Analysis, Haver Analytics, and authors’ calculations.

Second, the predicted contribution from income growth, which captures the indirect effect of the pandemic on durable goods spending growth, amounts to 2.8 percentage points or almost half of the growth in durable goods PCE. The major types of durable goods show some notable differences. Income growth boosted motor vehicle purchases and accounted for the majority of the increase in purchases of furniture and appliances, but it accounted for only a small portion of the increase in purchases of recreational goods.

Third, the economy-wide factors specific to 2020, which capture the direct effect of the pandemic on durable goods spending growth, are obtained residually by subtracting the two other predicted growth terms from actual growth. This effect contributed 3.0 percentage points, or slightly more than half, to the observed growth in real per capita durable goods PCE. The major types of durable goods again display some interesting differences. The pandemic’s direct impact on motor vehicle spending was negative, indicating that substituting for services such as public transit was not a major driver of aggregate motor vehicles purchases, a conclusion that is consistent with the sharp decline in vehicle miles traveled.8 In contrast, the increase in purchases of recreational goods appears to reflect primarily a change in consumer preferences induced by the pandemic.9

Conclusion

The surge in durable goods purchases by consumers was an unusual macroeconomic development, one among many brought about by the COVID-19 pandemic. Our analysis has found that altered consumer tastes and increased disposable incomes were two important factors behind the surge, although monetary policy may have contributed as well by fostering favorable financial conditions. The importance of these factors is likely to fade as public health concerns are mitigated by increasing vaccinations and the US economy reopens. Consumers’ shopping baskets will likely come to resemble more closely the historical mix of durable goods, nondurable goods, and services as social distancing requirements are relaxed.10 Disposable income will likely settle around its longer-term trend level as the pandemic fiscal support is withdrawn. Consequently, consumer spending on durable goods may slow for some time.

Footnotes

- The unusual rise in disposable income during the pandemic occurred in the face of reductions in gross domestic product (GDP) and employment. Real disposable income rose 3.9 percent in the fourth quarter of 2020 from a year earlier, whereas real GDP declined 2.4 percent and nonfarm payroll employment declined 6.0 percent. Return to 1

- While the theory of consumption has evolved since Keynes—the two most prominent models of consumption behavior today are the life-cycle hypothesis and the permanent income hypothesis—the Keynesian concept of a marginal propensity to consume out of income persists in contemporary analyses. See, for example, Mankiw (2019, Chapter 19) for a concise overview of consumer theory. Return to 2

- The US national accounts list the pandemic-income transfers related to 12 government programs. The largest three types of programs are the stimulus payments, various unemployment benefits programs, and forgivable loans through the Paycheck Protection Program. The three periods that witnessed the largest stimulus payments were April–May 2020 ($266.2 billion), January 2021 ($138.4 billion), and March–April 2021 ($394.4 billion). Return to 3

- A number of recent papers analyze consumer spending in the pandemic. Chetty et al. (2020) analyze the responses to the pandemic of economic indicators in the Opportunity Insights database. Baker et al. (2020) explore the consumption response to the early spread of COVID-19, while Coibion et al. (2020) examine the consumption response to the first stimulus payments enacted with the CARES Act, and Carroll et al. (2021) predict the consumption response to different components of the CARES Act. Relatedly, Parker et al. (2013) examine the consumption response to the stimulus payments of 2008. Return to 4

- The time fixed effects control for aggregate variation, which mitigates concerns about endogeneity. Any feedback from fluctuations in state-specific durable goods purchases to its state-specific (labor) income would likely be limited to the state’s wholesale and retail trade activity and leave its manufacturing activity essentially unaffected. Return to 5

- Personal income differs from disposable personal income by including personal taxes and social security contributions. For the aggregate economy, personal income and disposable personal income move almost in lockstep, with a correlation of 0.999 in the sample from 1929 to 2020, indicating that either income measure would yield similar regression results. We use the personal income data in the regression because they are available at the state level. Return to 6

- Regarding interest rates, previous research finds no strong dependence of consumption on the interest rate as many consumers face borrowing constraints (Hall, 1988, Campbell and Mankiw, 1989), although spending on durable goods is more responsive to interest rates than other consumption spending (Erceg and Levin, 2006). Wealth effects are generally found to be much smaller than those from the MPC (Carroll et al., 2011). Return to 7

- Vehicle miles traveled fell 13.2 percent in 2020 from 2019 according to the US Federal Highway Administration. In a survey conducted in late 2020, CarGurus (2020) found that only 14 percent of pandemic car buyers cited as the reason that they “did not want to rely on public transport, ride-share, or taxis.” About twice as many pandemic car buyers (27 percent) did so for recreational purposes: they “wanted to buy a vehicle for personal travel, leisure, hobbies, or projects.” Return to 8

- Because many recreational goods are inexpensive compared to motor vehicles, credit likely plays a smaller role in financing their purchases. Thus, the finding that the pandemic had a large direct effect on recreational goods and a small direct effect on motor vehicles is consistent with the notion that the direct effect reflects a change in consumer preferences rather than low interest rates. Return to 9

- In a survey of consumers, Knotek et al. (2021) find that after the COVID-19 crisis ends, the typical consumer expects to return to using high-contact services—hospitality, public transportation, and public events—to a similar extent as before the pandemic. Return to 10

References

- Baker, Scott R., Robert A. Farrokhnia, Steffen Meyer, Michaela Pagel, and Constantine Yannelis. 2020. “How Does Household Spending Respond to an Epidemic? Consumption during the 2020 COVID-19 Pandemic.” The Review of Asset Pricing Studies, 10(4): 834–862. https://doi.org/10.1093/rapstu/raaa009.

- Campbell, John Y., and N. Gregory Mankiw. 1989. “Consumption, Income, and Interest Rates: Reinterpreting the Time Series Evidence.” In Olivier Jean Blanchard and Stanley Fischer (Eds.), NBER Macroeconomics Annual, Vol. 4, National Bureau of Economic Research, University of Chicago Press Journals: 185–246. https://doi.org/10.1086/654107.

- CarGurus. 2020. “CarGurus COVID-19 Sentiment Study. How the Pandemic Impacted Automotive Sentiment in 2020.” https://go.cargurus.com/rs/611-AVR-738/images/USNov_Covid19-Survey_CarGurus.pdf.

- Carroll, Christopher D., Edmund Crawley, Jiri Slacalek, and Matthew N. White. 2021. “Modeling the Consumption Response to the CARES Act.” International Journal of Central Banking, 17(1): 107–141.

- Carroll, Christopher D., Misuzu Otsuka, and Jiri Slacalek. 2011. “How Large Are Housing and Financial Wealth Effects? A New Approach.” Journal of Money, Credit and Banking, 43(1): 55–79. https://doi.org/10.1111/j.1538-4616.2010.00365.x.

- Chetty, Raj, John N. Friedman, Nathaniel Hendren, Michael Stepner, and the Opportunity Insights Team. 2020. “The Economic Impacts of COVID-19: Evidence from a New Public Database Built Using Private Sector Data.” National Bureau of Economic Research, Working Paper No. 27431. https://www.doi.org/10.3386/w27431.

- Coibion, Olivier, Yuriy Gorodnichenko, and Michael Weber. 2020. “How Did U.S. Consumers Use Their Stimulus Payments?” National Bureau of Economic Research, Working Paper No. 27693. https://www.doi.org/10.3386/w27693.

- Hall, Robert E. 1988. “Intertemporal Substitution in Consumption.” Journal of Political Economy, 96(2): 339–357. https://doi.org/10.1086/261539.

- Keynes, John Maynard. 1936. The General Theory of Employment, Interest and Money. MacMillan.

- Knotek, Edward S. II, Michael McMain, Raphael Schoenle, Alexander Dietrich, Kristian Ove R. Myrseth, and Michael Weber. 2021. “Expected Post-Pandemic Consumption and Scarred Expectations from COVID-19.” Federal Reserve Bank of Cleveland, Economic Commentary, 2021-11. https://doi.org/10.26509/frbc-ec-202111.

- Luengo-Prado, María José, and Bent E. Sørensen. 2008. “What Can Explain Excess Smoothness and Sensitivity of State-Level Consumption?” Review of Economics and Statistics, 90(1): 65–80. https://doi.org/10.1162/rest.90.1.65.

- Mankiw, N. Gregory. 2019. Macroeconomics. Tenth Edition, Worth Publishers.

- Parker, Jonathan A., Nicholas S. Souleles, David S. Johnson, and Robert McClelland. 2013. “Consumer Spending and the Economic Stimulus Payments of 2008.” American Economic Review, 103(6): 2530–2553. https://doi.org/10.1257/aer.103.6.2530.

- Stock, James H., and Mark W. Watson. 2008. “Heteroskedasticity-Robust Standard Errors for Fixed Effects Panel Data Regression,” Econometrica, 76(1): 155–174. https://doi.org/10.1111/j.0012-9682.2008.00821.x.

Suggested Citation

Tauber, Kristen, and Willem Van Zandweghe. 2021. “Why Has Durable Goods Spending Been So Strong during the COVID-19 Pandemic?” Federal Reserve Bank of Cleveland, Economic Commentary 2021-16. https://doi.org/10.26509/frbc-ec-202116

This work by Federal Reserve Bank of Cleveland is licensed under Creative Commons Attribution-NonCommercial 4.0 International