- Share

Monetary Policy Tightening and Long-Term Interest Rates

The Federal Open Market Committee (FOMC) has maintained an accommodative monetary policy ever since the 2007 recession, and some financial market participants are concerned that long-term interest rates may increase more than should be expected when the Committee starts to tighten. But a look at five historical episodes of monetary policy tightening suggests that such an outcome is more likely when markets are surprised by policy actions or economic developments. Given the Fed’s new policy tools, especially its evolution toward more transparent communications, the odds of a surprise are far less likely now.

The views authors express in Economic Commentary are theirs and not necessarily those of the Federal Reserve Bank of Cleveland or the Board of Governors of the Federal Reserve System. The series editor is Tasia Hane. This paper and its data are subject to revision; please visit clevelandfed.org for updates.

In the wake of the last recession, the Federal Open Market Committee (FOMC) implemented what has arguably been the longest and most accommodating spell of monetary policy in its history. The Committee’s traditional monetary policy tool, the federal funds rate (FFR), has been as low as it can be—at the zero lower bound, in economics jargon—since late 2008.

During the same time, new tools designed to deliver further accommodation in the context of the zero lower bound have been introduced. For example, in an effort to lower long-term interest rates, the Fed has purchased a substantial amount of assets that historically it has not held much of, like long-term Treasury securities and the debt and mortgage-backed securities (MBS) of federal agencies like Fannie Mae.

Another type of tool involves the Committee’s communications with the public. In the statements it puts out after each meeting, the Committee has been using language meant to provide the market with “forward guidance”—information about what policy will likely be in the future. Recently, the Committee has promised to keep rates low for an extended period of time and conditioned the future path of the federal funds rate and the Fed’s balance sheet on particular economic outcomes.

Perhaps because of the unprecedented nature of this episode, some financial market participants have raised concerns regarding the possibility that long-term interest rates may increase more than should be expected when the Committee starts to tighten. (As if on cue, in late June, the 10-year Treasury rate moved up almost 50 basis points in the space of two weeks.)

But I think history—and the Fed’s new policy tools— suggest otherwise. After studying past tightening episodes, I conclude that the move to a less accommodative monetary policy stance is unlikely to bring about significant disruptions to credit markets, unless both the markets and the FOMC seriously underestimate future growth (or equivalently, future inflation). While some of the current circumstances, like the relatively high maturity of Treasuries outstanding or the historically unprecedented size of the Federal Reserve’s balance sheet, may pose challenges, these should be overcome by the current set of policy tools the FOMC has at its disposal.

Tightening Cycles since 1983

I look back at each of the preceding five tightening episodes since 1983 to examine how long-term interest rates behaved. I started the analysis in 1983 because it coincides with a period of significant change in Fed policy. Paul Volcker had just finished his first term as chairman of the Federal Reserve (he would be reappointed by President Reagan in July 1983). Volcker is widely credited with having ended years of stagflation—high unemployment and high inflation—during his first term and having inaugurated a new era of FOMC monetary policy in terms of its efficacy and credibility.

The Fed’s monetary policy goals, as mandated by Congress in its 1977 amendment to the Federal Reserve Act, are twofold: price stability and maximum employment. Although the FOMC has considerable discretion in the pursuit of those goals, traditionally, monetary policy has been conducted by targeting the federal funds rate—the overnight interest rate at which depository institutions trade balances held at the Federal Reserve. Although the Committee does not set the fed funds rate directly, it conducts open market operations (trading short-term government securities with depository institutions) to keep the rate close to the Committee’s target.

A tightening cycle typically develops as a consequence of the economy’s expansion. As unemployment decreases, if the Committee expects inflation to be substantially above target, it increases the FFR target (selling short-term government securities). Higher interest rates then slow down economic activity (but not so as to compromise the employment goal) and bring inflation down.

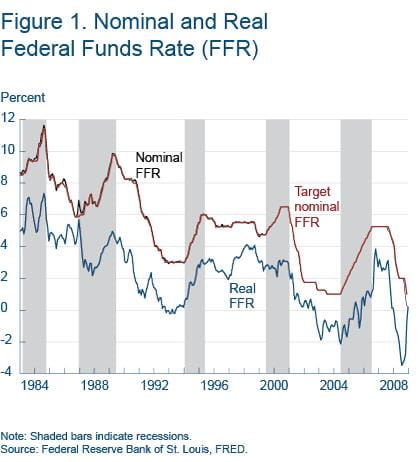

Figure 1 shows five clear episodes of tightening after 1983 (defined by sustained increases in the federal funds rate target.1) The circumstances leading up to the tightening in most of these five instances were broadly similar, with the Committee trying to react to what it judged to be incipient signs of inflationary pressure.

Note: Shaded bars indicate recessions.

Source: Federal Reserve Bank of St. Louis, FRED.

April 1983 to August 1984

In the first half of 1983 the economy was starting to recover from the “twin recessions” of 1980–82. The FOMC was keenly aware of how fragile the incipient recovery was and started the year by standing pat on monetary policy. However, as growth projections started to come in stronger than anticipated, the Committee moved to tightening and eventually moved the target FFR from 8.5 percent to 11.5 percent over this period.

April 1987 to May 1989

In the first quarter of 1987, inflation seemed very much under control, and growth had actually been slowing down since its 1984 peak. But on a conference call on April 29, the decision was made to start tightening. Such conference calls were not uncommon and happened whenever pressures developed in the fed funds market that required a review of the directive the Committee issued to its securities trading desk at the New York Fed. At this time the FFR was already running 75 basis points above the implicit target of 6 percent. The Committee would eventually move the target FFR from 6 to 9 percent over this period with a brief hiatus following the 1987 stock market crash, after which the FFR was lowered as a way to provide much needed liquidity to the market.

February 1994 to February 1995

The February 1994 FOMC meeting turned out to be one of historical significance, at least for Fed watchers. Not because the Committee decided to start increasing rates, although it did, but because it actually issued a public statement saying it would do so. The FFR would eventually rise 300 basis points, from 3 to 6 percent, in a year. With the hindsight provided by looking at the minutes and transcripts of FOMC meetings, the Committee seems to have been responding to an unexpected pick-up in economic growth. At the September 1993 meeting, participants were predicting 2.5 percent growth in 1994, well below the 4.1 percent growth that would eventually materialize.

July 1999 to May 2000

At its late June 1999 meeting, the Committee increased the FFR from 4.75 to 5 percent as a preemptive move to reduce inflation risks. At that juncture, inflation was predicted to come in very strong in the second quarter of 1999 (as it did), and economic growth was expected to accelerate going into the third quarter of that year. This cycle would turn out to be relatively brief and only took the policy rate up to 6.5 percent.

July 2004 to July 2006

In the first half of 2004 the Committee was particularly attentive to the possibility that economic growth would accelerate unexpectedly, leading to inflationary pressures. When its forecast for CPI inflation over the second and third quarters increased substantially, it took the opportunity to remove some accommodation. Even though it judged inflationary pressures to be temporary, tightening seemed appropriate, as the FFR was at a 45-year low of 1 percent. Clocking in at two years, this cycle was particularly long and took the FFR all the way up to 5.25 percent.

Tightening and Long-Term Interest Rates

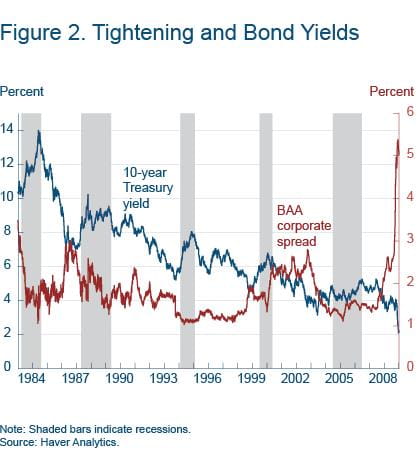

The increases in short-term interest rates described in these episodes resulted in increases in longer-term Treasury rates, as shown in figure 2. It is generally understood that as short-term rates increase, long-term rates follow suit, at least early in the tightening cycle. That is because the return on holding a 10-year bond to maturity should be related to that of holding a sequence of shorter-term bonds over the same period, as market participants are free to pursue both strategies. If the former increased relative to the latter, investors would flock to the long-term bond, bidding up its price and lowering its yield and vice versa.

This relationship means that, as a first approximation, one can think of the 10-year rate as the average of the expected relevant short-term rates over the next 10 years. Anything that raises the path of expected short-term rates—like the expectation that the FOMC will start tightening policy or an increase in inflation expectations—should raise long-term rates. This is noticeable, for example, in the 1999 episode. Then, inflation expectations moved up from 2.3 percent in November 1998 to 2.8 percent in May 1999 (before the FOMC actually increased short-term rates) and so did long-term Treasury rates, as can be seen in figure 2.

Note: Shaded bars indicate recessions.

Source: Haver Analytics.

Like long-term Treasuries, the prices of other long-term securities, such as corporate bonds, tend to behave the same way and decrease during tightening episodes. Nonetheless, corporate bond yields tend to increase by less than Treasury yields of comparable maturity.2 That is, the corporate spread (the difference in yields between corporate and Treasury bonds of the same maturity) tends to decrease during tightening episodes, as figure 2 shows.3 If history is any guide, when interest rates start rising this time, corporate bond prices will fall by proportionately less than the prices of Treasury bonds of comparable maturities.

Anecdotally, much of the current concern about policy accommodation stems from comparisons to the 1994 episode. At that time, yields on 10-year Treasury bonds increased over 200 basis points in one year. The pace of this increase seems to have been largely unanticipated by many in the bond market, as it was reportedly associated with large losses.4 Moreover, the increase was accompanied by rising rates elsewhere in the world, making it harder on investors looking for alternative investments.5 But one should notice that equal- or larger-sized increases in the FFR occurred earlier in 1987–1988 and later in 2004–2006, with seemingly less adverse consequences for bond markets. One is led to think that the magnitude and speed of adjustment are less important than the extent to which the market anticipates the changes.

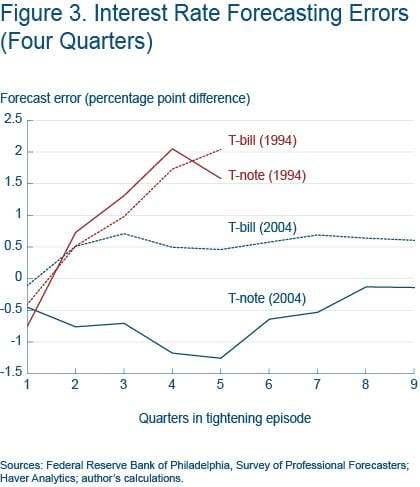

To check on this conjecture, I compare interest rate expectations, as given by the Survey of Professional Forecasters, to realized interest rates in the 1994 and 2004 episodes. Figure 3 shows the difference between the actual interest rate in every quarter of each tightening episode and the interest rate that was expected a year earlier, for both a short- and a long-term security.

Sources: Federal Reserve Bank of Philadelphia, Survey of Professional Forecasters; Haver Analytics; author's calculations

There is a clear contrast between the two episodes. While in the 2004 episode forecasting errors were relatively small and stable (most below 1 percentage point in absolute value), in the shorter 1994 episode this was not the case. Forecasting errors were increasing and ended up being relatively large, as yields consistently surprised on the upside.

To form expectations about interest rates, the market needs to predict not only economic conditions such as economic growth and inflation but also how the FOMC will react to these conditions in adjusting short-term interest rates. The problem in 1994 seems to have resided with the former. First, as mentioned before, the minutes show that the FOMC itself was surprised by stronger-than-expected growth. Second, FFR futures market data show that the market mostly correctly predicted increases in the FFR on the days preceding the meetings and as far as three months in advance.6

What Is Different This Time?

A lot has changed since the Committee last removed policy accommodation back in 2004–2006. In thinking about what changes might make a difference for the outlook this time, three areas seem most significant. These are changes in the Treasury market, changes in the nature of those who hold Treasuries, and, of course, changes in the way monetary policy is conducted.

In the Treasury market, the average maturity of outstanding Treasuries is higher now by roughly a year. The Treasury formulates its own, independent, debt issuance plan, presumably designed to finance government spending as cheaply and effectively as possible. In doing so, it takes into account multiple factors affecting the relative demand for each maturity and thus the slope of the yield curve. Such factors include not only safe haven and collateral motives on the part of private investors, but also the behavior of central banks around the world including the Fed. An argument can be made that, in the aftermath of the financial crisis, the behavior of both private and institutional investors has increased demand for relatively longer-term securities, and therefore bolstered the incentives for the Treasury to issue further down the maturity curve. As the average outstanding maturity increases, so does interest rate risk, implying that the potential for capital losses, everything else being the same, is higher.

The nature of Treasury holders has also changed substantially. The share of Treasuries in the hands of official institutional entities like the Federal Reserve and foreign central banks has more than doubled. Such institutions are substantially less likely to dump Treasuries once prices start falling, which should hinder any repeat of the fire sales that occurred in 1994. Some analysts cite those fire sales, which were associated with excessive leverage and margin calls, for the precipitous fall in Treasury prices in 1994.

Perhaps the most significant changes though, have come from how monetary policy has evolved since the crisis. After the FFR hit the zero lower bound, traditional monetary policy took a back seat, and tools that the Committee had not used in the past came to prominence. These tools make the likelihood of a smoother transition higher.

For example, in the same way that the Fed’s sizeable portfolio of Treasuries lowers the risk of fire sales in Treasuries, the fact that the balance sheet also holds more than 15 percent of outstanding agency mortgage-backed securities (MBS) should also contribute to decreased volatility. As interest rates rise, prepayment risk on the MBS held by private investors decreases, so their average portfolio duration increases, leaving them more exposed to potential capital losses. One way they can counteract this effect is by selling long-dated Treasuries, further lowering their price. Everything else being the same, the risk of this happening should decrease the more MBS the Fed’s balance sheet holds.

Forward guidance has been of the utmost importance during the accommodation period and may also prove useful during the removal of that accommodation. Take the use of thresholds to guide the path of the FFR. The FOMC has made explicit what sort of economic conditions would lead to a lift-off of the FFR so that agents react immediately to changing economic conditions in forming expectations about future rates. Moreover, the fact that the Committee now regularly puts out, in the form of the Summary for Economic Projections, its forecast for economic conditions under appropriate policy, should help align the market and the Committee’s expectations.

Forward guidance such as this can, in principle, avoid credit market turbulence that would have resulted from market participants being surprised by the actions of the Committee. What it cannot do is avoid credit market reactions that result from both the Committee and the market being surprised by economic conditions.

Moreover, communicating forward guidance can be a challenging process, fraught with pitfalls like market overreaction. Following the June 2013 FOMC meeting, Chairman Bernanke tried to clarify the conditionality surrounding future asset purchases only to see long-term rates jump substantially in the following week. While many factors move interest rates, it is hard to believe that something other than the market’s interpretation of the chairman’s comments was behind this abrupt jump in rates.

The market is, of course, well aware of the history associated with past tightening cycles as well as how the monetary policy context has changed since then. Given all this, what is it expecting will happen this time around? As of March of this year, expectations for the 10-year Treasury rate implied increases from a level of about 2 percent to somewhere between 3.25 and 3.75 percent at the end of 2015, and somewhere between 4 and 5 percent at the end of 2017.7 As of the end of June, though, the market had revised up its expectations considerably, and the 10-year rate was forecasted to hit 3 percent by the end of 2014.8 This is a testimony to the high degree of uncertainty surrounding these expectations. The hope is that such uncertainty is coming mostly from the inherent randomness associated with future economic activity and that the Committee is actually helping to reduce it with its new tools and recent actions.

Footnotes

- Up until 1994 the Committee did not announce its federal funds rate target. Data for the period prior to 1994 come from the working paper, “A New Federal Funds Rate Target Series: September 27, 1982–December 31, 1993” (Daniel L. Thornton, 2005. Federal Reserve Bank of St. Louis.). Data from 1994 to the present are derived from FOMC meeting transcripts and FOMC meeting statements. Return

- See Longstaff, Francis A., and Eduardo S. Schwartz, 1995. “A Simple Approach to Valuing Risky Fixed and Floating Rate Debt,” Journal of Finance, 50, 789–820. Return

- Starting in early 2000 the spread actually increased substantially, but that was during a period when Treasury rates had already started coming down, so one can hardly argue that the spread was increasing because the Committee was increasing short-term interest rates. Return

- See Ehrbar, Ali, 1994. “The Great Bond Massacre,” Fortune (October 17). Return

- See Borio, Claudio E.V., and Robert N. McCauley, 1995. “The Anatomy of the Bond Market Turbulence of 1994,” Bank for International Settlements, working paper no. 32. Return

- See Pakko, Michael R. and David C. Wheelock, 1996. “Monetary Policy and Financial Market Expectations: What Did They Know and When Did They Know It?” Federal Reserve Bank of St. Louis, Review, 78:5, 19–32. Return

- See Bernanke, Ben, 2013. “Long-Term Interest Rates,” remarks at the “Annual Monetary/Macroeconomics Conference: The Past and Future of Monetary Policy,” sponsored by the Federal Reserve Bank of San Francisco. Return

- Blue Chip Financial Forecasts, July 1, 2013. Return

Suggested Citation

Amaral, Pedro S. 2013. “Monetary Policy Tightening and Long-Term Interest Rates.” Federal Reserve Bank of Cleveland, Economic Commentary 2013-08. https://doi.org/10.26509/frbc-ec-201308

This work by Federal Reserve Bank of Cleveland is licensed under Creative Commons Attribution-NonCommercial 4.0 International